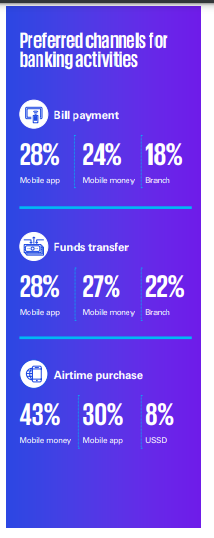

The Bank of Ghana’s (BoG) 2023 FinTech Sector Report indicates substantial advancements in the nation’s digital financial sector, with mobile money accounts exceeding 65 million and total transaction values surpassing GH¢1.9 trillion.

This development represents a significant achievement in Ghana’s pursuit of a more inclusive and cashless economy.

The surge in this sector is fueled by the growing acceptance of mobile financial services, which offer a dependable and efficient way for millions of Ghanaians, particularly in underserved and rural regions, to obtain financial services.

According to the report, mobile money has established itself as a prominent player in Ghana’s financial framework, with transaction volumes growing exponentially each year.

The Bank of Ghana emphasizes the vital contribution of Rural and Community Banks (RCBs) to the national financial inclusion strategy.

The central bank has pointed out that RCBs, which act as crucial financial service providers for rural communities, have a unique chance to utilize technology and digitalization in their operations.

By implementing digital solutions, RCBs could effectively narrow the financial access divide in rural areas, delivering more customized services tailored to the needs of local populations.

At the 23rd Annual Chief Executive Officers’ Conference held in Ho, Mrs. Elsie Addo Awadzi, the BoG’s Second Deputy Governor, stressed the significance of digital transformation for the rural banking sector through remarks made by Mr. Yaw Sapong, Director of the Other Financial Institutions Supervision Department.

She emphasized that RCBs should capitalize on technology to broaden their reach and enhance the quality of their service offerings.

Mrs. Awadzi highlighted the BoG’s dedication to promoting financial inclusion through digital initiatives, referencing the success of the Ghanapay initiative, which serves as a national digital payments platform aimed at improving financial service access, particularly in rural regions.

She encouraged RCBs to adopt this platform and build collaborations with FinTech companies via the ARB Apex Bank to foster innovation and tailor their offerings to customer needs.

Furthermore, she emphasized the necessity for RCBs to move beyond standard financial products, asserting that to effectively assist rural communities, they must create specialized financial solutions that address the specific requirements of local populations.

This entails comprehending the financial rhythms of farmers, small-scale traders—particularly women and individuals with disabilities—and local enterprises.

By providing services such as savings and loan products that align with agricultural and business cycles, RCBs could ensure that their offerings remain relevant and accessible to their intended clients, she stated.

She noted that this strategy would not only bolster the financial well-being of rural communities but also position RCBs as the primary source for financial services in those areas.

To maintain this progress, Mrs. Awadzi urged RCBs to invest in capacity building and effective corporate governance practices, suggesting that enhancing staff skills would enable RCBs to adapt to changing financial needs, while robust governance structures would promote accountability and long-term stability.

Mr. Alex Kwesi Awuah, Managing Director of ARB Apex Bank, also praised the successful rollout of the Financial Sector Development Project (FSDP).

With support from the Government of Ghana and the World Bank, the FSDP has played a crucial role in implementing digital banking platforms for RCBs, facilitating seamless and secure digital financial services for their clients.

Mr. Awuah pointed out that the digital transformation of RCBs has not only enhanced their operational effectiveness but also allowed them to broaden their customer base, integrating more Ghanaians into the formal financial system.

The 23rd Annual CEOs Conference convened 147 CEOs from RCBs nationwide, offering a forum for rural banking leaders to explore challenges, opportunities, and the future of the sector.

Held on the theme: “Positioning Rural Banking at the Centre of the National Financial Inclusion Agenda,” the event also featured representatives from the Bank of Ghana, executives from the Association of Rural Banks, and the Board Chairman of ARB Apex Bank, Dr Toni Aubyn.

As the rural banking sector continues to play a pivotal role in Ghana’s financial landscape, the adoption of technology and a customer-centric approach will be essential in ensuring sustainable growth and widespread financial inclusion across the country.