The Institute of Economic Affairs (IEA) has raised concerns over the Ghanaian government’s excessive borrowing from the domestic debt market, particularly at the short end, where investor demand remains high.

The think tank warns that this aggressive borrowing could trigger another economic crisis if not closely monitored and controlled.

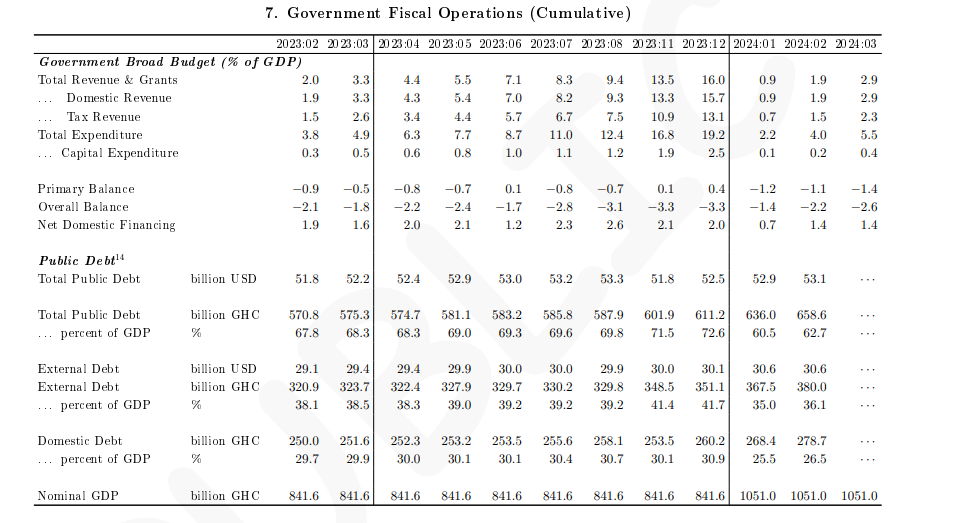

In its July-August 2024 Economic Outlook, the IEA revealed that Ghana’s domestic debt surged by GH¢32.7 billion, a 12.7% increase, from GH¢257.3 billion to GH¢290.0 billion within the year leading up to June 2024.

In contrast, the external debt component saw only a modest rise of US$0.9 billion, or 0.3%, from US$30.1 billion to US$31.0 billion over the same period.

While the government’s reliance on domestic borrowing is understandable—given its lack of access to the international bond market—the IEA cautioned that such borrowing must be carefully managed to avoid exacerbating the country’s debt situation.

As of June 2024, Ghana’s total public debt reached GH¢742.0 billion, marking a year-to-date increase of GH¢133.6 billion, or 22.0%. In dollar terms, this equated to US$50.9 billion, down from US$52.2 billion at the end of December 2023, largely due to the depreciation of the cedi impacting the domestic debt component.

Despite the surge in domestic borrowing, the debt-to-GDP ratio decreased slightly to 70.6% in June 2024, from 72.3% at the end of 2023. This was attributed to an increase in nominal GDP. However, under the International Monetary Fund’s (IMF) Economic Credit Facility (ECF) programme, Ghana’s public debt is projected to rise to 82.5% of GDP by the end of 2024, according to the IMF’s Executive Board review in June 2024.

The IEA expressed surprise at this high projection, given that the debt restructuring efforts and fiscal consolidation under the ECF were initially expected to bring Ghana’s debt down to a sustainable level of around 56% by 2028.

“It is not clear whether this sustainable target is still attainable,” the IEA concluded.