IMF’s Executive Board has completed a review of its surcharge and lending policies, resulting in a reduction in borrowing costs.

In a statement, IMF Managing Director Kristalina Georgieva highlighted that, amidst the current global economic challenges and rising interest rates, member countries have agreed on a comprehensive plan to significantly lower borrowing costs.

This initiative aims to maintain the IMF’s ability to assist countries in need while offering relief to borrowers by reducing financial pressures.

She said: “The approved measures will lower IMF borrowing costs for members by 36 percent, or about US$1.2 billion annually,” explaining: “The expected number of countries subject to surcharges in fiscal year 2026 will fall from 20 to 13.”

“This is achieved by reducing the margin over the SDR interest rate, raising the threshold for level-based surcharges, lowering the rate for time-based surcharges, and increasing the thresholds for commitment fees,” Ms Georgieva noted.

The approved package will take effect on November 1, 2024.

“While substantially lowered, charges and surcharges remain an essential part of the IMF’s cooperative lending and risk management framework, where all members contribute and all can benefit from support when needed,” she pointed out.

She said: “Together, charges and surcharges cover lending intermediation expenses, help accumulate reserves to protect against financial risks, and provide incentives for prudent borrowing.”

“This provides a strong financial foundation that allows the IMF to extend vital balance of payments support on affordable terms to member countries when they need it most,” explained the MD.

“This reform helps ensure that the IMF can continue serving our members in a changing world,” she mentioned.

The International Monetary Fund (IMF) has forecasted that the introduction of Artificial Intelligence (AI) will impact 40 percent of the global workforce.

While AI has demonstrated improvements in productivity, it is poised to displace numerous jobs in the foreseeable future.

Speaking at the sidelines of the 2024 IMF-World Bank Spring meeting in Washington DC, Managing Director of the Fund, Kristalina Georgieva emphasized the permanent presence of AI.

She cited an IMF study revealing that AI’s influence could extend to 40 percent of jobs worldwide, with advanced economies potentially facing a 60 percent impact.

Georgieva highlighted the dual nature of AI, stating it could enhance worker productivity while simultaneously posing a threat to employment. She stressed the importance of investing in digital infrastructure, skills development, and robust social safety nets to shape the pace of AI adoption and its ramifications on productivity.

Furthermore, the IMF’s January report outlined potential ramifications on income and wealth inequality within countries due to AI.

It posited that AI might lead to polarization within income brackets, benefiting workers adept at leveraging AI while leaving others behind.

The report suggested that younger workers might find it easier to capitalize on AI opportunities, while older workers might face challenges in adaptation.

Additionally, the report noted that AI’s impact on labor income hinges on its complementarity with high-income workers.

If AI significantly complements higher-income workers, it could disproportionately increase their labor income and favor high earners. This scenario, coupled with gains in productivity from AI adoption boosting capital returns, could exacerbate inequality.

In light of these findings, the IMF stressed the need for proactive policymaking to mitigate the potential exacerbation of inequality by AI.

It advocated for establishing comprehensive social safety nets and offering retraining programs for vulnerable workers to ensure an inclusive AI transition that safeguards livelihoods and curbs inequality.

“A recent IMF study shows that artificial intelligence could affect up to 40 percent of jobs across the world and 60 percent in advanced economies.

“It could enhance workers’ productivity but also threatens some jobs. Investing in digital infrastructure and skills, as well as in strong social safety nets will determine the pace of AI adoption and its impact on productivity.”

The IMF in January this year also predicted that “AI could also affect income and wealth inequality within countries. We may see polarization within income brackets, with workers who can harness AI seeing an increase in their productivity and wages—and those who cannot falling behind. Research shows that AI can help less experienced workers enhance their productivity more quickly. Younger workers may find it easier to exploit opportunities, while older workers could struggle to adapt.

“The effect on labour income will largely depend on the extent to which AI will complement high-income workers. If AI significantly complements higher-income workers, it may lead to a disproportionate increase in their labour income. Moreover, gains in productivity from firms that adopt AI will likely boost capital returns, which may also favour high earners. Both of these phenomena could exacerbate inequality.

“In most scenarios, AI will likely worsen overall inequality, a troubling trend that policymakers must proactively address to prevent the technology from further stoking social tensions. It is crucial for countries to establish comprehensive social safety nets and offer retraining programs for vulnerable workers. In doing so, we can make the AI transition more inclusive, protecting livelihoods and curbing inequality.”

Ms. Georgieva was the sole candidate nominated for the position.

The Board’s decision followed a series of discussions, including with Ms. Georgieva, in accordance with the selection process established on March 13, 2024.

After the meeting, the Executive Board Coordinators, Mr. Afonso S. Bevilaqua and Mr. Abdullah F. BinZarah, issued a statement.

“In taking this decision, the Board commended Ms. Georgieva’s strong and agile leadership during her term, navigating a series of major global shocks. Ms. Georgieva led the IMF’s unprecedented response to these shocks, including the approval of more than $360 billion in new financing since the start of the pandemic for 97 countries, debt service relief to the Fund’s poorest, most vulnerable members, and a historic Special Drawing Rights (SDR) allocation equivalent to $650 billion. Under her leadership, the Fund introduced innovative new financing facilities, including the Resilience and Sustainability Facility and the Food Shock Window. It replenished the Poverty Reduction and Growth Trust, with the capacity to mobilize concessional loans to its poorest members, and co-created the Global Sovereign Debt Roundtable. It also secured a 50 percent quota increase to bolster the Fund’s permanent resources and agreed to add a third Sub-Saharan African chair to the IMF Board.

“Looking ahead, the Board welcomes Ms. Georgieva’s ongoing emphasis on issues of macroeconomic and financial stability, while also ensuring that the Fund continues to adapt and evolve to meet the needs of its entire membership. It recognizes her focus on strengthening the Fund’s support to its members through effective policy advice, capacity development and financing. The Board looks forward to continuing to work closely with the Managing Director.”

Ms. Georgieva has been serving as Managing Director of the IMF since October 1, 2019. In this role, she is the head of the IMF’s operational staff and chairs the Executive Board.

Ms. Georgieva is supported by four Deputy Managing Directors in overseeing the Fund’s operations, which involve approximately 3,100 staff members.

A Bulgarian national, Ms. Georgieva has held various prominent positions prior to her role at the IMF. She was previously the Chief Executive Officer of the World Bank from January 2017.

Additionally, she served as the Interim President for the World Bank Group from February 1, 2019, to April 8, 2019. Ms. Georgieva also has a background in the European Commission, where she held roles such as Commissioner for International Cooperation, Humanitarian Aid, and Crisis Response, as well as Vice President for Budget and Human Resources.

Ms. Georgieva’s academic qualifications include a Ph.D. in Economic Science and a M.A. in Political Economy and Sociology from the University of National and World Economy in Bulgaria. She also taught at the same university from 1977 to 1991.

I appreciate the opportunity today to speak on behalf of my fellow Governors about “Bolstering Africa’s Financing through the Overlapping Crises and Beyond.”

Let me first express my heartfelt gratitude to the Managing Director, Madam Kristalina Georgieva, for your excellent leadership, and your strong support for Africa. Madam MD, Africa continues to face complex challenges against the backdrop of successive shocks, manifesting in a subdued post-pandemic recovery, elevated debt distress, and a persistent funding squeeze, that have amplified income divergences and undermined the achievement of sustainable and inclusive growth.

My colleague Governors, our domestic adjustment policy efforts without adequate financing can only yield limited results, in the context of the complex domestic and external environment.

As such, stronger support from the development partners, including the IMF, remains paramount. Considering the low catalytic effect of Fund financing, many of our countries view the countercyclical role of Fund financing as indispensable.

To this end, Madam Managing Director, we highlight the following points for your consideration:

First, we view continued pragmatism and agility of IMF’s policies to changing global conditions as paramount to better serve its vulnerable members.

To this end, we underline the necessity for the upcoming comprehensive review of LICs facilities to maintain the PRGT’s concessionality and promote higher access to reverse erosion amplified by the global inflationary episode. We also underscore the criticality of replenishing the CCRT resources envelope to offer grant support to our most vulnerable members in this shock-prone world.

Considering the expiry of the Food Shock Window amidst a food crisis triggered by the El Nino phenomenon, Fund emergency financing alongside augmentations in program countries would be important to close climate induced financing gaps. In this regard, we call for intensified fundraising efforts under the second phase of the resource mobilization initiatives.

Second, we call for meaningful collaboration between the IMF and the World Bank to better align their support to LICs. In this regard, we stress the need for coordination of the IMF’s LIC Facilities Review with the World Bank’s IDA21 replenishment efforts to support LICs in a holistic manner.

Third, we stress the need to keep all financing options on the table, including the use of the Fund’s internal resources. In view of the recent multiple shocks and a crisis like no other, now is the opportune time for a modest gold sale, particularly when gold prices are still favorable.

Finally, we restate our request for further enhancements to the G20 Common Framework while leveraging the Global Sovereign Debt Roundtable (GSDR) to promote rapid, transparent, and equitable resolution of debt as well as facilitate debt cancellation for the most vulnerable members. The review of the Fund’s internal debt policies is welcome, but we stress the need to ensure that the changes are impactful and achieve their intended purpose.

Global Financial Stability Report by the IMF for April 2024, has it that companies have historically faced relatively moderate direct losses from cyberattacks, but some have encountered significantly heavier burdens.

For instance, the US credit reporting agency Equifax paid over $1 billion in penalties following a major data breach in 2017, affecting approximately 150 million consumers.

The report highlights an escalating risk of severe losses from cyber incidents, potentially leading to funding challenges for companies and even endangering their financial stability. These extreme losses have surged to $2.5 billion since 2017, quadrupling in size. Additionally, indirect losses such as reputational harm or security enhancements are substantially higher.

The financial sector is particularly vulnerable to cyber risk due to the vast amounts of sensitive data and transactions it handles, making it a prime target for criminals aiming to steal funds or disrupt economic operations. Attacks on financial institutions constitute nearly one-fifth of the total, with banks being the most susceptible.

Incidents within the financial sector pose a threat to financial and economic stability by undermining confidence in the financial system, disrupting essential services, or triggering cascading effects on other institutions.

For instance, a significant incident at a financial institution could erode trust and potentially lead to market turmoil or bank runs. While no major “cyber runs” have occurred thus far, analysis suggests minor yet somewhat persistent deposit outflows at smaller US banks following cyberattacks.

Cyber incidents disrupting critical services such as payment networks could severely impact economic activity. For instance, a December attack on the Central Bank of Lesotho disrupted the national payment system, halting transactions by domestic banks.

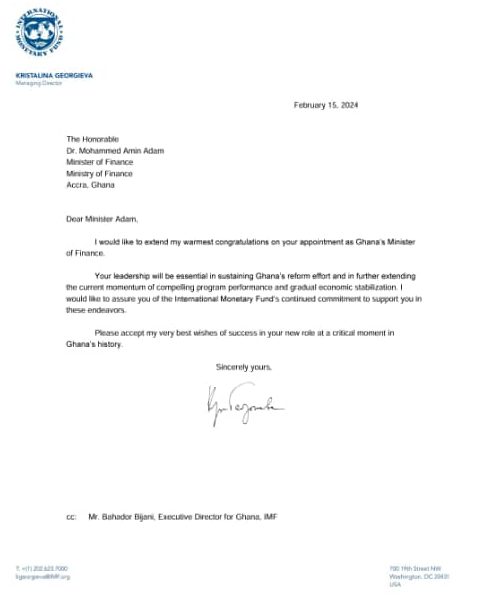

The Managing Director of the International Monetary Fund (IMF), Kristalina Georgieva, has advised the newly appointed Minister of Finance, Dr. Mohammed Amin Adam, to maintain the efforts of the country’s economic reform program.

In a congratulatory letter, Ms. Georgieva emphasized the importance of Dr. Amin Adam’s leadership in continuing the momentum of the IMF program to achieve economic stability and meet its targets.

Ms. Georgieva highlighted the significance of guidance in driving the reform effort forward, stating, “Your leadership will be essential in sustaining Ghana’s reform effort and in further extending the current momentum of compelling program performance and gradual economic stabilization.”

Expressing support, she assured the Minister that the IMF would collaborate with him to contribute to Ghana’s economic recovery. The letter concluded with warm wishes for success in Dr. Amin Adam’s new role.

Ghana is currently implementing a three-year program with the IMF, aiming to receive a $3 billion support fund.

The country has already received a second tranche of funding totaling $600 million, following the initial $600 million to support the Balance of Payment account.

Dr. Mohammed Amin Adam, an Economist and Energy and Petroleum Policy Expert, has an extensive educational background, including a Ph.D. in Energy and Petroleum Economics from the University of Dundee. He has over 25 years of experience in political management, administration, and key roles in the Government of President Nana Akufo-Addo. Dr. Adam is recognized globally for his expertise and has served in various advisory capacities for international organizations and African countries.

The Managing Director of the International Monetary Fund (IMF), Kristalina Georgieva, has expressed her approval of the new Finance Minister, Dr. Mohammed Amin Adam.

She emphasized the importance of Dr. Amin Adam’s leadership in maintaining Ghana’s reform initiatives and building upon the ongoing positive trajectory of program performance and economic stabilization.

Kristalina Georgieva urged Dr. Adam to take the lead in restoring stability to Ghana’s economy.

Dr. Mohammed Amin Adam, previously the Minister of State at the Finance Ministry, was promoted to the substantive Minister for the Finance Ministry in the recent reshuffle, replacing Mr. Ken Ofori-Atta.

In her congratulatory statement, the IMF boss stated, “Your leadership will be essential in sustaining Ghana’s reform effort and in further extending the current momentum of compelling program performance and gradual economic stabilization. I would like to assure you of the International Monetary Fund’s continued commitment to support you in these endeavors.”

Ghana, which has received a $3 billion International Monetary Fund (IMF) support package, is currently in the midst of its inaugural program evaluation, scheduled to wrap up by November, according to the Managing Director of the IMF, Kristalina Georgieva.

During a comprehensive interview, Georgieva expressed her positive outlook regarding Ghana’s economic advancements, highlighting a significant upturn in the country’s financial situation in the past month.

Additionally, in her discussion, Kristalina Georgieva commented on the progress being made by Zambia and Ghana, both of which have experienced debt defaults, within their respective IMF programs.

She also noted that while Tunisia doesn’t require a restructuring at this point, the country should take prompt actions to strengthen its economy.

“Ghana is doing actually quite well. You have seen that their position has improved over the last month, the economy is in a much better place.

“I would very much hope that we can have the disbursement,” she said referring to a $600 million tranche of IMF money that’s due to be disbursed in November.

“That is part of the confidence building that we are projecting,” she said regarding Ghana’s economic stability.

In her broader comments, Georgieva underscored the importance of tackling unsustainable debt crises as a “high-priority” issue.

She offered a defense of the G20 Common Framework for debt resolution, even in the face of criticism regarding its perceived slow response in providing relief to eligible nations.

Georgieva noted that as more countries seek assistance, the process has become more streamlined, with Chad, Zambia, Sri Lanka, and Ghana all showcasing shorter timeframes for achieving progress.

She highlighted specific examples, noting that Chad took 11 months from the initial staff-level agreement to financial assurances, Zambia accomplished this in nine months, Sri Lanka in six months, and Ghana in just five months.

“I hear lots of people saying, oh this doesn’t work,” she said.

“My question to them is, ok, you forget about it. What do you have instead?”

In the meantime, the IMF Managing Director emphasized that Egypt’s precious reserves will continue to dwindle unless the country opts for another currency devaluation. She commended other measures that Egypt, the IMF’s second-largest borrower, has taken to address its struggling economy.

Since early 2022, Egypt has devalued its currency three times, resulting in a nearly 50% depreciation against the US dollar.

Georgieva argued that delaying another devaluation is only postponing the inevitable, and the longer Egypt refrains from taking this step, the more challenging the situation will become.

“The sooner we can reach an agreement on the road map for this the better,” she said.

“The issue here is very simple. Egypt would bleed reserves protecting the pound and neither the country nor overall the environment is such that this is desirable. That’s a problem that has to be solved.”

Egypt’s net international reserves experienced a decline last year, reaching their lowest point since 2017, before showing signs of stability in recent months and reaching $35 billion in September. However, this figure remains more than one-fifth lower than its peak in 2020.

The decision to maintain the stability of the Egyptian pound has come at a cost, as it has led to a depletion of foreign exchange in the economy through a reduction in commercial banks’ net foreign assets. In August, these assets shrank by over 5%, reaching $13.1 billion, as calculated by HC Research based in Cairo.

Nevertheless, Kristalina Georgieva mentioned that progress is being made in the IMF’s assessment under Egypt’s $3 billion rescue program.

“In the last couple of days there have been some constructive engagements,” the IMF head said ahead of a speech she made in Abidjan, Ivory Coast.

“There will be more systematic work of our team with Egypt. So stay tuned. Let’s see what would come out in the next weeks.”

Egypt’s long-term foreign debt rating was downgraded late Thursday by Moody’s to Caa1 from B3, seven levels into junk.

The ratings agency cited the government’s “worsening debt affordability trend and the persistence of foreign currency shortages in the face of increasing external debt service payments over the next two years.”

The economic situation in Tunisia, another North African country facing challenges, is not as severe as some others, but it still requires immediate attention to finalize the agreements related to a $1.9 billion rescue package from the IMF, according to Georgieva.

A debt restructuring is not required as “they are not yet hanging at the cliff,” she said.

Nevertheless “the sooner the country takes some measures to strengthen their fiscal position, to strengthen their overall economic performance the better.”

Egypt and Tunisia are grappling with some of the highest bond yields globally, highlighting investor caution towards holding their debt. Egypt’s dollar notes yield an average of 18.5%, as per Bloomberg indexes, while a Tunisian bond maturing in 2025 is trading at a yield of over 40%.

Moving to the southern part of the continent, Zambia and Ghana, both countries that have experienced debt defaults, are in line to receive additional support, as stated by Georgieva.

She noted that a memorandum of understanding with Zambia’s bilateral creditors has been tentatively agreed upon and will be signed once a few remaining details are resolved.

Additionally, in recognition of the challenges faced by many of the world’s poorest nations in repaying debt, Georgieva expressed her support for the concept of suspending debt payments when countries are hit by climate-related disasters.

“I’m very much in favour of including clauses in debt, be it bonds or loans, that put debt service suspension in place. So if a natural disaster happens, the country is not forced to choose between saving lives and paying creditors,” she said.

“We all need to think about how we go about debt service in a world of more frequent and devastating climate disasters.”

Managing Director of the International Monetary Fund (IMF), Kristalina Georgieva, has assured Ghanaians that the Fund will be working expeditiously to approve the country’s request to obtain a credit facility worth $3 billion.

Engaging stakeholders during the Spring Meetings of the World Bank Group (WBG) on Thursday, Madam Georgieva she expressed optimism about creditors giving Ghana the go ahead to finalise its deal with the Fund.

“To tell you the truth, I am actually quite optimistic. Ghana is going to move; the creditors are going to move; and we (the IMF) are going to move swiftly… so stay tuned and stay positive,” she said.

Her assurance comes amid ongoing discussions between Ghana and its creditors over its debt situation. Ghana’s debt-to-GDP ratio has increased to over 90%, leading to concerns about its ability to repay its loans.

However, Madam Georgieva said the IMF is committed to supporting Ghana’s economic recovery and will work closely with the government and other stakeholders to address the country’s debt challenges.

“We know that Ghana has a strong track record of economic growth and has made significant progress in reducing poverty in recent years,” Georgieva said. “We believe that with the right policies and support, Ghana can overcome its current challenges and continue on a path of sustainable development.”

She also praised the Ghanaian government’s efforts to implement economic reforms, saying that they have taken “difficult but necessary steps” to address the country’s fiscal imbalances.

Madam Georgieva added that, the IMF is committed to providing technical assistance and policy advice to help Ghana implement its economic reform programme.

According to Richard Ahiagbah, the director of communications for the ruling New Patriotic Party (NPP), the effects of Covid-19 and the Russia-Ukraine war on the world economy are visible.

He told Ghanaians not to be deceived by the main opposition National Democratic Congress(NDC) to think otherwise.

Despite the effect of these two exogenous factors, he said, the government of Ghana continues to pay salaries and provide essential public services.

“Ghanaians, we are going through difficulties, but we continue to pay salaries and provide essential public services.

“The impact of Covid-19 and Russia-Ukraine war on the global economy is real. Let’s not be deceived by NDC to think otherwise,” he tweeted.

Ghanaians, we are going through difficulties, but we continue to pay salaries and provide essential public services. The impact of Covid-19 and Russia-Ukraine war on the global economy is real. Let's not be deceived by NDC to think otherwise. #CitiCBS #CitiNewsroom #JoyNews… pic.twitter.com/1krde4mSex

— Richard Ahiagbah (@RAahiagbah) April 13, 2023

The Managing Director of the International Monetary Fund (IMF) Kristalina Georgieva has also repeated her comment that Ghana’s economy has been negatively impacted by the Russia-Ukraine war.

She described Ghana as an innocent bystander that has been hit by the Covid pandemic and the war.

Speaking at the ongoing IMF/World Bank Spring Meetings in Washington, she said “we have been in constant contact with authorities in Ghana, we have worked very hard and very swiftly to have the programme, $3bn support programme, for Ghana in place.

“We have been urging Ghana’s creditors to act swiftly. My appreciation also for the proactive role of the Minister of Finance of Ghana in reaching out to the creditors. We are expecting that next week there will be discussions among creditors.”

She further indicated that the Fund has asked Ghana’s creditors to act swiftly to ensure that the deal that the country is seeking with the Fund is approved.

“I can tell you that I use every opportunity myself to urge them to act swiftly. Let us remember that Ghana for a long time has done really well to tap markets to finance its growth paths.

“It has been like all innocent bystanders hit by Covid, hit by the war in Ukraine. it caused complicated domestically, the ability to Finance the budget. So a country that has a long track record of sound macroeconomic management.”

Kristalina Georgieva, the IMF’s managing director, is confident that the fund’s Executive Board would quickly give Ghana’s bailout request its final clearance.

Ms Georgieva said at the ongoing World Bank/IMF Spring Meetings in Washington D.C. that her optimism stemmed from the swelling goodwill that the country was getting from the international community, including its creditors.

Graphic Online’s Maxwell Akalaare Adombila who is covering the World Bank/IMF Spring Meetings in Washington D.C., USA reports Ms Georgieva told journalists Thursday that her outfit was pushing the bilateral creditors to quickly provide the financial assurance needed for the board to approve the deal.

Ghana secured a staff-level agreement (SLA) for the $3 billion request in December but efforts to move pass the final lap have dragged as bilateral creditors haggle over the terms of the debt restructuring exercise.

Sources had told Graphic Online at the Spring Meetings that a deal in May was closer as China softened its stance on the need for multilaterals to share debt losses.

The IMF MD, when asked about when Ghanaians should expect a deal, said: “We have been urging Ghana’s creditors to act swiftly.”

“To tell you the truth, I am optimistic that we are going to move swiftly and so stay positive,” she said.

Ghana needs a deal to stabilise the cedi further, contain inflationary pressures and tap into the international capital market for loans to fund development. It would be the country’s 17th bailout programme after joining the IMF in September 1957.

The National Democratic Congress’ (NDC’s) national communications officer, Sammy Gyamfi, claims thatCOVID-19 is not the cause for Ghana’s economy woes.

The Akufo-Addo administration has attributed Ghana’s economic crisis to the COVID-19 pandemic and the war in Russia and Ukraine.

The Managing Director of the International Monetary Fund (IMF), Kristalina Georgieva had earlier agreed that COVID-19 and the Russia-Ukraine war negatively affected the country’s economy.

But speaking on Face to Face on Citi TV with Umaru Sanda Amadu, Sammy Gyamfi, said the IMF Chief was being diplomatic with the truth on the true state of the Ghanaian economy.

According to him, the MD of IMF didn’t want to jeopardise the progress of the bailout the government is seeking to restructure its debt, hence the massaged facts regarding the economic crisis.

The NDC’s National Communications Officer reiterated that the economy was broken before the outbreak of COVID-19.

“The economy was worse before COVID-19 came in, even before COVID-19 our economy was broken. It’s not what the IMF or World Bank says, it’s about what the facts say. The IMF is like a doctor, doctors have a certain duty of care to their clients. They will tell you reasons for your sickness but in a diplomatic way and well-dressed manner”.

He maintained, “right now that we have gone to IMF for a bailout, they are our doctor, and we are the patient. They will definitely not say something that actually reflects the reality, knowing that it can hamper the bailout and economic recovery programme we are seeking from them. They were being diplomatic. In diplomatic settings, it’s very normal. If you listen to what these external players are saying, you will be deceived. You need to examine things for yourself, before COVID-19 what was the state of the economy?”.

Mr. Gyamfi asserted that the COVID-19 pandemic cannot be used as a justification by the government for the woes of the country slamming the government for spending money on wasteful ventures.

“They [NPP government] had more resources to transform this country than any government since Dr. Kwame Nkrumah’s tenure. Yet have wasted these funds on needless and useless ventures such that today they have very little to show for the unprecedented resources they had. These and many falsehoods were presented by President Akufo-Addo in his state of the nation address,” the National Communications Officer of NDC pointed out.

According to him, the local currency had depreciated by close to 13% against the dollar before COVID-19 describing as false claims that the economy was on a good trajectory before the pandemic.

“Before COVID-19, our cedi had depreciated against the dollar by close to 13%. That claim that we were on a good trajectory before COVID-19 is false,” he stated.

The Managing Director of the International Monetary Fund, Kristalina Georgieva, will visit Rwanda later this month after traveling to Zambia, Reuters has revealed.

Madam Georgieva on Thursday said she would visit Zambia the week after next, but her visit to Rwanda has not been previously reported. She will travel to Africa after speaking at the World Economic Forum in Davos, Switzerland next week.

Rwanda was the first African country to receive IMF funding under its new Resilience and Sustainability Trust.

The IMF in October reached a staff-level agreement with Rwanda on a 36-month financing package valued at $310 million.

At the time, the IMF said the funding would help the country move forward with its economic reforms and build resilience against climate change.

Due to a limited market supply, Brent crude increased by 2.5% to $79.75 a barrel and West Texas Intermediate by 2.6% to $74.70 early on Thursday.

US pipeline operator Colonial Pipeline said Wednesday it has halted operations at its Line 3, with a restart scheduled for Jan. 7, Reuters reported. Prior to the pipeline shutdown, oil prices had been hit by uncertainty in the near-term economic prospects for China as COVID-19 cases rise.

Significant disruption is expected in the coming months, followed by a recovery from around the middle of the year, which should boost demand, OANDA analyst Craig Erlam said in a Wednesday note.

The falling value of the US dollar supported higher oil prices by encouraging traders using other currencies. A weaker dollar further fuels strong demand in the market. Meanwhile, global recession fears lead to lower demand expectations.

Weaker demand worries heightened especially after the IMF’s Managing Director Kristalina Georgieva said one-third of the world’s economies are expected to go into recession in 2023.

Low demand fears are also supported by rising COVID cases in China which cap further price increases. Adding more on demand worries, the world’s second-largest economy, China, significantly increased its first batch of 2023 export quotas for refined oil products.

This shows the country is expecting less consumption.

This follows the Fund’s announcement on December 13 that it had reached an agreement with Ghana at the staff level for an extended credit facility worth US$3 billion over three years, among other things, to restore macroeconomic stability.

“Very good meeting with President @NAkufoAddo. I congratulated him on Ghana reaching a staff-level agreement for IMF support. We stand with Ghana and remain committed to helping deliver relief to Ghanaians,” the IMF boss wrote.

Meanwhile, the Staff-Level Agreement secured with the IMF is subject to IMF Management and Executive Board approval and receipt of the necessary financing assurances by Ghana’s partners and creditors.

“The economic program aims to restore macroeconomic stability and debt sustainability while laying the foundation for stronger and more inclusive growth,” the IMF said on its website on December 13.

“The Ghanaian authorities have committed to a wide-ranging economic reform program, which builds on the government’s Post-COVID-19 Program for Economic Growth (PC-PEG) and tackles the deep challenges facing the country,” the statement read in part.

“Key reforms aim to ensure the sustainability of public finances while protecting the vulnerable. The fiscal strategy relies on frontloaded measures to increase domestic resource mobilization and streamline expenditure. In addition, the authorities have committed to strengthening social safety nets, including reinforcing the existing targeted cash-transfer program for vulnerable households and improving the coverage and efficiency of social spending,” it added.

The International Monetary Fund (IMF) has congratulated Ghana on the efforts made so far with regards to the IMF bailout being sought by the country.

Managing Director of the International Monetary Fund (IMF), Kristalina Georgieva, restated the Fund’s commitment to help Ghana secure a support programme.

Ghana, in December 2022, reached a staff-level agreement with the IMF, awaiting a board approval.

In a tweet, Ms. Georgieva said “very good meeting with President @NAkufoAddo. I congratulated him on Ghana reaching a staff-level agreement for IMF support. We stand with Ghana and remain committed to helping deliver relief to Ghanaians”.

President Akufo-Addo is in America attending the U.S-African Leaders’ Summit.

Ghana secures staff agreement

The IMF staff and government of Ghana reached a Staff-Level Agreement on economic policies and reforms to be supported by a new three-year arrangement under the Extended Credit Facility (ECF) of about $3 billion.

A statement from the fund, said the Ghana’s strong reform programme aimed at restoring macroeconomic stability and debt sustainability while protecting the vulnerable, preserving financial stability and laying the foundation for strong and inclusive recovery, was key in this decision.

However, the staff-level agreement is subject to IMF Management and Executive Board approval and receipt of the necessary financing assurances by Ghana’s partners and creditors.

To support the objective of restoring public debt sustainability, the statement added that, the government has launched a comprehensive debt operation. But the Fund said sufficient assurances and progress on this front will be needed before the proposed Fund-supported programme can be presented to the IMF Executive Board for approval.

“The Ghanaian authorities have committed to a wide-ranging economic reform program, which builds on the government’s Post-COVID-19 Programme for Economic Growth (PC-PEG) and tackles the deep challenges facing the country”, the statement pointed out.

Other international organizations, such as rating agencies, raised concern about Africa’s ability to pay back its loans.

According to the IMF, 20 of the continent’s 54 nations were close to or in a state of distress as of 2019.

Record commodity prices and low global interest rates have encouraged African countries to borrow as they did in the 1990s, but now some are struggling to pay up as their revenue slows along with economic growth.

Government debt as a percentage of gross domestic product in sub-Saharan Africa has doubled in the past decade, heading back toward the level it reached in 2000.

International Monetary Fund Managing Director Kristalina Georgieva said in November this is a cause for concern. Of the 54 countries on the continent, 20 are near or at distressed levels, according to the IMF, which means they face difficulties honoring their obligations.

African governments have raised about $26 billion in international markets this year, from close to $30 billion in 2018, as they took advantage of investors’ thirst for returns in a world awash with negative yields.

Volatile currencies across the continent increase the risks of borrowing in hard currency and the rising cost of serving debt could crowd out other expenditure in a region that’s home to more than half of the world’s poor people.

“The conditions are ripe for a much higher level of debt distress,” Sonja Gibbs, head of sustainable finance at the Institute of International Finance, said by phone. “Whatever triggers the next crisis, when it happens, you are likely to see a high degree of contagion risk because investors have been moving into higher yielding assets.”

“Some individual countries are getting to higher levels in terms of debt-to-GDP ratios, that’s the concern,” African Development Bank President Akinwumi Adesina said in an interview. The debt-to-GDP ratio of Africa is still “well within acceptable limits,” he said.

Costly Debt

More reliance on commercial bonds has raised servicing costs, diverting funds that could be spent on new roads or schools. Nigeria, the continent’s top oil producer, spends about the same amount every year on repaying debt as it does on infrastructure.

Countries such as South Africa, the continent’s most industrialized economy, are raising debt levels and this year had its biggest Eurobond issuance yet to help plug a widening budget deficit as economic growth slows and public-sector wages and bailouts for state companies sap resources.

External debt payments now eat up on average about 13% of the revenue of African governments from 4.7% in 2010, according to data compiled by the U.K.-based Jubilee Debt Campaign.

Overspending and crashing commodity prices in the 1990s led to a debt crisis that prompted multilateral lenders and rich nations to write off the obligations of dozens of African countries in 2005. This time around a debt pardon may not be that easy.

The complex debt structure with opaque terms and mix of different creditors will make any potential restructuring agreement more difficult.

“We’re concerned that debt relief might now become more complicated,” said Jan Friederich, a senior director at Fitch Ratings. “Nowadays there is a greater concern that governments, when they forgive any debts, might not actually help the African countries very much, but might primarily be bailing out the commercial creditors.”

Russia’s air strikes on civilian infrastructure raise the cost of Ukraine’s recovery, which will require nearly $4 billion per month to maintain power and water supplies, according to the International Monetary Fund’s chief.

In an interview with Reuters, IMF managing director Kristalina Georgieva said the organisation was focused on keeping Ukraine afloat while working on a longer-term plan.

“We still hope that we can stay within these parameters of 3-4 billion, but what changed since we had this discussion in Russia’s terrible bombing of civilian infrastructure,” she said.

“Just to get electricity back and water supply back we are moving towards the upper range of 4 billion…Just imagine a worst-case scenario.”

Georgieva also signalled that China should be allowed to join an international platform that the European Commission wants to set up this year for Ukraine.

At the beginning of their annual meetings on Monday in Washington, the International Monetary Fund (IMF) and the World Bank issued a warning about a potential global recession.

According to World Bank President David Malpass, economic growth in Europe’s industrialized nations is decreasing.

He said currency depreciation was a concern for low-income countries, where the debt burden was expanding, in reference to the dollar’s recent climb.

According to Malpass, the increase in interest rates added to the strain on these nations, and inflation continued to be a serious issue for everyone, but especially the poor.

IMF Managing Director Kristalina Georgieva noted slowing economies in all three of the world’s major economic zones. She pointed to increased energy prices as a problem for the eurozone and to outbreaks of the coronavirus pandemic in China as a persistent cause of supply chain problems.

While the labour market in the United States remained strong, jobs growth was slowing in response to interest rate increases imposed by the Federal Reserve.

On Tuesday, the IMF is to present its latest forecasts for the global economy. Georgieva has announced that the growth prediction will be reduced again.

She pointed to factors such as the pandemic, the Russian invasion of Ukraine and climatic disasters on all continents as creating problematic situations.

For the first time since 2019, the meeting is taking place in a single location, with gatherings over recent years being in hybrid format.

The meeting brings together finance ministers and representatives of banking and development aid, as well as central bankers.

In order to ensure that major elements of the programme are included in the 2023 budget statement, finance minister Ken Ofori-Atta said the government will expedite negotiations with the International Monetary Fund (IMF).

The Finance Minister at a press briefing on Wednesday said negotiations have been smooth so far.

“In line with the President’s dialogue with the IMF Managing Director, Kristalina Georgieva, negotiations will be fast-tracked to ensure that key aspects of the programme are reflected in the 2023 Annual Budget Statement in November 2022,” he added.

He said the government is committed to ensuring that a comprehensive package is negotiated with the International Monetary Fund with the aim of restoring and sustaining macroeconomic stability, ensuring durable and inclusive growth, and promoting social protection.”

“In addition, the IMF and Government Team are working to update the medium-term macro-fiscal framework to inform IMF programme design.”

The Finance Minister said no agreement has been reached with the fund on the parameters of debt operations, as the government is still in the process of completing the debt sustainability analysis.

Mr. Ofori-Atta stressed that everything will be done, to protect the financial sector; and there must be room for a win-win conversation through extensive stakeholder engagement with both the domestic and external investors.

He also indicated that the Development Bank Ghana (DBG), is supporting the private sector to invest in areas that will stabilize the economy over the medium to long-term, with positive knock-on effects on job creation and economic growth.

“I am extremely confident about where we will land on this journey. We have survived a 142 percent inflation, yellow-corn hysteria, mass exodus from our country, and more recently a successful exit from the 2015 Extended Credit Facility. So let us go for the spirit of courage for the LORD is with this Nation. Let us not fear, for He who is with us is greater than all.”

Georgieva said the following when speaking at the Africa Adaptation Summit in the Netherlands earlier this month:

“Ghana’s people have been harmed by exogenous (external) shocks, just like everyone else on the earth.

“The epidemic came first, then Russia’s conflict in Ukraine.

We must recognize that this is not the result of poor national policy, but rather of a confluence of shocks, and help Ghana as a result.

stated Georgieva.

Discussing Ghana’s ongoing talks with the IMF, Georgieva highlighted that the Fund had ‘started very constructive discussions’, noting that she would support Ghana “because your (Ghana’s) strength contributes to the strength of your neighbours; it contributes to a stronger world”.

In the face of the pandemic and the war in Ukraine, as stressed by Georgieva, Ghana proactively entered talks with the IMF for a $3 billion loan.

The loan will be used to stabilise the economy in the face of global economic turbulence, supporting the cedi and helping to reduce the price of food and fuel.

In the past month, the IMF has provided loans to both Pakistan and Sri Lanka, showing the global nature of current economic challenges.

Meanwhile, the immediate past IMF resident representative for Ghana, Dr. Albert Touna Mama, said Ghana has dealt well with those external shocks and expressed confidence that it can deal with these ones too.

“This country has known a lot of shocks and we have navigated those together. There is no reason it cannot navigate the current ones,” Dr. Mama said.

More than 30% of emerging and developing countries are at or near debt distress, Managing Director of the International Monetary Fund, Kristalina Georgieva, has revealed.

For low-income countries that number is 60%.

According to her, the tightening financial conditions and exchange rate depreciations has escalated the debt service burden which she described a harsh and for some countries unbearable burden.

Speaking at the hybrid meeting of the G20 Finance Ministers and Central Bank Governors, Madam Georgieva said the outlook of the global economy has darkened significantly, and uncertainty is exceptionally high, adding, “downside risks about which the IMF had previously warned have now materialisedâ€.

She therefore wants a strong global leadership to tackle the scourge of high debt, which has reached multiyear highs.

“The war in Ukraine has intensified, exerting added pressures on commodity and food prices. Global financial conditions are tightening more than previously anticipated. And continuing pandemic-related disruptions and renewed bottlenecks in global supply chains are weighing on economic activity.â€

“As a result, later this month, we will project a further downgrade to global growth for both 2022 and 2023 in our World Economic Outlook Update. Moreover, downside risks will remain and could deepen—especially if inflation is more persistent—requiring even stronger policy interventions which could potentially impact growth and exacerbate spillovers particularly to emerging and developing countries. Countries with high debt levels and limited policy space will face additional strains. Look no further than Sri Lanka as a warning signâ€, she added.

Emerging and developing countries have also been experiencing sustained capital outflows for four months in a row. They now suffer the risk of reversing three decades of catching up with advanced economies and instead falling further behind.

3 priorities to navigate challenging environment

The MD of IMFsaid first countries must do everything in their power to bring inflation down, adding, “failure to do so could risk the recovery and further damage living standards for vulnerable peopleâ€.

She expressed excitement that central banks are stepping up their game.

“Monetary policy is increasingly synchronised: more than three-quarters of central banks have raised interest rates and have done so 3.8 times. Central bank independence is critical for the success of these policy actions, as is clear communication and a data-driven approach.â€

Secondly, she said fiscal policy must help but not hinder central bank efforts to tame inflation.

“With growth slowing down, some people will need more support, not less. So fiscal policy needs to reduce debt while providing targeted measures to support vulnerable households facing renewed shocks, especially from high energy or food pricesâ€.

Thirdly, Kristalina Georgieva said, a fresh impetus for global cooperation will be critical to confront the multiple crises the world is facing. We need G20 leadership particularly to address the risks from food insecurity and high debt.

President @NAkufoAddo. I congratulated him on

President @NAkufoAddo. I congratulated him on