Martin Lewis has included new tips to assist consumers maximise their financial resources during interest rate increases.

According to The Money Saving Expert, rates for savings accounts and Cash ISAs have both increased as a result of the ongoing Bank of England interest rate hikes.

According to him, this may translate into savings account interest gains of hundreds of pounds for those who shop about for the best rates.

He has already done the legwork for savers by recommending the current top rates for people with savings of at least £8,000.

His recommendation is to “ditch it” if you opened a Cash ISA more than six months ago because the rate “will be terrible.”

Due to taxes, he claimed, customers would receive more interest in an ISA than in a typical savings account.

It’s time for millions to reopen cash ISAs, Martin Lewis stated on the most recent episode of The Martin Lewis Podcast on BBC Sounds.

Anyone with £8,000 in savings should check right away to see if their money is in a cash ISA because the top pay 5.7% and interest rates are rising.

Cash ISAs often pay a little less than the corresponding regular savings. Thus, it is only for those who would pay taxes.

“So it’s about over £8,000 for a lower rate taxpayer and £16,000 for a higher rate taxpayer. Over those amounts is when you want to start looking at it.”

Martin then walked listeners through the best solutions available right now. On simple access savings, Chip pays 4.51%, he stated. Normal savings surpass cash ISAs because the top Cash ISAs, Leeds Building Society and Principality, pay 4.2%.

yet, if you are paying taxes, the chip’s tax rate is 4.5%; yet, if you were paying 20% tax on the chip, your equivalent rate would be 3.16%.

‘If you were paying 40% tax, your equivalent rate is 2.7%, significantly less than you would get in a cash ISA,’ says the calculator.

The best bank accounts for right now are then encouraged to be checked out, Martin suggested.

The top one-year fix in regular savings, he noted, is offered by Vanquis Bank at 6.15%. The top cash ISA one-year fix rate from Natwest is 5.7%.

Some individuals who locked into cash ISAs ought to cancel them and pay the associated fees.

In general, it is advised to withdraw from a Cash ISA if you opened it more than six months ago.

If you had locked in your rates more than six months ago, they would have been very high.

“You will have to pay a penalty to get out,” she said, “but generally, you will earn more in the new ISA than the interest penalty will cost you because an interest penalty where the interest isn’t that much.”

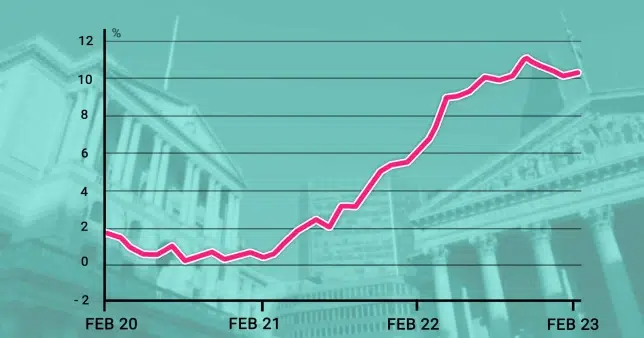

The Bank of England has increased interest rates for the thirteenth time in a row as Britain’s inflation rate remains persistently high.

The rate was almost nil at the end of 2021, thus the central bank’s announcement today that it has increased it to 5% from 4.5% is startling.

As a result, the rate has risen to its highest level in 15 years once more. The Bank of England boosted interest rates, generally known as the bank rate, by 0.25% last month.

The cost of borrowing money for things like mortgages, loans, and savings accounts increases as interest rates rise.

The statistics agency said April’s figure being glued into place was driven by higher prices for flights, second-hand cars and live gig tickets.

Anaam Raza, of investment platform Saxo, told Metro.co.uk: ‘It was common knowledge that the Bank of England was preparing to raise interest rates today for the 13th time in a row.

‘This will be a large blow to the UK population, particularly mortgage holders.’

Given that interest rates are now even higher, monthly mortgage payments will likely soar. Those applying for mortgages may see offers pulled or rates jacked up.

This only adds financial pain to even more Brits already struggling with soaring food costs, with grocery shops throughout a month thought to be more expensive than energy bills.

According to the ONS, food inflation eased slightly to 18.4% in May, down from 19.1% in the year to April 2023, though this is still close to the 45-year high.

The Bank has been on the attack for the last half a year as Britain faces its worst inflation in four decades, with raising interest rates being its best weapon.

The Bank’s policy-makers hope that, by making borrowing costs higher, people will be more inclined to save rather than spend, so demand for goods go down.

Inflation would, they hope, go down with it so prices won’t climb as fast as they are now.

The BoE is tasked with cooling down inflation to 2% but the figure was in the double digits for months, peaking at 11.1% in October. The government, meanwhile, is hoping to halve inflation by the end of the year.

When setting interest rates, BoE policy-makers closely look at core inflation, which is how fast the prices for goods and services are rising with the exception of food and energy.

Core inflation is a good gauge of how deep inflation has burrowed into the economy as, to economists, it removes the price changes of food and energy.

Experts see these as more volatile – they’re more easily spooked by outside influences like bad harvests, for example, and things that people can’t go without.

Services like cinema tickets or haircuts, though, which core inflation considers, can though. So core inflation rising suggests people are cutting back spending on all but the necessities.

Core inflation in May, the ONS said yesterday, climbed to 7.1% in the year through May, the fastest pace since 1992.

Tommaso Aquilante, associate director of economic research at the business analysts Dun & Bradstreet, told Metro.co.uk: ‘It’s the highest level for over 30 years, leaving the UK with the highest core inflation rate in the G7.’

‘With the [Consumer Price Index] inflation rate remaining sticky at 8.7% yesterday and everyday prices still remaining high,’ Saxon’s Raza added, ‘thousands across the UK will now be stuck between a rock and a hard place when deciding what to do next with their personal finances.’

On Thursday, the Bank of England is anticipated to increase interest rates from 4.5% to 4.75% as part of its efforts to curb inflation.

UK’s inflation to drop in May and was stuck at 8.7%.

However, there are speculations among economists that the Bank may opt for a more significant increase of 0.5%.

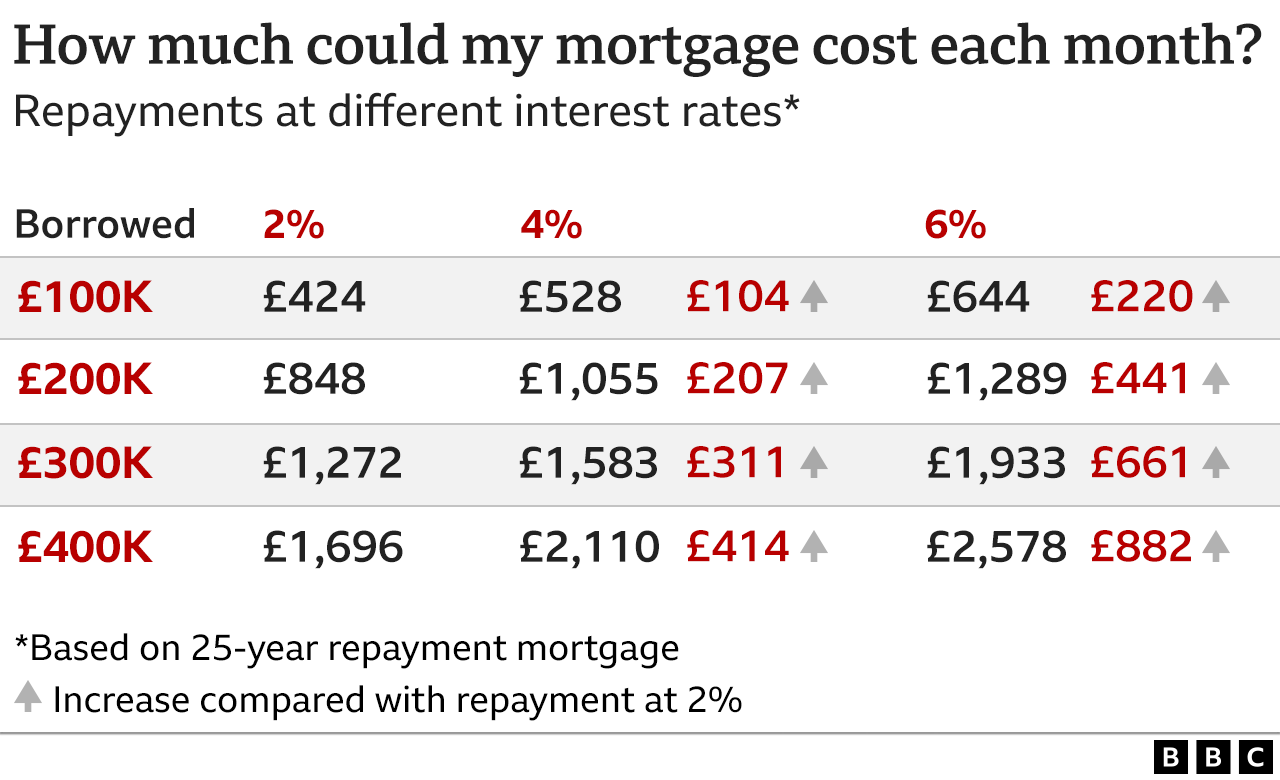

Should the rates rise, it is expected that mortgage rates will also go up for individuals seeking to re-mortgage or those with variable-rate mortgages. Approximately 800,000 individuals are projected to re-mortgage next year.

As of today, a typical two-year fixed mortgage deal carries an interest rate of 6.15%. Meanwhile, the standard variable rate, effective from 1 June 2023, stands at 7.52%, as reported by financial data firm Moneyfacts.

In recent weeks, mortgage lenders have been withdrawing mortgage deals and swiftly raising rates.

Additionally, Chancellor Jeremy Hunt announced yesterday that there will not be a major scheme implemented to provide assistance to homeowners facing financial difficulties.

A private attorney, Albert Gyamfi, has stated that taking money from a deceased person’s bank account to pay for their funeral is illegal and punishable by law.

According to the lawyer, although this is a common practice in the Ghanaian sociocultural context, the act, by law, is characterised as intermeddling with the property of the deceased, an act that is punishable by law.

Mr Gyamfi further explained to the host of The Law, Samson Lardy Anyenini that the bank account of a deceased by law is immediately closed off when the person is declared dead.

Thus, no relative can access the bank account of the deceased until a letter of administration (LA) or probate has been granted to them to have access to the bank account, he said.

“Let me sound this warning, the general practice has been that when a person dies, people would want to go into his bank account for money for the organization of the funeral. That is intermeddling. Wherever the family will find a room to organize the funeral, they should do so. And when probate has been granted, then if there’s any property to liquidate that debt, they use his property to do so.”

“But you cannot go into his bank account, withdraw money for purpose of a funeral. As soon as the person dies, doctors declare him dead, his bank account is closed until probate has been granted,” Mr Gyamfi cautioned while contributing to a discussion on The Law on Sunday. Withdrawing money from a deceased’s account to organise funeral is a criminal offence – Lawyer

Subsequently, he shared that in a situation where an individual gathers the properties of a deceased person to safe keep the assets but does not deprive the entitled persons of the use of the property, such an act was not categorised as intermeddling with the properties of the dead person.

“If you look at section 17, the law principally says, unlawfully deprive the entitled persons of the use. So, the law has a mens rea of you unlawfully depriving persons of the use. So, if I am only gathering them for safekeeping, I am not depriving people of the use,” Mr Gyamfi emphasised.

Hence, referencing a scenario whereby the deceased person was the owner of a vehicle that was being used as a commercial vehicle, the lawyer advised that a driver in such a case keeps the sales received safe until legitimate administrators are appointed to whom the driver can give an account of the money received.

However, he warned that the inability of the said driver to account for the money is categorised as intermeddling.

So, the lawyer stated that, “If you are unable to account and some monies are gone somewhere, then you can be said to have been depriving the beneficiaries of the use, and you will be guilty of intermeddling.

“So gathering properties in good faith for purposes of administration in mind does not amount to intermeddling,” Mr Gyamfi reiterated.

Following Wednesday’s unexpected increase in inflation, the Bank of England is predicted to increase interest rates for the eleventh time in less than 18 months.

It will make its most recent judgment at midday as it attempts to balance the UK’s bleak economic prospects with a global banking crisis.

The BoE must strike a delicate balance between the need to control inflation and concerns about the state of the banking system and the potential for lending restrictions.

Last month the raise in interest rates meant it was the highest in 14 years.

Yesterday’s data – showing inflation rising to 10.4% in February rather than continuing its descent – immediately turned today’s announcement into an almost one-way bet on a quarter-percentage-point increase in Bank Rate.

Financial markets widely expect a 0.25 percentage point hike to 4.25%.

It comes after inflation hit a 41-year high at 11.1% in October last year.

The Bank of England will make an announcement at noon today (Picture: EPA)

As recently as Tuesday, investors were split almost 50-50 on whether the BoE would leave Bank Rate unchanged for the first time since November 2021.

Bets earlier this week on the BoE halting its run of rate hikes were further bolstered by the rescue of Credit Suisse and the collapse of Silicon Valley Bank which showed how some global banks were struggling to adjust to higher borrowing costs.

Any increase in Bank Rate would be part of a series of measures to reduce inflation, but would inevitably increase pressure on many people, particularly mortgage holders, already being squeezed by the cost-of-living crisis.

The European Central Bank also raised its three main interest rates by 50 basis points last week despite financial market turmoil engulfing Credit Suisse and the collapse of Silicon Valley Bank.

While some of the inflation rise can be blamed on one-off factors such as vegetable shortages, the underlying measures that the Bank of England tracks have also increased.

It was the first major central bank to start raising interest rates in December 2021.

NG economist James Smith said he expected any rate hike was likely to prove the last in the Bank of England’s run.

He said: ‘Assuming the broader inflation data continues to point to an easing in pipeline pressures, then we suspect the committee will be comfortable with pausing by the time of the next meeting in May.’

Shares on Wall Street tumbled sharply overnight on the Fed’s decision and its comments suggesting it does not expect to cut rates anytime soon, highlighting the fragility of stock market confidence.

After three days of bounceback gains, the S&P 500 fell 1.7%, while the Dow Jones Industrial Average lost 1.6% and the Nasdaq composite dropped 1.6%.

Some of the sharpest drops again came from the banking industry, where investors are worried about the possibility of more banks failing if customers pull out their money all at once.

Craig Erlam, a senior market analyst for Oanda, said: ‘Whatever flexibility the Bank of England may have thought it would have on Thursday was wiped out by Wednesday morning’s inflation data.’

He added there is ‘nothing that would justify a pause’ in raising interest rates, ‘even against the backdrop of financial stability concerns and the knock-on effects of aggressive rate hikes’.

It also threw into question whether higher interest rates are putting too much pressure on smaller lenders, which could be buckling under the weight of losses on their investments.

ING Economics suggests the Bank of England will want to see more evidence that inflationary pressures are easing up more broadly before ending its cycle of rate rises.

Meanwhile, Investec Economics predicts the Bank will opt for a ‘wait-and-see approach’ and keep rates at 4% while it assesses the situation.

Economist Ellie Henderson said: ‘The MPC will have to assess which is the lesser of two evils: the risk of inflation being higher for longer or the current threat to financial stability stemming from the rapidly evolving fears of a banking crisis.’

In order to strengthen its finances, Credit Suisse has announced that it will borrow up to 50 billion Swiss francs (£44.5 billion) from the nation’s central bank.

The struggling banking behemoth declared that it is taking “decisive action” to improve and streamline its operations.+

Following the announcement that it had discovered “weakness” in its financial reporting, shares of Credit Suisse dropped 24% on Wednesday.

Fears of a wider banking crisis sparked steep falls on stock markets, with Asian shares dropping.

However, markets in Europe are expected to open higher on Thursday.

The BBC understands that the Bank of England has been in touch with Credit Suisse and the Swiss authorities to monitor the situation.

Swiss National Bank, the country’s central bank, insisted Credit Suisse had the money it needed, but stressed it was ready to step in and help further if required.

Problems in the banking sector surfaced in the US last week with the shock collapse of Silicon Valley Bank, the country’s 16th-largest lender, followed two days later by the failure of New York’s Signature Bank.

The US central bank had been forced to step in to prevent a run on bank deposits as panic spread.

Sir John Gieve, former deputy governor at the Bank of England, told the BBC that central banks were sending a “message” that such problems would be contained locally.

He added that in Credit Suisse’s case, this was likely to be enough to stop the crisis spreading.

“What we’ve seen overnight is the Swiss central bank saying no, we will not let this get into a disorderly collapse,” he told the BBC’s Today programme.

“I don’t know what the future for Credit Suisse holds but so far they are still standing and it looks like the Swiss central bank will ensure it’s standing long enough to rearrange its affairs for the future.”

Japan’s Nikkei 225 index was down by 1.1% in late midday trading, with markets in Hong Kong and Sydney down by over 1.5%. The Shanghai Composite lost 0.5%.

‘Material weaknesses’

Credit Suisse, founded in 1856, has faced a string of scandals in recent years, including money laundering charges, spying allegations and high profile departures.

It lost money in 2021 and again in 2022 and has warned it does not expect to be profitable until next year.

The bank’s disclosure on Tuesday of “material weakness” in its financial reporting renewed investor concerns.

Daniel Davies, managing director at Frontline Analysts, and a former bank analyst at Credit Suisse, said that the bank’s “millionaire and billionaire client base just seems to have reached the end of their tolerance and they’ve been taking money out over the last six months at what began to look like an increasing rate”.

He added that the Bank of England will have been asking its Swiss counterpart whether it still had faith in Credit Suisse.

“Because the nature of these crises is that when you have a real massive deposit run it is like a tsunami – nothing humans can make can stop it. The only thing you can do is stop it before it turns into a proper deposit run and the only people that can do that are the central banks.”

These were intensified when the Saudi National Bank, Credit Suisse’s largest shareholder, said it would not buy more shares in the Swiss bank on regulatory grounds.

On Wednesday shares in the lender plunged as other banks rushed to pull out their funds from the bank and prime ministers in Spain and France spoke out in an attempt to ease fears.

The collapse of Silicon Valley Bank has also fuelled concerns about the value of bonds held by banks, as rising interest rates made those bonds less valuable.

Central banks around the world – including the US Federal Reserve and the Bank of England – have sharply increased interest rates as they try to curb the rate of price rises, or inflation.

Banks tend to hold large portfolios of bonds and as a result are sitting on significant potential losses.

The falls in the value of bonds held by banks is not necessarily a problem unless they are forced to sell them.

Silicon Valley Bank – which specialised in lending to technology companies – was shut down on Friday by US regulators in what was the largest failure of a US bank since 2008.

The Bank of England has unveiled the new design for banknotes that feature the image of King Charles.

The only change to the current designs of the £5, £10, £20, and £50 notes will be the portrait, which will go into circulation in the middle of 2024.

The King’s portrait will appear on new notes on the front and in the transparent security window.

After the new notes start to circulate, old notes will still be accepted in stores.

Beginning in 1960, Queen Elizabeth was the first and only monarch to be depicted on circulating Bank of England banknotes. The monarch is not shown on the notes that Scottish and Northern Irish banks have issued.

There are about 4.5 billion individual Bank of England notes worth about £80bn in circulation at present.

The King’s cypher will also appear on the notes

The Bank of England said that, following guidance from the Royal household, the new notes would only be printed to replace worn notes or to meet increased demand, in order to minimise the environmental and financial impact of the change.

Bank of England governor, Andrew Bailey, said he was “proud” of a “significant moment” with the new design.

Fifty pence coins bearing the image of King Charles III have already entered circulation via post offices across the country.

An estimated 4.9 million of the new coins are being distributed to post offices – about half of the total number earmarked for circulation – to be given in change to customers.

The new King Charles 50p coins have already entered circulation

Coins carrying the image of the late Queen will still be accepted in shops, in the same way as banknotes.

For anyone taking part in a family Christmas quiz this year, it is worth remembering that, in ascending order, the reverse side of current polymer Bank of England banknotes feature Sir Winston Churchill, Jane Austen, JMW Turner and Alan Turing.

Cash use has become far less frequent when compared to debit cards, owing primarily to the use of contactless payments and then accelerated by the Covid pandemic. The buying power of specific coins and banknotes have also been diluted by rising prices.

However, there is still keen interest from consumers and collectors about the images used on cash.

Collectors will be particularly excited to get their hands on the lowest serial numbers of the new King Charles banknotes when they appear.

As the impact of the Queen’s funeral continues to play out in UK growth figures, there is no reason to rejoice.

According to preliminary official figures, the economy returned to growth in October, which experts believe could be the last for some time.

The Office for National Statistics (ONS) reported 0.5% growth in October, following a 0.6% contraction in September, which was largely attributed to disruption to normal activity due to the Queen’s funeral bank holiday.

The partial recovery in October, which was slightly stronger than expected, was largely explained by the return of normal working days rather than any real surge in output.

The ONS charted the main boost coming from wholesale and retail activity – both significantly affected by closures as a mark of respect to the late Queen.

As such, economists still expect a recession to be confirmed at the end of the year.

That is because output is tipped to be negative during the current fourth quarter as a whole, following the 0.2% dip recorded for the third quarter to September.

The Bank of England and Office for Budget Responsibility – which have both already declared their belief that the UK is in recession – expect the downturn to last throughout 2023 but remain shallow.

Economic activity has slowed as a result of high inflation, mostly caused by Russia’s war in Ukraine, curbing appetite for spending.

Interest rate rises from the Bank, aimed at curbing inflation, have raised borrowing costs to further dampen demand.

Fixed rate mortgages, also, are yet to ease back to levels seen before the September mini-budget which saw financial markets baulk at the spending plans of the-then Liz Truss-led government.

New chancellor Jeremy Hunt, who has since rowed back on the growth measures, said of the latest growth figures: “High inflation, exacerbated by Putin’s illegal war, is slowing growth across the world, with the IMF predicting a third of the world economy will be in recession this year or next.

“While today’s figures show some growth, I want to be honest that there is a tough road ahead.

“Like the rest of Europe, we are not immune from the aftershocks of Covid-19, Putin’s war and high global gas prices.

“Our plan has restored economic stability and will help drive down inflation next year, but also lay the foundations for long-term growth through continued record investment in new infrastructure, science and innovation.”

The Bank, which raised its rate by 0.75 percentage points last month, is widely expected to impose a further hike of 0.5 percentage points this week.

It is anticipating an easing in energy-driven inflation ahead but forecast to maintain the pressure given that the rate of inflation is at a 41-year high of 11.1%.

Figures for November, due on Wednesday, are expected to show an annual rate of 10.9% according to economists polled by the Reuters news agency.

The UK is “not as wealthy a nation as it thought it would have been in 2020”, Sky’s economics and data editor Ed Conway has said.

Analysing the country’s financial situation, Ed said that before the pandemic GDP was expected to rise but then when the pandemic hit there was a “massive fall down”.

He went on to say the Bank of England forecast’s were now flatlining.

“There’s a lot of other things going on right now. The dollar has been very strong recently as well,” he adds.

“But even so, these charts, whether it’s the pound, whether it’s government bond yields, are the kinds of things that the government is going to be paying attention to.”

He adds that looking at the latest charts helps explain why the UK will most likely receive a “miserable” update from the chancellor today.

The latest wage figures will likely concern policymakers at the Bank of England who fear increases will fuel inflation further down the line.

Wage growth picked up by more than expected over the three months to September, according to official figures also showing a rise in the jobless rate.

The Office for National Statistics (ONS)said average weekly earnings, excluding bonus payments, rose at an annual rate of 5.7% during the three months to September as more workers secured better deals to help navigate the cost of living crisis and firms moved to retain and attract staff.

That was up from the 5.4% figure last month.

Economists polled by Reuters had expected an increase of 5.5%.

Nevertheless, at 5.7% it remains well below the official rate of inflation at 10.1%.

Real wage growth was 3.7% weaker in September when the effects of inflation were included, the ONS said.

The unemployment rate rose to 3.6% from 3.5% as the number of people in employment fell by 52,000.

Darren Morgan, ONS director of labour and economic statistics, said of the shift: “The proportion of people neither working nor looking for work has risen again.

“Since the onset of the pandemic, this shift has largely been caused by older workers leaving the labour market altogether, but in the most recent quarter the main contribution has actually come from younger groups.

“August and September saw well over half a million working days lost to strikes, the highest two-month total in more than a decade, with the vast majority coming from the transport and communications sectors.

“With real earnings continuing to fall, it’s not surprising that employers we survey are telling us most disputes are about pay.”

The figures were released as the economy battles problems from the highest inflation for 40 years and the fallout from Trussonomics – namely the now largely reversed mini-budget of September.

Official figures last week showed the economy contracted during the third quarter of the year as the cost of living crisis hit demand, leaving the country on course for a prolonged but shallow recession, according to the Bank of England, which believes the jobless rate could hit 6.5%.

The rate is the single most important interest rate in the UK and determines the rate the Bank of England pays to commercial banks that hold money with them. It influences the rates those banks charge people to borrow money or pay on their savings.

The Truss government’s growth plan exacerbated problems as financial markets called into question the UK’s economic credibility, making imports more expensive through a collapse in the value of the pound.

Other implications included a rise in fixed-term mortgage costs, adding to households’ growing bill mountain.

Jeremy Hunt, the chancellor, will deliver his autumn statement to MPs on Thursday with little firepower to help alleviate the overall pain.

‘Taxes will increase for everyone’

He told Sky News on Sunday that everyone faced higher taxes as the government, now led by Rishi Sunak, aims to take a more sustainable approach to the public finances.

It is believed the package will be designed to save about £50bn from annual borrowing in the medium term.

Mr Hunt said in reaction to the employment data: “Tackling inflation is my absolute priority and that guides the difficult decisions on tax and spending we will make on Thursday.

press home the knock-on impact of 12 years of Tory economic mistakes and low growth.

“Real wages have fallen again, thousands of over 50s have left the labour market and a record number of people are out of work because they’re stuck on NHS waiting lists or they’re not getting proper employment support.

“What Britain needs in the autumn statement on Thursday are fairer choices for working people, and a proper plan for growth.”

As traders responded to the data, shares climbed in the US and Asia. On Friday morning, stock markets in the UK and Europe also increased.

According to the Labor Department, the US consumer price index increased 7.7% in October compared to the same month last year.

Since the beginning of the year, that is the smallest annual increase.

The figure, which is down from 8.2 per cent the previous month, means the US central bank may ease its aggressive approach to raising interest rates to tackle inflation.

On Friday Hong Kong’s Hang Seng index jumped by 7.7 per cent, while the Nikkei in Japan ended the day three per cent higher and South Korea’s Kospi gained 3.4 per cent.

That came after the benchmark S&P 500 index in New York rose by more than 5.5 per cent, while the Dow Jones Industrial Average gained 3.7 per cent. At the same time the technology-heavy Nasdaq soared by 7.35 per cent.

Shares in US technology companies saw some of the strongest gains with Amazon up by over 12 per cent, while Apple and Microsoft rose more than eight per cent.

European share prices edged higher on Friday too, although they didn’t match the large gains seen in the US and Asia.

In London, the FTSE 100 index was up by 0.4 per cent in early trading after official figures showed the UK appears to be heading into recession.

The economy contracted by 0.2 per cent between July and September, according to the Office for National Statistics.

Meanwhile the US dollar, which has jumped in value this year, weakened against major currencies including the pound and the yen.

Earlier this month the US Federal Reserve raised its key interest rate to a fresh 14-year high.

The move took the central bank’s benchmark lending rate to 3.75 per cent-4 per cent, the highest since January 2008.

Also this month, the Bank of England lifted interest rates to three per cent from 2.25 per cent, the biggest jump since 1989, and warned that the UK is facing its longest recession since records began.

A recession is defined as when a country’s economy shrinks for two three-month periods – or quarters – in a row.

Higher interest rates make it less likely that people will spend on big ticket items, such as homes, cars or expanding their businesses. That fall in demand is, in turn, expected to curb price increases.

Food and energy prices have jumped, in part because of the Ukraine war, which has left many households around the world facing hardship and started to drag on the global economy.

But some economists are concerned that higher rates could also trigger slowdown in the global economy.

Share prices have risen as investors greet official data showing that the cost of living in the United States increased at a slower-than-expected rate last month.

Shares soared in the United States and Asia as traders reacted to the data, and stock markets in the United Kingdom and Europe rose on Friday morning.

According to the Labor Department, the US consumer price index increased 7.7% year on year in October.

Since the beginning of the year, this is the smallest annual increase.

The figure, which is down from 8.2% the previous month, means the US central bank may ease its aggressive approach to raising interest rates to tackle inflation.

On Friday Hong Kong’s Hang Seng index jumped by 7.7%, while the Nikkei in Japan ended the day 3% higher and South Korea’s Kospi gained 3.4%.

The Hang Seng was also boosted after Chinese state media reported that Covid-19 travel measures will be eased.

That came after the benchmark S&P 500 index in New York rose by more than 5.5%, while the Dow Jones Industrial Average gained 3.7%. At the same time the technology-heavy Nasdaq soared by 7.35%.

Shares in US technology companies saw some of the strongest gains with Amazon up by over 12%, while Apple and Microsoft rose more than 8%.

European share prices edged higher on Friday too, although they didn’t match the large gains seen in the US and Asia.

In London, the FTSE 100 index was up by 0.4% in early trading after official figures showed the UK appears to be heading into recession.

The economy contracted by 0.2% between July and September, according to the Office for National Statistics.

Meanwhile the US dollar, which has jumped in value this year, weakened against major currencies including the pound and the yen.

Earlier this month the US Federal Reserve raised its key interest rate to a fresh 14-year high.

The move took the central bank’s benchmark lending rate to 3.75%-4%, the highest since January 2008.

Also this month, the Bank of England lifted interest rates to 3% from 2.25%, the biggest jump since 1989, and warned that the UK is facing its longest recession since records began.

A recession is defined as when a country’s economy shrinks for two three-month periods – or quarters – in a row.

Higher interest rates make it less likely that people will spend on big ticket items, such as homes, cars or expanding their businesses. That fall in demand is, in turn, expected to curb price increases.

Food and energy prices have jumped, in part because of the Ukraine war, which has left many households around the world facing hardship and started to drag on the global economy.

Centrica reveals more assistance for vulnerable households as it updates the market on its financial performance, predicting that the group as a whole will outperform many analysts’ expectations.

The parent company of British Gas has announced additional assistance for struggling customers while lowering profit expectations for its household supply division due to lower demand.

Centrica said: “Warmer than normal weather in October has contributed towards lower volumes and profits in British Gas Energy”.

It also pointed to “broader inflationary and economic pressures” hitting the cost base and customer numbers in British Gas Services & Solutions.

It added: “As a result, we expect adjusted operating profit in our retail division to be lower than current expectations.”

Centrica made the announcement as consumer groups and surveys report surging numbers of households leaving the heating off as temperatures drop because of record prices for gas and electricity.

While household energy bills have soared, the wider cost of living crisis is further squeezing spending power.

Inflation is running at a 40-year high of 10.1% and is tipped by the Bank of England to peak at around 11% – lower than it had initially thought.

That is largely because the government’s energy price guarantee covering wholesale prices will limit bill increases this winter.

However, it sees rising interest rates to tackle inflation resulting in the average household facing a £3,000 annual increase in their mortgage costs.

That more than outweighs any government help with energy bills.

‘I hope Sunak brings our energy prices right down’

Centrica said of British Gas: “With over 10 million customers, we are acutely aware of the difficult environment facing many people and we remain committed to doing what we can to support those who need our help most.

“Today, Centrica is announcing an additional £25m of help for our customers, taking the amount we have invested in voluntary customer support this year to £50m.

Its shares soared by up to 9% on its wider trading update, however, as it was intended to set the market straight on the group’s financial performance as a whole.

It indicated that many of the analysts who watch its performance might be making overly cautious predictions.

Centrica said group earnings per share were likely to be closer towards the 26p that the most optimistic experts expect than the 15.1p that the most pessimistic have forecast.

“Centrica has continued to deliver strong operational performance from its balanced portfolio since its interim results in July and now expects full-year adjusted earnings per share to be towards the top end of the range of more recent sell-side analyst expectations,” its statement said.

The parts of the business that generate electricity and extract gas from under the ground have performed well in recent months.

It’s sort of discombobulated because we’ve been just running 100 miles an hour.

It has calmed down a bit, but I would describe it as the calm before the storm – because of what we’ve seen in terms of the Bank of England‘s decision on lifting interest rates.

But inflation is going to peak, quite soon, and lower than perhaps expected.

They are also talking about a recession – a very long, potentially quite long recession – potentially the longest recession since records began.

So that’s all worrying for the government at a time when there is this black hole in the public finances, exacerbated by the decisions that Liz Truss took… and Jeremy Hunt, the new chancellor, has now reversed.

So Rishi Sunak and his chancellor have got a series of very difficult decisions to take on tax and spending.

How are you going to get that through the party? There are so many different views about what he should do.

The Federal Reserve announced a 0.75 percentage point increase in its key interest rate, bringing it to its highest level since early 2008.

The bank believes that raising borrowing costs will cool the economy and reduce price inflation.

However, critics are concerned that the moves will precipitate a severe downturn.

The latest increase takes the bank’s benchmark lending rate to 3.75% – 4%, a range which is the highest since January 2008.

Many other countries are moving along with the US to raise borrowing costs, as they grapple with their own inflation problems.

In the UK, the Bank of England started raising rates last year but has so far opted for smaller hikes than the Fed. The Bank of England is expected to announce its own 0.75 percentage point hike on Thursday – the biggest such move since 1989.

The sharp rise in borrowing costs has already started to cool some parts of the economy, such as housing.

But economists say more economic slowdown is necessary if inflation is to return to the 2% level considered healthy.

“There is always the hope of painless, immaculate disinflation,” said economist Willem Buiter, a former member of the Monetary Policy Committee of the Bank of England who is now an independent economic advisor. “Unfortunately there are very few historical episodes that fit that picture”.

“This is not going to be a pleasant year,” he added.

Federal Reserve chairman Jerome Powell warned that rates were likely to move up again.

“We still have some ways to go and incoming data since our last meeting suggest that the ultimate level of interest rates will be higher than previously expected,” he said at a press conference following the announcement.

“We will stay the course until the job is done,” Mr Powell added.

Inflation – the rate at which prices rise – hit 8.2% in the US last month, continuing to fall after reaching 9.1% in June – the highest rate since 1981.

A decline in energy prices has helped ease the pressures, but the cost of groceries, medical bills, and many other items is still rising.

At the annual meetings of the World Bank and IMF this month, lobbyists circulated photographs of Ghana’s Finance Minister Ken Ofori-Atta sitting together with Britain’s Chancellor of the Exchequer Kwasi Kwarteng.

Before the end of the week, Chancellor Kwarteng was on a flight back to London, forced to cancel his participation in the rest of the summit because his job was at risk. Within days, the British government had collapsed, and Prime Minister Liz Truss had joined Kwarteng on the back benches.

This week Ghana’s Ofori-Atta faces a rebellion from MPs in his own party, calling for his resignation and accusing him of mismanaging the economy. The risk that London’s political drama plays out similarly in Accra must worry Ofori-Atta and President Nana Akufo-Addo.

Common shaky ground

On the surface, both men are relatively similar; Ghanaian economists and bankers are in charge of the fiscus of two countries with a shared colonial experience.

However, there is a deeper layer to the symbolic ties between the Chancellor and the Minister.

Kwasi Kwarteng’s woes are universally acknowledged to have stemmed from his botched mini-budget. At a time of widespread anguish about inflation and interest rate hikes in America, the mini-budget, with its ideological flourish of “the largest tax cuts since 1972” and unfunded growth pills, rang of neoliberal excess.

Interestingly, the heaviest backlash came from the markets. A Conservative Prime Minister and her Chancellor didn’t expect the blowback to come from the financial heartlands.

After all, caps on bankers’ bonuses were to be scrapped, and the highest tax rate (for the top 1.1%, roughly a third of whom work in financial services) was to be brought down from 45% to 40%. Planned corporation tax increases were dropped.

And a raft of regulations bogging down business was to be cut’ more free zones, with even fewer taxes and regulations, created. A Conservative newspaper, the Daily Mail, crooned: “A Tory budget at last!”

Surely the grandees of the historic square mile of central London, the fount of global capitalism, would jump on board? The charm offensive of the Chancellor, himself a JPMorgan alum and longtime finance guy, must have seen to that?

They didn’t.

Analysts deciphered the consequences of a mini-budget to include a massive spate of borrowing at a time of rising interest rates, an undoing of the Bank of England’s efforts to tackle inflation, and a squeeze of middle-class incomes (in the ~£60,000 to ¬£120,000 band), with potential effects on demand.

The market took a longer horizon and broader-demographic perspective. That aligns with the increasingly nuanced view of the link between pro-growth tax cuts and market benefit that has emerged from the vast literature on the Trump tax cuts.

So, the markets revolted.

Yields on long-term government securities, a measure of investors’ sense of the state’s creditworthiness and likely cost of future borrowing, rose by a staggering 150 basis points. The pound sterling sank immediately.

Lunging for stability, the blindsided Bank of England announced a £65 billion program to buy back government bonds caught in therout, reversing an earlier plan to sell £80 billion more into the market. Only the wholesale repudiation of the Kwarteng-Truss mini-budget could calm the markets.

Off the straight and narrow

It is mainly the short-lived tenor of Britain’s most recent episode of fiscal adventurism that marks it out from Ghana.

In their six years in power, the ruling party in Ghana has sought to transform the country’s finances into a rollercoaster capital market play. It has devised various unprecedented fiscal devices to do so.

It has securitised future tax streams, grabbed the cash up-front, and splashed on massive capital and welfare projects. The securitisation extravaganza has touched taxes meant to fund the educational sector, energy sector levies, and road taxes.

As future revenue streams have been packaged into products on the capital markets and sold and spent upfront, the government’s budget has become rigid, unable to respond to international pressure. The government’s love for fiscal gaming encouraged support for a domestic debt securities market (GFIM) in Ghana.

At its birth in 2015, total trade turnover hovered around cedis 5 billion in local currency units. In the first nine months of this year, trade volumes exceeded cedis170 bn.

Even adjusted for inflation, it has grown ten times, but almost all securities traded are government-issued. This means they reflect more than anything the government’s unrelenting use of the capital markets to fund a degree of fiscal expansion never before witnessed. And not just domestically.

From tripling Eurobond issuances, to opening up domestic debt to foreign investors, Ghana’s government took capital market liberalisation to every possible extreme. At one point, Ghana ranked number five worldwide for foreign ownership of domestic debt.

International capital maestros like Michael Hasenstab, at the height of his “Emerging Markets Bond King” reputation, piled in. In 2017, Ghana rode on the back of such powerbrokers to launch Africa’s largest-ever dollar-denominated domestic bond.

Bills, bills, bills

All this fiscal brinksmanship came at a cost: debt servicing.

Today, Ghana is on course to spend nearly 60% of all government revenue just dealing with debt. This is up from about 10% a decade and a half ago when the international community forgave a chunk of Ghana’s debt pile from previous decades of excesses.

Now, Ghana’s capital market friends have brought out the whips. They have shut her out of the market and are dumping the bonds they bought previously.

Their actions have finally driven Ghana to the IMF for much-needed disciplining. Inflation is hovering around 40% and the cedi has plunged from about 5.8 to the dollar at the beginning of the year to more than 14.5 to the dollar.

It seems that the government’s bubbly enthusiasm for capital market devices, and the massive hoard of fees and commissions (some shared by companies founded by the Finance Minister and his deputy), have not been sufficient to keep the love story going.

These days, far from endearing politicians to the markets, neoliberal fiscal adventurism is a sure way to invite their painful censure.

The gilt market was returned to its pre-Liz Truss mini-budget level shortly after Rishi Sunak was declared as Tory leader.

Gilts, or UK government bonds, are an essential part of our financial markets.

Following the mini-budget, the Bank of England was forced to intervene to prevent the gilt market from worsening.

UK government bonds were already staging a rally as Monday began and this rally became more aggressive as it became clearer that Rishi Sunak would likely face an unopposed run to the top job, business reporter Sharon Marris writes.

The 30-year gilt had been pummelled after Kwasi Kwarteng’s mini-budget in September but it recovered late on Monday to levels seen before Mr Kwarteng’s tax-cutting plans had prompted a markets meltdown.

Investors are betting that Mr Sunak, a former chancellor with a background in finance, will stick with the economic policies announced by current chancellor Jeremy Hunt, which have calmed the markets in recent days.

The former deputy governor of the Bank of England says the future Prime Minister will have to keep Jeremy Hunt as chancellor.

Prof Charlie Bean has been telling BBC Radio 4’s World At One programme that appointing a new chancellor would “generate volatility”.

He says any change to Hunt’s economic programme would be “problematic”,

“It is a significant tying of hands.”

Prof Bean praises Hunt for doing “quite a good job” of calming the markets and setting out a broad direction by “unwinding two-thirds” of the cost of Kwasi Kwarteng’s mini-budget which caused financial chaos last month.

He says there could be some “tweaking at the margins” of Hunt’s plans – but it would be “problematic” if the new PM came in and said they wanted a more significant change in the economic package ahead of the financial statement on 31 October.

Market estimatesfor the Bank of England’s bank rate are at their lowest since the mini-budget, which is excellent news for individuals with mortgages.

Market forecasts peaked soon after the mini-budget at 6.1%, but have since dropped to just over 5%.

It was just three weeks ago the then-Chancellor Kwasi Kwarteng unveiled his tax-cutting mini-budget to MPs, which caused economic turmoil in the UK,as the value of the pound plummeted.

Today, Mr Hunt said there “were mistakes” in last month’s announcement, and pointed out some taxes may have to rise and others might not fall as much as planned.

The BoE is due to announce its next decision on interest rates, which will impact household mortgages, on 3 November and many investors think it will either raise them from their current level of 2.25% to 3% or possibly 3.25%, both of which would be much bigger moves than usual.

After being in office for 38 days, Kwasi Kwarteng, the British-born politician of Ghanaian parentage was sacked by Prime Minister Liz Truss as the Chancellor of the Exchequer.

The dismissal was after Kwarteng presented a mini-budget which resulted in financial turbulence and revolt from Conservative Party lawmakers.

While presenting the mini-budget on 23 September, an eye-watering £45 billion in tax cuts alongside an energy relief plan projected to cost £60 billion over the next six months was announced by Kwasi Kwarteng.

This, according to various media reportage was a huge departure from the fiscal policy of the Johnson government, which had planned tax rises to pay for health and social care and to manage the post-Covid deficit.

Kwarteng claimed his ambitious plans would drive growth and reduce inflation.

The financial markets disagreed: in the days after his announcement, lenders pulled mortgage packages, the pound hit a record low against the dollar, and the Bank of England started buying bonds at ‘an urgent pace’ to calm the markets and stop pension funds going bust.

In a high-risk strategy designed to revive Britain’s stagnant economy, the British of Ghanaian descent announced more than £400bn of extra borrowing over the coming years to fund the biggest giveaway since Tony Barber’s ill-fated 1972 budget.

The Guardian reported that the Conservative MP said tax cuts worth more than £55,000 annually to someone earning £1m a year were part of a new direction for the economy and were designed to help boost growth to 2.5% a year. Some Labour MPs described them as a “class war”.

The Treasury admitted there were no forecasts for the impact of the measures on growth and the gamble received a hostile reception not just from the markets and opposition politicians, but from economic think tanks and many Tory MPs, some of whom were aghast.

The pound has gained as speculation about a possible U-turn on the mini-budgethas increased.

On Friday morning, sterling was trading above $1.13 versus the dollar as the chancellor returned home early from the United States for urgent discussions in Downing Street.

In September, the currency touched a record low of $1.03 as markets responded negatively to Kwasi Kwarteng’s mini-budget.

In it he promised billions of pounds of tax cuts but did not explain how he would fund them.

Government borrowing costs have also fallen, after surging to worrying levels in the days after the mini-budget.

The Bank of Englandhas been buying government bonds – known as gilts – to try to stabilise their price and prevent a sell-off that could put some pension funds at risk of collapse.

However, that support is due to come to an end on Friday.

There has been speculation it may be extended, although this was dismissed by the Bank’s governor, Andrew Bailey, earlier this week.

The government has already U-turned on its plan to scrap the top rate of income tax, but many Conservative MPs think a further change of plan is imminent.

Russ Mould, investment director at AJ Bell, said the financial markets were already pricing in a government U-turn.

“They started to [price it in] yesterday,” he told the BBC’s Today programme.

Mr Mould pointed to the fact that the yields – or the effective interest rate – on UK government bonds have been falling back in anticipation of a reversal to the tax-cutting plans. On Friday morning, the yield on bonds that borrow money over 30 years fell to 4.47%.

“Gilt yields came down… and sterling rose against the dollar to $1.13 and against the euro to €1.16, so I think they are starting to either expect, demand, sniff out that there will be some degree of U-turn possibly on corporation tax, dividend tax, other areas,” Mr Mould said.

Asked what would happen if there is no U-turn, Mr Mould said: “You would expect the gains that we’ve started to see, to unwind.”

Bank of England support

The government raises the money it needs for spending by selling bonds – a form of debt that is paid back plus interest in anywhere between five and 30 years.

Pension funds invest in bonds because they provide a low but usually reliable return over a long period of time.

However, the sharp fall in their value after the mini-budget forced pension funds to sell bonds, threatening to create a “downward spiral” in their prices as more were offloaded, which left some funds close to collapse.

This sparked an emergency intervention by the Bank of England,which stepped in to buy bonds and prevent their price falling further.

There has been strong speculation that the Bank will extend the scheme, which is due to end on Friday.

But on Tuesday, Mr Bailey dashed those hopes, telling pension funds: “You’ve got three days left now and you’ve got to sort it out.”

Bethany Payne, global bonds fund manager at Janus Henderson, told the BBC it was not clear whether pension funds have done enough to strengthen their finances.

“The risk is that we don’t know how pension funds have used this window of time and whether they have used it effectively by raising cash and doing everything they need to,” she said.

“So the true test of the market will be this afternoon and Monday morning to see whether they have done enough.”

More from Trade Minister Greg Hands, who says the rally in UK financialmarkets yesterday and this morning could be due to “a variety of different factors.”

The pound has climbed against the dollar, and yields on government bonds, known as gilts, have fallen, lowering the cost of borrowing for the government.

When asked if former Bank of England governor Mark Carney is wrong to imply they are reacting to the idea that the government will reverse its decision on the mini-budget soon, the minister refused to answer.

Hands cite the Japanese Yen hitting a 30-year low against the US dollar and the euro performing as poorly as the pound as other reasons that could have caused the rally.

He cites his own experience working in financial services and argues they “behave the way they do based on information that comes into them from a multitude of different sources”.

“It’s not a UK-only thing,” Hands tells the Today programme.

Pushed on whether the country would be better off if his preferred candidate Rishi Sunak had become prime minister, Hands says “no” and calls on the Conservative Party to “unite behind” Liz Truss.

The Bank of England is set to stop its government bond-buying scheme today after attempting to reassure the UK’s financial markets.

The Bank launched the unprecedented intervention after the chancellor’s mini-budget caused chaos within the markets, as well as a potential pension pots crisis.

It promised to buy up to £65bn in government bonds – which are known as gilts – from those who wanted to sell them.

The government issues bonds to raise money for public spending, often used to service pension funds and the life insurance market.

Banks and big financial institutions that buy the gilts from the government at auction can sell them on to smaller financial institutions, traders or investors on the open market.

The price – or rate – at which they are bought and sold will be higher if investors think the government is able to repay the debt when the bond matures.

But when confidence in the UK economy falls, so does the bond price.

This increases the yield, the rate of interest, or the cost of borrowing, as investors seek to protect their money.

How much did the BoE spend on bonds?

The scheme launched by the Bank of England was designed to restore confidence in the government’s finances – increasing bond prices and decreasing the yields it has to pay on them.

Initially, the Bank’s intervention seemed to push down yields on these gilts.

But on Wednesday, yields had surged as high as 5.1%, the same level they reached before the Bank’s initial intervention.

As part of the programme, the Bank bought around £4.35bn of bonds on Wednesday and £4.7bn on Thursday in an increased effort to help soothe the markets.

It brings the total bond buying to £17.8bn.

Ultimately, it has helped to prop up pension funds at a time when they were already under a lot of strain from global financial pressures.

Another U-turn expected

Chancellor Kwasi Kwarteng and Prime Minister Liz Truss are now under pressure to reinstate a planned increase in corporation tax from April.

On Thursday night, the chancellor announced he would be returning to the UK from the US earlier than planned, amid growing expectations of a government U-turn on corporation tax.

The widely anticipated move appeared to reassure the finance industry after Bank of England Governor Andrew Bailey spooked the markets by insisting that the emergency support would not be extended.

Mr Kwarteng has also that there would be “no real cuts to public spending”, appearing to double down on comments made in the House of Commons by the PM on Wednesday.

The government’s plans revolve around securing an increase in economic growth – with a target of an annual rise of around 2.5% in gross domestic product.

The crucial date will be 31 October, when the forecasts presented by the Office for Budget Responsibility alongside the chancellor’s statement will give an assessmentof whether such a plan is realistic.

As a result of the government’s £45 billion in unfunded tax cuts, which were revealed last month and caused havoc in the markets, Prime Minister Liz Truss is facing an open uprising inside her own party.

The foreign secretary has declined to guarantee that the government will implement all of the tax cuts outlined in the disputed mini-budget presented by the chancellor.

James Cleverlytold Sky News “the package the chancellor put forward is pro-growth and is the right answer”.

He refused to rule out further changes, however, dodging multiple questions on whether the government will stick with its plan to scrap the rise in corporation tax.

Asked if there will be no more reversals of policy, Mr Cleverly told Kay Burley: “The chancellor is making a statement on the 31 October which gives a more holistic assessment of the public finances and our response to the global headwinds that every democracy, every economy in the world is facing.

“But as I say, the foundations of that mini-budget, protecting people from energy bill prices, letting people keep more of their earnings, protecting businesses from those energy prices, making sure we are internationally competitive, all those things are really key for the growth agenda the PM is putting forward.”

Probed again on whether the government will be sticking to its tax-cutting mini-budget, the foreign secretary replied that “ultimately, that mini-budget was about protecting tens of millions of people from unaffordable energy prices”.

Pressed specifically on the government’s plan to axe the increase in corporation tax from 19% to 25% in April, Mr Cleverly said: “Well, I mean the chancellor will come to the dispatch box…”

The foreign secretary added it is “absolutely right” the government helps businesses to “stay competitive” and “stay afloat”

“We have got to make sure we can compete internationally with the other places businesses can choose to locate. We have got to make sure we are tax-competitive.”

Prime Minister Liz Truss faces open revolt in her party over the government’s £45bn package of unfunded tax cuts, which unleashed chaos in the markets after it was announced last month.

Ms Truss and Kwasi Kwarteng, the chancellor, have said the cuts are needed to get Britain’s economy growing again, as data published on Wednesday suggested the country is heading for a recession.

Mr Kwarteng will meet with International Monetary Fund (IMF) leaders in Washington DC today after the institution’s chief economist said tax cuts threatened to cause “problems“ for the UK economy.

The IMF has said Britain’s priority should be tackling inflation rather than adding to the price problem through tax giveaways to achieve economic growth.

The prime minister and her chancellor have already been forced into reversing one of the many tax-cutting policies within their plan – scrapping the 45p tax rate for the highest earners.

In her first PMQs since the mini-budget last month, Ms Truss yesterday pledged not to cut public spending to balance the books – despite a leading economics-focused think tank warning the government is billions short of the sums needed.

The Institute for Fiscal Studies has warned the government would have to cut spending or raise taxes by £62bn if it is to stabilize or reduce the national debt as promised.

On Wednesday, Mel Stride, the Tory chairman of the Commons Treasury Committee, said that given Ms Truss’s commitments to protecting public spending, there was a question over whether any plan that did not include “at least some element of the further row back” on the tax-slashing package can reassure investors.

Tories must ‘get back to being fiscally responsible

“Credibility might now be swinging towards evidence of a clear change in tack rather than just coming up with other measures that try to square the fiscal circle,” Mr Stride warned.

While David Davis, the Tory former minister, called the mini-budget a “maxi-shambles” and suggested reversing some of the tax cuts would allow Ms Truss and Mr Kwarteng to avert leadership challenges for a few months.

The foreign secretary later warned Tory MPs against attempting to replace Ms Truss as prime minister.

“Changing the leadership would be a disastrously bad idea not just politically but economically,” he told BBC Radio 4’s Today programme.

Mr Cleverly also rejected an attack by former Tory leader Sir Iain Duncan Smith – who described Bank of England Governor Andrew Bailey as “stupid”.

“Of course, he is not stupid. You don’t get to be governor of the Bank of England if you are stupid,” the foreign secretary told Sky News.

“The job of the Bank of England is to intervene. He is doing his job. It doesn’t mean we always agree with everything the Bank of England governor says or does.”

The question of whether the Bank of England was correct to indicate the end of its market intervention was repeatedly avoided by the business secretary.

Although he stated his support for the Bank of England governor, Jacob Rees-Mogg challenged the idea that pension funds face “systemic” risk.

Speaking to Sky News, the business secretary said “of course” he has confidence in Andrew Bailey, describing him as “respected”.

He questioned, however, whether there was a “systemic problem” with pensions after the Bank of England expanded its market intervention to help pension funds for the second time in two days on Tuesday by buying up index-linked gilts.

The Bank had warned of a “material risk to UK financial stability” with “fire sales” of assets if it did not act.

The business secretary said that on the whole, pension funds “aren’t at risk”, but added: “Some pension funds have taken some high risk investments.”

He told Sky News that the “rightly independent” Bank intervened to protect these “risky investments”.

The Bank confirmed yesterday that its emergency support operation to protect pension funds would end this week.

Mr Rees-Mogg repeatedly refused to be drawn on whether the Bank was right to signal an end to its market intervention.

“I’m not going to criticise the Bank of England or the governor,” he said. “It is not for me to speculate on what the Bank of England is doing.”

He also insisted to Kay Burley that parts of the economy were in a “good state” as he admitted that after the economic turmoil of recent weeks his own mortgage payments have gone up.

“Mortgage rates have gone up for everyone who has a mortgage, and I have a mortgage,” he said.

“Any floating rate mortgages have gone up.”

Earlier this morning, new Office for National Statistics figures indicated that the economy shrank by 0.3% between July and August, a fall from downwardly revised growth of 0.1% the previous month.

Mr Rees-Mogg urged caution in interpreting them.

“The previous quarter’s figure showed a contraction [and] was then revised to show economic growth. So, be very careful about how you interpret figures immediately after they’re released,” he told Sky News.

“It’s a small amount of a very large economy, but these figures are notorious for being revised afterward.”

The business secretary also refused to indicate his own view on whether benefits should rise in line with inflation, an issue that has split the Conservative Party.

“We haven’t yet had the inflation figure on which benefits will be set. So, that is something that will be decided once the figure is available,” he said.

“Most predictions, most economic forecasts, turn out to be inaccurate rather than spot on. So, one has got to be careful about forecasts.”

Are we set for another era of austerity?

‘Routine decision-making’

Mr Rees-Mogg said the decision on benefits would be made once inflation figures come out.

“There is a process for making this decision,” he said.

“The statutory instrument has to be laid in November to put through the increase. That will be done in the normal way. This is completely routine governmental decision-making.”

In the Commons on Tuesday Julian Smith, a former cabinet minister, warned Kwasi Kwarteng, the chancellor, that the government must not balance tax cuts “on the back of the poorest people in our country”.

The government has already been forced to abandon plans to scrap the top 45p rate of tax in the face of a threatened revolt.

Liz Truss, the prime minister, will face MPs in the Commons on Wednesday for the first time since Mr Kwarteng’s £43bn tax-cutting mini-budget caused economic turmoil.

On Tuesday, the International Monetary Fund warned that Mr Kwarteng’s package of unfunded tax cuts was making it harder for the Bank to get soaring inflation rates under control.

The Institute for Fiscal Studies has warned the chancellor he will have to find £60bn in public spending cuts if he persists with his tax plans.

Pensions faced being wound up due to the turmoil in the markets following the mini-budget, the deputy governor of the Bank of England has said.

Sir Jon Cunliffe was writing in response to a letter from the chair of the Treasury Select Committee, Mel Stride.

In it, Sir John noted that the “first concerns” about the state of the economy came after the “growth plan” announced by Chancellor Kwasi Kwarteng on 23 September.

Sir John added that the following week, the Bank got news of “increasing severity” from the markets – including some types of pension funds that lend the government money and get paid back over decades.

On Tuesday night, the Bank was told by managers that somepension funds risked falling into “negative net asset values” – and may begin “the process of winding up” on Wednesday 28 September.

This would have had a knock-on effect and threatened “severe disruption of core funding markets and consequent widespread financial instability”, the deputy governor said.

Bank of England employees worked overnight to come up with a plan to buy some government debt to stabilise the market.

So far, £3.7bn worth of debt has been purchased by the Bank.

Santander and Yorkshire Building Society have now suspended mortgage deals after a fall in the pound fuelled forecasts of rising interest rates.

The lenders join Virgin Money and Skipton Building Society in halting mortgage offers for new customers.

Meanwhile, Nationwide said it will lift rates on a range of fixed mortgages.

On Tuesday, the Bank of England‘s chief economist said that action would have to be taken – an indication that interest rates could rise sharply.

In a speech, Huw Pill said: “I think it is hard not to draw the conclusion that all this will require a significant monetary policy response.”

Economists now expect interest rates to more than double to 5.8% by April, from the current level of 2.25%. Interest rates had previously been forecast to hit 4% by next May.

Lucian Cook, head of residential research at estate agency Savills, said fixed-rate mortgages were “incredibly difficult to price at the moment” because there is a lack of certainty over interest rates.

The number of residential mortgages on offer by lenders fell to 3,596 on Tuesday, compared with 3,961 deals on Friday when the government announced a mini-budget, according to financial information firm Moneyfacts.

Julie-Ann Haines, chief executive at Principality Building Society, said lenders had to “stress-test” mortgages to make sure that if the Bank of England base rates go up customers can still afford their monthly payments.

She said the reason mortgage rates were going up quite quickly in recent months was because banks and building societies have to be able to make a margin.

Economists began forecasting a hike in interest rates when the pound plunged against the dollar on Monday.

The Bank of England issued a statement on Monday saying that it would “not hesitate” to raise interest rates after the pound hit record lows.

Overnight, the pound stabilised at $1.08 but is still at its lowest level against the dollar for 37 years.

‘I just want a home’

Image source, Robin Price

Sales assistant Robin Price, who is on the minimum wage, has been saving up his mortgage deposit for years and thanks to that and an inheritance, is now ready to buy. But with the threat of a sharp rise in interest rates looming, he says he now feels completely lost.

“I just want a home,” says the 38-year-old, who fears monthly mortgage repayments will become unaffordable to him just when he wanted to buy his own place.

“I can’t find anywhere that I can afford a mortgage on in London or Essex because I don’t earn enough,” he says. “If I was in a couple it would probably be a different story.”

Mr Price moved out of his rental property to live with his sister in Suffolk while waiting to find somewhere to buy.

“Then Covid hit and I’m still struggling to find somewhere. I’m unsure what to do.”

Friday’s mini-budget offered help to first-time buyers by cutting stamp duty, the tax paid when people buy a property in England and Northern Ireland.

But any savings Mr Price could have made from this will be wiped out if interest rates more than double.

Mr Price says he is now looking at houses closer to his father in Norfolk, but fears he will not be able to get a mortgage deal.

The Chancellor’s plans will require a large increase in government borrowing.

Concerns among investors about the UK’s ability to pay that debt led to the value of the pound falling and pushed the cost of UK government borrowing to near record levels.

Experts said a rise in the cost of long-term borrowing meant the current cost to mortgage lenders of offering new deals was now more expensive.

There are also concerns that would-be borrowers will rush to secure mortgages at favourable rates before interest rates rise and if they do jump, homeowners will not be able to afford higher repayments.

A weaker pound makes imports and goods priced in dollars, such as oil, much more costly and risks fuelling price rises at a time when UK inflation is at its highest for 40 years.

Some 8.3 million people have mortgages in the UK, according to banking trade body UK Finance.

The Bank of England has already lifted interest rates seven times in a row since December to the highest rate in 14 years.

Samuel Tombs, chief UK economist at Pantheon Macroeconomics, said if interest rates rise as predicted, the average household refinancing a two-year fixed rate mortgage in the first half of next year would see monthly payments jump to £1,490 from £863.

“Many simply won’t be able to afford this,” he said.

Changes to mortgage deals include:

Santander is removing all 60% and 85% loan-to-value mortgages to new customers, and raising lending rates on new mortgages as well as on transfers

Yorkshire Building Society is withdrawing deals for new customers from Tuesday evening

Nationwide is increasing rates on two, three, five and 10-year fixed mortgages

Virgin Money and Skipton Building Society are halting deals for new customers

Halifax is removing mortgage products that come with a fee from Wednesday

Bank of Ireland is withdrawing all residential and buy-to-let rates

Yorkshire Building Society said: “As a result of the current volatile market conditions, we will be temporarily withdrawing our range of mortgages for new customers at 8pm tonight.

“All applications submitted prior to this will continue as normal.”

Virgin Money and Skipton Building Society also said applications that have been submitted will proceed.

Halifax said from Wednesday it would remove mortgage products that come with a fee “as a result of significant changes in mortgage market pricing we’ve seen over recent weeks”.

Mortgage deals that have product fees can result in lower monthly repayments for homeowners, with the fee being added to the total mortgage debt. The overall cost of the loan will be higher due to more interest accruing over time.

Madeline Ratcliffe, a journalist for Sky News, reports that the trading floor is calmer and traders are more at ease today, however one dealersays the market is still bumpy.

I spoke to the senior trader at Monex Europe, Michael Quinn, who told me the quieter markets today were because traders were digesting after initially being spooked by the mini-budget.

That said, the weak pound was a sign investors were losing faith in the UK economy.

“Foreign currency markets are far more driven by sentiment, than by economic reality,” he said.

He added that the Bank of England was “very conscious” of being seen to do a “bad interest rate hike”, or a panicked hike.

“There’s a very real risk that that would be seen as a panic move from the Bank of England, and that’s why they’re having to tread very carefully.

“Fundamentally, more than anything, the Bank of England needs the UK economy to start recovering and there’s only a limited amount that monetary policy can do to address that,” Mr Quinn continued.

“So as things stand at the moment, the situation from a markets perspective looks fairly grim because the general expectation is that the Bank of England is going to have to hike interest rates fairly sharply in a bid to combat inflation.

Some mortgage deals have been withdrawn by banks and building societies after a fall in the pound fuelled forecasts of a sharp rise in interest rates.

Virgin Money and Skipton Building Society halted mortgage offers for new customers while Bank of Ireland said it had withdrawn all mortgages.

Halifax said it would stop mortgages with product fees.

The Bank of England said on Monday it would “not hesitate” to hike interest rates after the pound hit record lows.

The pound plunged against the dollar on Monday after comments at the weekend from Chancellor Kwasi Kwarteng pledging more tax cuts, on top of Friday’s mini-budget when he announced the biggest tax cuts for 50 years. Overnight, the pound stabilised at $1.08 after hitting a record low of $1.03 on Monday.

The mini-budget plans will require a large increase in government borrowing and concerns among investors about the country’s ability to meet that debt led to the value of the pound being pushed down while the cost of UK government borrowing also soared.

Former US Treasury Secretary Larry Summers tweeted: “I was very pessimistic about the consequences of utterly irresponsible UK policy on Friday. But, I did not expect markets to get so bad so fast.”

A weaker pound also makes imports and goods priced in dollars, such as oil, much more costly and risks fuelling price rises at a time when UK inflation is at its highest for 40 years.

The Bank of England said it would make a full assessment as to whether it should change interest rates at its next meeting on 3 November, following speculation it might have intervened earlier.

Following Monday’s volatility, financial markets updated predictions and said interest rates could now more than double by next April to 5.8%, from their current level of 2.25%, to curb inflation – the rate at which prices for consumers rise. Interest rates had previously been forecast to hit 4% by next May.

Experts said a rise in the cost of long-term borrowing meant the current cost to mortgage lenders of offering new deals was now more expensive. There are also concerns that would-be borrowers will rush to secure mortgages at favourable rates before interest rates rise and if they do jump, homeowners will not be able to afford higher repayments.

Some 8.3 million people have mortgages in the UK, according to UK Finance, the trade association.

The number of residential mortgages on offer by lenders fell to 3,596 on Tuesday, according to financial information firm Moneyfacts, compared with 3,961 deals on Friday when the mini-budget was announced. It is also a sharp fall from the number available in December last year when the Bank of England started raising interest rates.

Julie-Ann Haines, chief executive at Principality Building Society, said: “As a lender what we need to do is one of two things. Firstly to make sure that customer mortgages are affordable. We have to do that under regulation and we therefore need to stress-test and make sure that if the Bank of England base rates go up that consumers can still afford their mortgage.