OmniBSIC Ghana Ltd offered the lowest interest rate of 33.06 percent on loans to Small and Medium Enterprises (SMEs) with a tenure of 5 years in March 2024, according to a recent report from the Bank of Ghana.

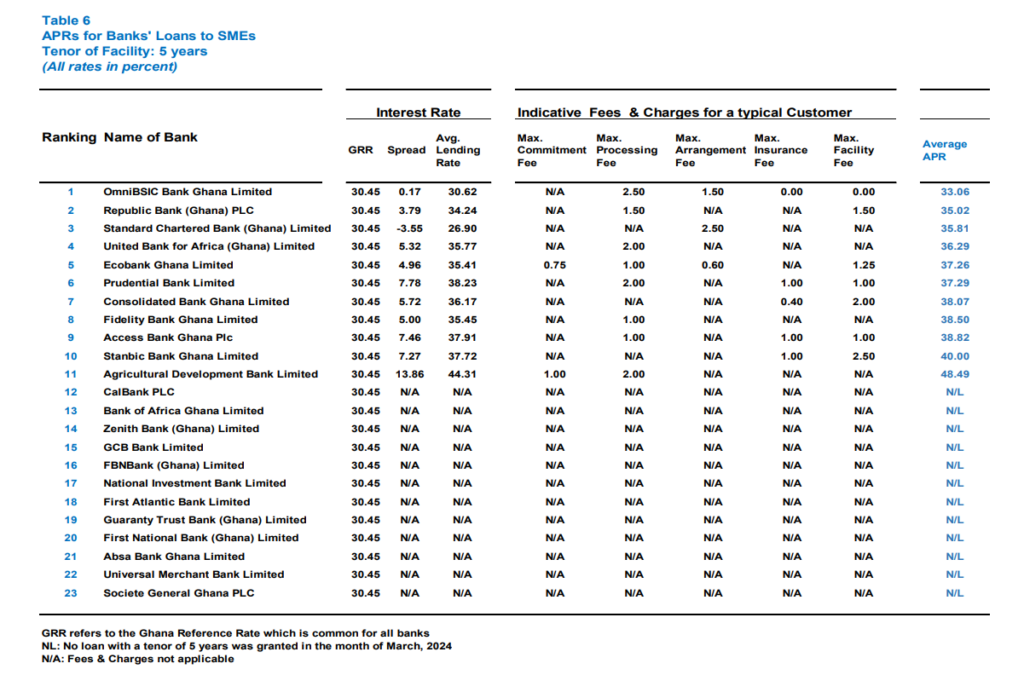

Following closely behind, Republic Bank provided loans at a rate of 35.02 percent, while Standard Chartered Bank offered loans at 35.81 percent under the same tenor.

The Annualized Percentage Rate (APR) report, released by the Bank of Ghana in April 2024, surveyed interest rates offered by 23 banks operating in the country.

“The APR reflects the true cost of a loan that economic agents are confronted with when they go through an approval process to secure a loan facility. It comprises the Ghana Reference Rate, bank specific risk-premia and other bank-specific charges” the Bank of Ghana said.

Fitch Solutions predicts potential upward risks to Ghana’s interest rate outlook, pointing to geopolitical tensions and disruptions in global trade that may result in higher commodity prices.

In their recent article titled “More Interest Rate Cuts On The Way In Ghana, Following Cautious Start Of Easing Cycle,” they suggest that Ghana, being a net importer of fuel and food items, could face increased import costs, which could disrupt the disinflation process.

The report underscores the risk of stalled negotiations between Ghana and its commercial creditors, which could potentially delay International Monetary Fund (IMF) disbursements and undermine investor confidence.

Such a scenario could lead to a sell-off of the cedi and a resurgence of inflation, prompting the Bank of Ghana to adopt a more conservative monetary easing cycle than initially anticipated.

Despite these concerns, interest rates in Ghana have generally remained stable. According to the Bank of Ghana, there has been a downward trend in rates at the short end of the yield curve.

In December 2023, the 91-day and 182-day Treasury bill rates decreased to 29.49% and 31.70%, respectively, compared to 35.48% and 36.23% in the corresponding period of 2022. Similarly, the rate on the 364-day instrument decreased to 32.97% in December 2023 from 36.06% in December 2022.

On November 28, 2023, the Bank of Ghana reported the interbank forex rates, revealing that the Ghana Cedi trades against the dollar at a buying price of 11.5842 and a selling price of 11.5958.

In Accra’s Forex bureaus, the dollar is bought at a rate of 12.05 and sold at 12.25. Against the Pound Sterling, the Cedi is traded at a buying price of 14.6169 and a selling price of 14.6327.

In Accra’s Forex Bureau, the pound sterling is bought at a rate of 14.90 and sold at a rate of 15.40.

The Euro is trading at a buying price of 12.6696 and a selling price of 12.6822. In Accra’s Forex Bureau, the Euro is bought at a rate of 12.85 and sold at a rate of 13.35.

The South African Rand is trading at a buying price of 0.6193 and a selling price of 0.6199. In a forex bureau in Accra, the South African Rand is bought at a rate of 0.40 and sold at a rate of 1.10.

The Nigerian Naira is trading at a buying price of 71.3063 and a selling price of 71.3891.

In a forex bureau in Accra, the Nigerian Naira is bought at a rate of 9.00 Naira for every 1 Cedi and sold at a rate of 15.00. For the CFA, it is trading at a buying price of 51.7227 and a selling price of 51.7741.

In a forex bureau in Accra, the CFA is bought at a rate of 17.30 CFA for every 1 Cedi and sold at a rate of 19.80 CFA for every 1 Cedi.

Among some top 15 African nations, Ghana is said to have the highest interest rates, surpassing that of Egypt.

The rates for the 91-day and 182-day treasury bills were approximately 24.39% and 26.03%, respectively, according to the Weekly Fixed Income Update put together by several investment firms, making Ghana the highest rates among the sampled leading African economies.

Egypt followed Ghana closely with a 91-day Treasury bill rate of 23.41%, whilst the 182-day T-bill is going for 24.02%.

Its currency – the Egyptian Pound – has also been recording rapid depreciation to the dollar.

Seychelles has the lowest interest rates of about 0.95% among the top African countries and is followed by Nigeria with 2.87%.

The Domestic Debt Exchange Programme (DDEP) caused Ghana’s rates to drop dramatically in March 2023, but since then they have steadily increased to about 30% (364-day bill), ranking them among the highest in the world. Since March 2023, the 91-day bill and 182-day bill have decreased by 10.97% and 9.95%, respectively.

Ghana has some of the highest average lending rates on the African continent, at about 38%.

As the government looks for extra liquidity to finance its initiatives, the majority of analysts have forecast an increase in interest rates in the upcoming week. This follows from the Bank of Ghana’s Open Market Operations bills having competitive returns.

In fact, due to the inflation’s unrelenting pace, actual returns on short-term securities are now negative.

Although some analysts have stated that any such move may have an impact on the real sector of the economy, it is uncertain whether the Bank of Ghana will hike its Monetary Policy Rate from the present 29.5% in order to help mop up surplus cash in circulation to manage inflation.

An appeal has been made by the newly-appointed Vice President-Confederation for the Development of Poultry in Africa (CADA), Mr. John Bewuah Edusei, calling for commitment to revive the local poultry industry and the agricultural industry as a whole.

This, he said, should be done while shunning the political gimmickry that has characterised successive governments’ policies on the sector, especially in the face of threatening global food insecurities.

He cautioned that the country’s failure to transform the agriculture sector could result in hunger and famine, especially due to a ‘population explosion’.

According to the 2022 United Nations Population Division forecast, the future population of the world’s countries – based on current demographic trends – will reach 9.7 billion people by 2050 and 10.9 billion by 2100.

Meanwhile, a greater proportion of this population growth is expected to come from the African continent.

It is against this background that Mr. Edusei cautioned that a great famine beckons the continent if leadership do not take pragmatic steps in domesticating agricultural products.

“The time to plan is now. We either plan towards 2050 today and stop the games and politics or be ready to face the consequences of our actions tomorrow,” he stated.

The Vice President of CADA, who was speaking at a media engagement in Kumasi on his return from the CADA conference in Morocco, stated that: “Nobody knows when the next disaster will strike this world; we need to plan and ensure food security before it is too late.

“If dry Morocco and Burkina can grow their food requirements, green Ghana must do better in maize and chicken production,” he added.

He said Ghana will have to do more to feed its citizenry as the forecast emphasises animal-based protein, especially from poultry products.

“Poultry will have to play a major role going forward. But where are the poultry farms today? It becomes obligatory for us to have a systematic and sustainable development poultry growth plan…All our major layer-farms are down, and our broiler production is below 2 percent of national requirements,” he lamented.

Furthermore, he mentioned that some farms have declined from a capacity of 800,000 birds to less than 20,000 – noting the situation as worrying, “but the worst part of it is the exceptionally high job losses”.

Ghana’s chicken imports, according to Mr. Edusei, have almost doubled from US$375million in 2018 – noting that government has failed in curbing the high importation figures, leading to rampant job losses locally.

However, he acknowledged that the ‘Planting for Food and Jobs’ (PFJ) programme increased maize production; but insisted that the successes will be useless unless it is linked with a robust plan for pricing, storage and marketing.

He advocated that it is time to buy the produce at a good price from farmers, store them in our silos and market it all year round.

“The earlier as a nation we start with strategic programmes to systematically increase maize and poultry production, the stronger we will be to face the consequences of population hikes in 2050 and beyond,” he stated.

The purpose of CADA is to promote the poultry industry in Africa, through training and defending the interests of African poultry players through strategic programmes.

It also aims to promote and develop Modern Poultry Farming. This materialises the common vision of establishing a systematic growth in African poultry all over the African continent.

Evidence suggests that UK and US authorities were informed of a state-led effort to “rig” interest rates during the 2008 financial crisis but chose to conceal it.

Documents indicate that lenders significantly lowered their anticipated interest rates in response to central banks’ pressure.

Bankers were imprisoned for smaller-scale interest-rate “rigging” but juries were not presented with any evidence at that time.

Regulators said they had followed disclosure rules, declined to comment or in one case rebutted the claims.

Some evidence has previously emerged of Bank of England and UK government involvement in manipulation of interest rates. But the evidence indicating it was part of a broader, international drive not just by the UK but by central banks across the western world to push key interest rates down in October 2008 has never been published before.

The evidence indicates that in October 2008, central banks including the Bank of England, the Banque de France, the European Central Bank, Banca d’Italia, Banco de Espana and the Federal Reserve Bank of New York intervened on a large scale in the setting of Libor and Euribor.

At the height of the 2008 financial crisis, when bank lending had almost ground to a halt, central banks around the world urged calm. But my investigation reveals evidence that, behind the scenes, they were pulling levers to restore calm artificially – measures which would later be ruled to be against the law in the UK.

Those measures related to benchmark interest rates called Libor and Euribor, which track how much it costs banks to borrow money from each other. As such they are a big influence on the cost of mortgages and other loans. The more confidence investors had in the borrowing bank, the lower the rate. The higher the rate, the more doubts the market had about the viability of that bank.

In October 2008 there was an international drive, involving the central banks of the UK, US and eurozone, to get Libor down and restore a sense of calm to the market, at a time when banks lending had almost ground to a halt.

In November 2010, investigating agencies from the US Federal Bureau of Investigation (FBI) to the UK financial regulator were directly informed of this – but they have since kept it secret from Parliament, Congress and the public.

Andrew Tyrie, who chaired the UK Treasury Committee of MPs when it enquired into Libor in 2012, told the BBC that he believed Parliament “appears to have been misled”.

“The evidence that Mr Verity has unearthed strongly suggests that the committee’s inquiry into the Libor scandal was not told the whole truth.

“The public rely on Parliament to get to the truth. This case illustrates why Parliament should bolster its information-gathering powers with more effective sanctions against those who provide less than the full picture. Parliament appears to have been misled and, if that’s the case, should not let it rest.”

I uncovered extracts from the transcript of an interview given by Barclays cash trader Peter Johnson whilst researching a book I have written about the secret history of the interest rate rigging scandal.

The interview was given on 19 November 2010 to the US Department of Justice, the FBI, other US regulators, and the UK’s financial regulator, then called the Financial Services Authority (FSA).

While 37 traders and brokers have been prosecuted by the US Department of Justice and the UK’s Serious Fraud Office, jurors in nine criminal trials for much smaller-scale interest rate “rigging” held in London and New York between 2015 and 2019 were never shown this evidence.

Backed up and supplemented by published data, the suppressed evidence indicates that in October 2008, central banks intervened on a large scale in the setting of Libor and Euribor.

Further suppressed evidence indicates that the UK government, including 10 Downing Street, was also involved in pressuring banks to “manipulate” Libor as defined by the criminal courts – meaning seeking to obtain movements in the benchmark rate while “disregarding the proper basis for setting Libor”.

Nineteen traders have been convicted and nine jailed because of court rulings that outlawed any influence on Libor apart from the interest rates on offer on the money markets at which a bank could borrow and lend cash.

If they allowed its setting to be influenced by other factors, such as the desire to avoid bad publicity or to help a bank’s market trades, they could be jailed for interest rate “manipulation”.

Call for fresh investigation

Speaking in Parliament, senior Conservative MP David Davis said: “I’m greatly concerned the Treasury Select Committee may have been misled by state agencies about the knowledge and involvement of the state in setting false rates. It’s a big and complex issue with hundreds of pages of evidence.”

Mr Davis said that in the light of the evidence he’d seen there was “a case to believe that state agencies coerced individuals into perjury that led to false convictions”.

Mr Davis added he would ask the Met Police to investigate potential perjury, but also called for the Treasury Select Committee to investigate his concern that Parliament may have been misled.

Image caption,Peter Johnson was interviewed by the FBI

Among the evidence suggesting a cover-up, is a recording from 2010 of FBI investigator Mike Kelly interviewing Peter Johnson, who submitted Libor rates on behalf of Barclays bank.

Mr Johnson said in October 2008 he was instructed by his bosses to submit artificially low Libor rates, far below the real interest rates on offer in the market – under pressure from the Bank of England and the UK government.

In the recording, Mr Kelly asked Mr Johnson: “Did you have any understanding as to why this pressure was being put upon Barclays?”

“I’m not sure that it was being put just on Barclays,” replied Mr Johnson.

“OK? Who else did you think, was being pressured?”

“We understood that the French banks had been told to get their rates down[…]”

“What entity was pressuring them?”

“We believe it was the Banque du France.”

Record rate falls

That information – never mentioned by regulators to Parliament nor Congress – is corroborated and supported by the published data on Euribor submissions from the time.

They show that following a co-ordinated cut in official rates by six central banks on 8 October 2008, there were also record falls in banks’ estimates of the cost of borrowing euros by French banks – moves only explicable as having been co-ordinated at a national level.

Because the vast majority of the other 40 banks whose Euribor submissions were monitored held rates steady, market factors could not explain the record moves.

Between 8 and 9 October, BNP Paribas cut its Euribor rates by 0.4% in a day – larger than the 0.35% move following the terror attacks of 11 September 2001. In the money markets, Euribor submissions rarely move by more than 0.1% per day.

Over the next three working days unprecedented moves happened at other banks:

French bank Credit Agricole dropped its Euribor estimates of the cost of borrowing euros over three months by 0.38%

Societe Generale dropped the same Euribor rate by 0.42%

Credit Industriel et Commercial dropped by 0.43%

HSBC’s French division dropped by 0.48%

Italian bank Intesa Sanpaolo dropped its rate for borrowing euros over three months in unusually round figures, of 0.1% per day over three days.

On the weekend of 11-12 October 2008, then UK Prime Minister Gordon Brown flew to Paris for an emergency summit with European leaders, including then European Central Bank president Jean-Claude Trichet, all of whom issued statements calling for the need for “co-ordinated” action to tackle the crisis.

Following the weekend summit, Banca Monte dei Paschi di Siena caught up, dropping its rates by an unprecedented 0.4% in a day. Spain too showed similar record drops.

Mr Johnson also pointed investigators to a below-market offer in the dollar Libor market in New York made by JPMorgan Chase in late October 2008.

Interviewing him in November 2010, the US regulator confirmed it had seen data that Chase New York had offered to lend at 4.68% – while putting in a Libor estimate of the cost of borrowing dollars that was much lower – at 3.25%.

Mr Johnson said he believed the offer to lend at a rate still far below the market, mid-crisis, when other lenders were refusing to lend any cash, was done at the urging of the Federal Reserve Bank of New York.

“Were there rumours surrounding Chase at that time?” asked Anne Termine, an investigator for US regulator the Commodity Future Trading Commission.

“Yes,” Mr Johnson replied.

“That the Fed had asked it to lend money into the market.”

However, the US authorities appear not to have investigated the US central bank’s rumoured intervention in their final notices for Barclays. Mr Johnson was asked no further questions and the Department of Justice’s final notices fining banks for Libor manipulation made no mention of any US central bank intervention.

None of this evidence was made public in press notices and statements of fact published by regulators as they prosecuted 37 traders and fined banks $8.8bn for rigging Libor and Euribor. None of the jurors were made aware of it.

The Treasury said it did not seek to influence individual bank Libor submissions.

The Financial Conduct Authority told the BBC it had met its disclosure obligations.

The Bank of England has previously referred to the allegations as “unsubstantiated”.

The FBI and the CFTC declined to comment.

The European Central Bank (ECB) said they “strongly rebut” the assertions which they say, without giving details, “misrepresent the role of a central bank in implementing monetary policy”. They also said that ECB has always acted in line with its mandate and in full compliance with applicable law”

Italian bank Intesa Sanpaolo said it had always acted independently and in full compliance with the rate-setting rules.

The Bank of England hikes interest rates as it indicates the UK is already in recession; government hints energy support for schools, hospitals, and care homes could continue beyond six months; submit your cost of living dilemma to personal finance expert Gemma Godfrey using the form below.

What is a recession?

It is a significant decline in economic activity, lasting months or even years.

Economists usually define a recession as two consecutive quarters where GDP has fallen.

Why do recessions happen?

There are a number of common causes for recession, including:

A sudden economic shock – such as the COVID pandemic or the war in Ukraine

Excessive debt

Asset bubbles – when investors become too optimistic and inflate the stock market or real estate bubbles, before the bubble bursts and panic selling ensues

Many people will also remember the Great Recession of 2008 and 2009 – the UK’s worst in modern history.

This was largely due to the mortgage crisis in the US impacting the British banking sector, and the subsequent “credit crunch”.

The UK also saw a recession between 1990 and 1991, caused by rapid economic expansion under Margaret Thatcher and Britain’s plans to maintain membership of the Exchange Rate Mechanism.

How will a recession affect you?

Unemployment levels will rise, so more people will be at risk of losing their jobs.

People who keep their jobs may see cuts to pay and benefits, or struggle to negotiate future pay rises.

Meanwhile, investments can lose money and savings can be reduced, upsetting some people’s plans for retirement or for large expenses such as buying homes or getting married.

Businesses make fewer sales during a recession, and mortgage lenders can also tighten standards for mortgages, car loans and other types of financing – meaning you may need a better credit score or larger down payment.