The Social Security and National Insurance Trust (SSNIT) has announced that it has made a payment of about five billion Ghana Cedis (GH¢5 billion) in pensions this year.

SSNIT, Ghana’s statutory public trust responsible for administering the country’s basic national pension scheme, mostly make payments on the 20th of every month.

The payment was confirmed by the Director-General of the Social Security and National Insurance Trust (SSNIT), Kwesi Afreh Biney, during an appearance on Citi TV’s Breakfast show on Thursday, October 30.

He made these remarks in response to affirming the viability, capacity and commitment of the scheme to meet its obligations.

“What I will say is that we have successfully paid pensions since 1965. In 1965, only three pensioners were being paid. Today, we pay over 257,000 pensioners each month. This year alone, we paid in excess of five billion cedis in pensions. Is it sustainable? The trust will continue to evolve, we will continue to make it stronger, and we’ll put in systems to ensure that we never fail,” he noted.

Around October last year, multiple investigations and Right to Information (RTI) disclosures revealed that SSNIT had tied up over GH¢1.8 billion in underperforming or mismanaged real estate projects, which included commercial properties valued at GH¢1 billion, residential projects exceeding GH¢500 million, and land banks with questionable strategic value, sparking fears that poor returns could threaten the fund’s long-term sustainability. These fears, according to reports, still linger in the minds of some Ghanaians.

But the SSNIT Director General has assured the public that the scheme remains strong, highlighting that pensioners’ pensions will not be in jeopardy.

Mr Biney acknowledged the shortfalls in the scheme and the challenges he inherited from the previous administration; however, he revealed that his outfit has worked on a three-year strategy to address these issues.

“The institution remains strong. There were challenges, but there were opportunities in there. I inherited challenges and positives, but we worked together to define a strategy for what the future will look like. This is a defined benefit scheme, so it’s one that we have to pay. It’s what the government even has to guarantee as well. So there’s nothing like the trust will fail, for which reason people’s pensions will be in jeopardy, non” he added.

During the Trust’s 60th anniversary in July, Dr Afreh Biney highlighted that the time it takes to process a pension has significantly dropped from several weeks to under ten working days.

He also touted the accessibility of SSNIT’s digital services, looking forward to rolling out its fully-fledged digital branch by September 2025.

He asserted that institutions survive not because they are flawless, but because they reflect, reform, renew, and take feedback constructively.

“The road ahead,” he said, “is challenging but also full of promise.” He added, “We must expand coverage, especially for the informal sector, because every worker deserves to retire in dignity. We must innovate with technology, deepen transparency, and strengthen public confidence, and we must do it with government, employers, labour, and civil society.”

“SSNIT must not just be a system people contribute to; it must be a partner they believe in,” he continued. “So yes, if you are over 60 and still dancing at parties, remember social security is 60 and still standing, still serving, and still strong. If the walls of SSNIT could speak, they would whisper stories of service, of quiet sacrifice, of hard lessons, and of a deep, unwavering belief in simple promises.”

Meanwhile, SSNIT paid a total of GHS521.96 million to over 257,000 pensioners in July. In a Facebook post, the Trust noted that the disbursement forms part of its commitment to ensuring the timely payment of pensions to retirees under the national scheme. Pensioners are expected to receive their next payment on August 21.

Earlier this year, SSNIT announced a 12% adjustment in pensions for 2025, starting in January, with payments scheduled for the third Thursday of every month.

This revision was made in coordination with the National Pensions Regulatory Authority (NPRA) and complies with Section 80 of the National Pensions Act, 2008 (Act 766).

As per SSNIT, all retirees receiving benefits as of December 31, 2024, will see an average increase of 12% in their monthly payments.

The adjustment includes a fixed increment of 8% along with an additional GH¢72.58, which accounts for 4% redistributed to assist lower-income pensioners.

“Redistribution is a mechanism applied to the indexation rate to cushion low-earning pensioners in conformity with the solidarity principle of social security.

As a result, pensioners will have an effective increment between 32.19% at the bottom end and 8.04% at the top end. Redistribution ensures that the minimum monthly pension of GH¢300 in 2024 will increase to GH¢396.58 in 2025, an effective increase of 32.19%,” a statement from SSNIT said.

This redistribution policy aims to provide extra relief for pensioners with lower earnings, following the social security solidarity principle.

Consequently, those receiving the least will experience a 32.19% boost, while those at the highest level will see an 8.04% rise.

With this revision, the minimum monthly pension will increase from GH¢300 in 2024 to GH¢396.58 in 2025. For retirees under PNDC Law 247, the highest monthly benefit will now stand at GH¢201,792.37, marking an 8.04% growth.

Meanwhile, the average pension will move from GH¢1,776.81 in 2024 to GH¢1,990.03 in 2025. SSNIT further disclosed that 63% of pensioners, particularly those earning GH¢1,814.50 or less per month, will benefit from increases ranging from 12% to 32.19%, ensuring their income keeps pace with inflation.

In a related development, the Finance Minister, Dr Cassiel Ato Forson, on Tuesday, June 3, oversaw the inauguration of the Board of Trustees for SSNIT, where he called for prudence, integrity, and transparency in the management of Ghana’s pension funds.

Dr Forson, in his address, noted the vital national importance of SSNIT, reminding the board that it is an institution “we will all need one day, when we retire.”

He warned against any attempts to sell state assets to politically connected individuals, as he questioned some of SSNIT’s past investment decisions

“Please don’t sell state assets to politicians. The President will not accept it, and as your sector Minister, I will be the first to oppose it,” he stressed.

He highlighted that the people of Ghana have entrusted their future into the board’s hands, and therefore, their actions must reflect the weight of that responsibility, charging the new board to chart a new course that will reflect the responsibility the people of Ghana have entrusted to them.

Chairman of the newly constituted Board, Nana Ansah Sasraku III, is committed to providing strategic direction to the Trust by leveraging collective expertise to drive growth, sustainability, and excellence in service delivery.

Nana Ansah Sasraku III noted that a roadmap for the Trust will be provided to safeguard the Scheme’s sustainability and ensure that it continues to meet its obligations to its valued members. He acknowledged the magnitude of the task ahead and expressed the Board’s readiness to deliver.

The Government of Ghana successfully saved a total of GHC895 million in 2023 through a nationwide payroll monitoring exercise and the deactivation of nearly 19,000 ghost pensioners from the Social Security and National Insurance Trust (SSNIT) payroll.

This achievement was announced by the Minister of Employment and Labour Relations, Mr. Ignatius Baffour Awuah, during a news briefing in Accra.

The savings included GHC345 million recovered from a comprehensive payroll monitoring exercise conducted by the Fair Wages and Salaries Commission (FWSC) across 120 public sector institutions. Additionally, GHC550 million was saved through the SSNIT’s deactivation of non-existent pensioners.

Mr. Baffour Awuah emphasized that these efforts reflect the government’s dedication to improving the management of public funds, particularly in the area of pensions. He highlighted the importance of these savings in strengthening the financial health of the government and supporting ongoing development initiatives.

“The government remains unwavering in its commitment to improving the welfare of workers while maintaining a peaceful labor front,” the Minister stated, commending various stakeholders, including Parliament, the Ministries of Finance, National Security, Education, and Health, the Ghana Employers’ Association, Organised Labour, and development partners for their collaboration in resolving labor-related issues.

The Minister also announced the development of the Ghana Labour Market Information System (GLMIS), an online platform designed to improve the services of the Labour Department. The GLMIS will provide valuable data on job vacancies, skills in demand, and training opportunities, helping to reduce job mismatch, unemployment, and underemployment. The system is part of the third component of the Ghana Jobs and Skills Project, funded by the World Bank, aimed at enhancing skills development and job creation.

“The GLMIS will enable employers to declare job vacancies and allow job seekers to upload their CVs for job matching, facilitating a more efficient labor market,” Mr. Baffour Awuah explained. He expressed optimism that this platform would support the government’s efforts to address challenges in the labor market and improve policy interventions for sustainable economic development.

The Social Security and National Insurance Trust (SSNIT) has distributed a substantial GH¢447.07 million to 250,580 pensioners for August 2024.

This payment, issued on Thursday, August 15, 2024, covers pension benefits under both PNDC Law 247 and Act 766, demonstrating SSNIT’s continued commitment to securing the financial stability of retirees across Ghana.

SSNIT reported that the highest monthly pension under PNDC Law 247 reached GH¢186,777.58, while the maximum under Act 766 was GH¢26,509.66.

The smallest monthly pension for current pensioners was GH¢409.10, while the minimum for new pensioners was established at GH¢300.00.

The next pension distribution is scheduled for September 19, 2024.

Imagine dedicating 30 years to your career, only to retire with a meager pension.

This is the reality for numerous retirees who have invested their hard work and effort into the nation’s progress.

Such is the case for a cousin of Balbir Naa Densua Allan, who herself is a retiree.

Describing the challenges faced by retirees, she mentioned that she considers herself somewhat fortunate because her husband, a foreign national, receives approximately £150 in weekly pension, which is their main source of income. This amount is about 10% less than what he would receive if he were residing in the UK.

In contrast, her cousin, who worked in Ghana, receives only GH₵300. While this used to meet her needs, the recent depreciation of the cedi and rising medical costs have left her reliant on support from her family and children.

She recounted how her cousin’s situation would have been even more dire without her help, noting, “Life will be very, very awful because look at the cost of electricity, look at the cost of the utilities , gas, water, the cost of a ball of kenkey and you want a person, she worked with Ghana Broadcasting Cooperation, and you want this person to survive on GH₵300 a month.

“When somebody like my husband has brought his pension in Ghana and he is earning like GH₵12,000 a month, he is at the base because he did the basic job and he is on GH₵12,000 a month and he can save some of his money,” she said.

She recounted that upon moving to Ghana, she sold her family property and invested the proceeds in microfinance and government bonds to provide for her family.

Unfortunately, due to the banking sector crisis, much of this money has been lost.

Balbir Naa Densua Allan mentioned that she now struggles to support her family members in need as she once did.

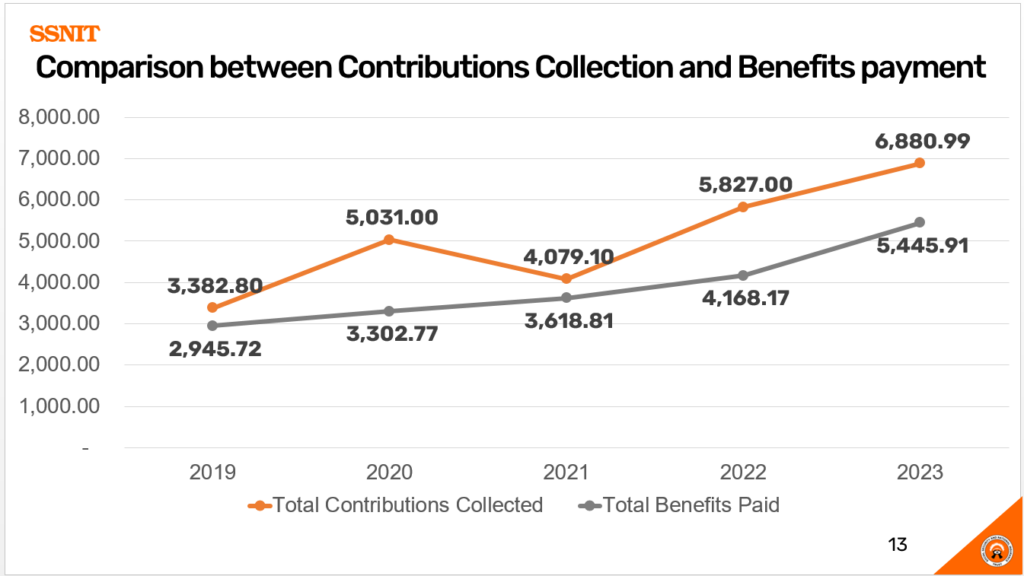

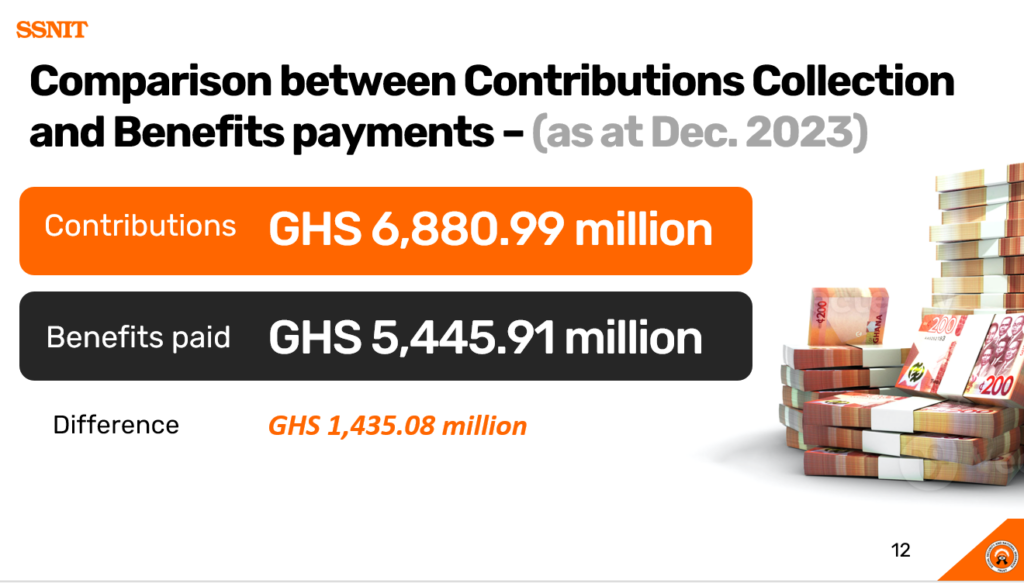

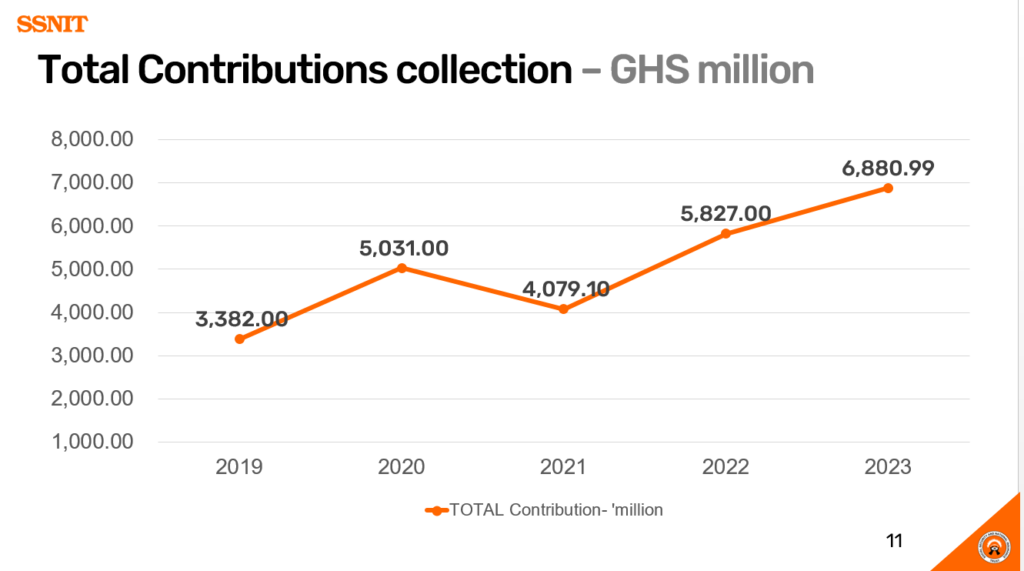

SSNIT Pension Scheme has accumulated a total of ₵6.8 billion in contributions, as reported in SSNIT’s operational summary for the year 2023.

Contribution collections for 2023, showed about a billion cedis jump from the ₵5.8 billion collected in 2022. In 2021, contributions stood at ₵4 billion while in 2020 SSNIT mobilized ₵5 billion.

The 2023 operations report showed that, private sector contributions stood at ₵4 billion as against a target of ₵3.5 billion. This represents 113.9 percent of its performance.

By December 2023, contributions from the public sector totaled ₵2.8 billion, falling short of the ₵4.8 billion target, achieving 66 percent of the expected contributions.

During the same period, SSNIT disbursed ₵5.4 billion in benefit payments, resulting in a surplus of ₵1.4 billion.

In 2022, total benefit payments amounted to ₵4.1 billion, while in 2021, it was ₵3.6 billion.

State of Membership

The figures indicated that active membership reached 1.9 million, demonstrating notable growth compared to previous years.

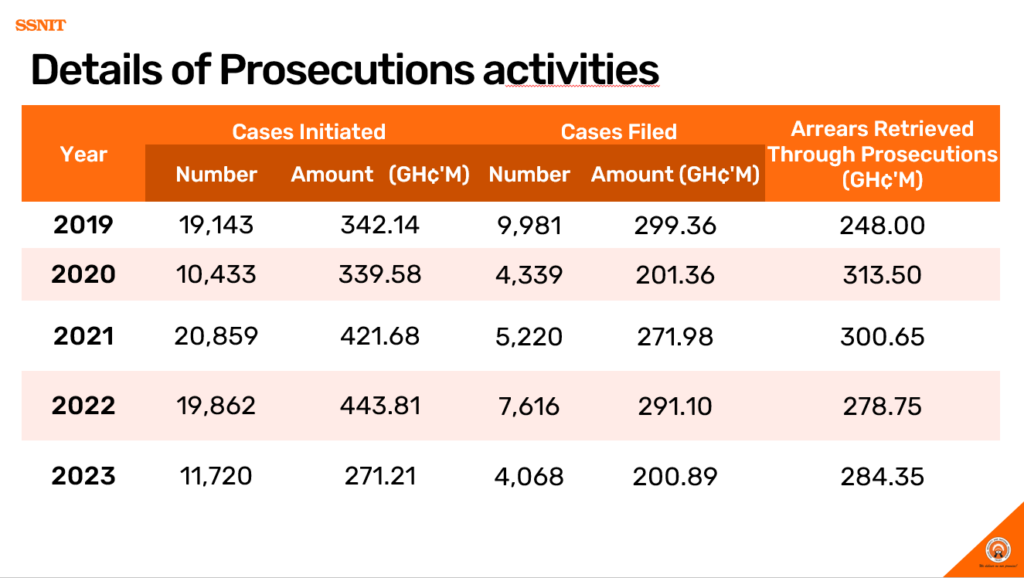

According Managers of the scheme, the company was able to retrieve ₵284 million in of arrears.

Sustaining the Performance

The company’s management has committed to adopting strategies aimed at enhancing the scheme’s growth. These initiatives include:

Promoting and educating stakeholders, including self-employed individuals, on the use of the Trust’s digital platforms for making contributions.

Partnering with the Office of the Director General to engage prominent employers or quasi-governmental organizations with outstanding debts to recover funds.

Increasing efforts to enroll new SEED members and ensuring timely payment processing.

The National Pensions Regulatory Authority (NPRA) has introduced a revised fee structure for service providers within the pension industry, encompassing licensed trustees, pension fund managers, and pension fund custodians.

These adjustments aim to secure sufficient funding for the regulation and supervision of pension funds across the nation.

As per a public notice published on the NPRA’s website, service providers managing funds for individual trustees will now be subject to a GHC500 renewal and registration fee, up from the previous GHC250 charged last year.

Conversely, the renewal fees for licenses and registration for corporate trustees, pension fund custodians, and pension fund managers have remained consistent with last year’s rates, ranging from GHC3,000 to GHC5,000.

Similarly, application, licensing, and registration fees for service providers have been upheld, with costs ranging from GHC2,220 to GHC5,550.

Moreover, registration fees for pension schemes, including master trust, employer, personal, or group personal schemes, have not seen any alterations and continue to range between GHC5,550 to GHC11,100.

The NPRA emphasizes that this updated fee structure is imperative for sustaining the pension industry and upholding effective regulation and supervision of pension funds in Ghana.

Service providers are urged to adhere to these new charges to evade potential penalties or sanctions from the regulatory body.

The Social Security and National Insurance Trust (SSNIT) has refuted claims suggesting that the Scheme might encounter difficulties in meeting its financial obligations to beneficiaries in the future, as outlined in the 2020 International Labour Organization Actuary Report.

Recognizing the speculative nature of the report’s findings, the Scheme emphatically stated that these projections do not correspond with the current realities on the ground.

Speaking to reporters in Accra on Monday, Joseph Poku, Chief Actuary of SSNIT, assured contributors that the scheme remains strong and adequately positioned to meet their needs.

“You cannot lift everything in there and say SSNIT is collapsing in the next 12 years; it is far from the truth. These are the processes…You take a period of 75 years and then, based on reasonable assumptions, you make projections. But remember, if you alter the assumptions, the results will differ. So, don’t take the report at face value; consider it alongside the underlying assumptions,” he further stated.

Mr. Poku further clarified that despite occasional delays in government contributions, the government has fulfilled its commitments up to January 2024. Ongoing engagements are in place to ensure sustained support.

“Monthly contributions have been paid up to January 2024,” he said, adding “While we recognize that March payments should have been made by now, it’s important to note that the government has fully covered January’s contributions, and part of February’s as well. Any delays are minimal, considering the overall timeline,” he said.

The Controller and Accountant General’s Department has instructed retired military personnel and military widows who receive government pension under Cap 30 to participate in quarterly validation exercises at a Veterans Administration, Ghana (VAG) District of their choice.

This validation is necessary to ensure the continuation of their monthly pension payments.

According to a statement released by VAG on Wednesday, March 27, 2024, all Cap 30 Pension Associations, including VAG, must validate their members quarterly and submit the returns to the Controller and Accountant General for the processing of pension payments.

Failure to comply with this requirement may result in individuals being removed from the payroll.

The statement, signed by Major (Retired) Amadu Anicks Lawson Dinko on behalf of the Executive Director, urged all military veterans and military widows receiving government pensions to promptly register with a VAG District to avoid any disruptions to their pension payments.

SSNIT withholds pension funds of 19,100 over failure to do biometric authentication

Social Security andNational Insurance Trust (SSNIT) has retained GH¢480 million, representing funds for 19,100 pensioners who have not undergone biometric authentication.

The Director-General of SSNIT, Dr. John Ofori-Tenkorang, revealed this information during a press conference in Accra, stating that SSNIT is prepared to reimburse the funds when those individuals comply with the biometric authentication process.

He emphasised that SSNIT’s pension scheme obligates the organisation to continue pension payments until the pensioner’s demise.

Death

He said if a person passed away before the age of 72 for those under PNDC Law 247 and 75 for those under the National Pensions Act, 2008 (Act 766), the trust had to pay some money to his or her survivors.

“But if you live beyond those years, then we don’t have to pay anything to your survivors and every month, our operation is that we pay monies directly into your bank account.

“So what we need to do is make sure that we find a way to ascertain that we are actually paying legitimate pensioners. So we asked our cherished pensioners every year to let us know that they are alive,” he said.

That, the SSNIT boss said, was done by asking them to report to the SSNIT officer to biometrically authenticate them and that it was mindful of the fact that there were people who might not have mobility challenges and then could not be able to visit a SSNIT office.

Arrangements

In view of that, he said, there were alternative arrangements where “if you call us we would come to where you are and we would biometrically authenticate you”.

He said for people who had not come to authenticate themselves, “whose money we have withheld, we have about GH¢480 million so far”.

“There’s GH¢480 million that we could have paid out that we have not paid.

“This is because those people to whom it belongs have not come back to tell us that they are alive. So that is what we call ghost pensions,” he emphasised, and “as and when they resurrect, we stand ready to pay them,” he said.

Background

In 2014, participants in the SSNIT pension scheme, including retirees, were instructed to undergo biometric registration. This phased exercise, conducted in collaboration with employers, aimed to collect biometric data from existing contributors and generate 13 alphanumeric social security numbers for those with eight-digit numbers.

Additionally, the project sought to gather additional information on existing policyholders of the National Health Insurance Scheme (NHIS) and individuals registered with the National Identification Authority (NIA).

The biometric data collected would facilitate swift and straightforward verification of the identities of SSNIT contributors in the future.

SSNIT, a statutory public Trust established under the National Pensions Act, 2008 Act 766, is entrusted with administering Ghana’s Basic National Social Security Scheme. Its mandate includes overseeing the First Tier of the Three-Tier Pension Scheme, making it the largest non-bank financial institution in Ghana.

The Trust’s primary responsibility is to replace a portion of lost income for Ghanaian workers due to Old Age, Invalidity, or Death, with dependents receiving lump-sum payments. It is also tasked with providing Emigration benefits to non-Ghanaian members leaving Ghana permanently.

Established in 1972 under NRCD 127 to administer the National Social Security Scheme, SSNIT originally operated as a Provident Fund Scheme. In 1991, it transitioned into a Social Insurance Pension Scheme governed by PNDC Law 247.

Subsequently, Act 766 of 2008 reformed the pension scheme in Ghana, replacing all existing schemes, including Cap 30. In 2014, the National Pensions (Amendment) Act 883 further modified certain provisions of Act 766.

In Ghana, there are over twelve million workers, but only about two million are protected by pension plans, according to Minister of Pensions, Employment, and Labor Relations, Ignatius Baffuor-Awuah, .

Mr. Awuah made this statement during the 55th anniversary celebration of the Ghana Co-operative Credit Unions Association Limited in Koforidua, in the Eastern region.

He urged the credit unions to collaborate with the National Pensions Regulatory Authority to establish a trust scheme, facilitating savings for informal sector workers’ future financial security.

“We have roughly twelve million people working in Ghana but those who are on pensions are less than two million, which means that many of our people reach their pensions without being on any social security system”, Mr Baffuor-Awuah indicated.

“We have together with the National Pensions Regulatory Authority begun programmes to enrol especially all persons within the informal sector of the economy. But I see a window in the credit unions because there are quite a number of informal operators who also are members of credit unions”, he said.

During the event, the association requested that the government grant its members tax exemptions. Dr. Bernard Bingab, the Board Chairman, emphasized that such an exemption would safeguard the investments of credit unions.

Dr Bingab said: “One of my biggest appeals to our government is tax exemptions for co-operatives”.

“Almost all African countries exempt co-operatives from tax. In recent years the Ghana Revenue Authority has clamped down on credit unions asking some to pay as high as one million cedis. Mr. Minister this is totally unwanted”, he noted.

“This is a group that is there to help the country. Monies that we take as credit unions get back to the pool, so, we have difficulty as to why other African countries have exempted co-operatives and yet the credit unions are being asked to pay tax”, he wondered.

Dr Bingab also noted: “As we navigate the future of credit unions, it is important to acknowledge that just as with any evolving industry, there are both threats and opportunities”.

“The threat of cyber-crimes is significant to us. We have recently engaged the Cyber Security Authority to see how they can help us. As credit unions, we see the way to go is technology but there’s a threat of cyber-crime”, he added.

As pension assets continue their ascent, reaching a total of N17.1 trillion in July, an increasing number of pension contributors and retirees find themselves growing frustrated by the mounting pile of unresolved complaints within the sector.

According to some contributors and retirees who shared their experiences with Financial Vanguard, their grievances often languish in a state of prolonged delay or, in some cases, go entirely unanswered. This situation has given rise to concerns that the National Pension Commission (PenCom) may be struggling to cope with the deluge of complaints that regularly inundate the commission.

Stakeholders argue that this mounting dissatisfaction could be one of the factors motivating certain groups and institutions to seek an exit from the Contributory Pension Scheme (CPS) and revert to the older pension scheme.

Financial Vanguard’s investigation, based on PenCom’s data, reveals that during the first quarter of 2023 (Q1’23), a total of 59 complaints regarding non-remittance of pension contributions were submitted to PenCom. Shockingly, only nine of these complaints were resolved, leaving a staggering 84.7 percent of the grievances unresolved during this period.

Similarly, in the fourth quarter of 2022 (Q4’22), there were 82 recorded complaints, with a mere seven of them reaching a resolution, resulting in a staggering 91.5 percent of the complaints remaining unresolved within that period.

During the third quarter of 2022 (Q3’22), PenCom received eight complaints, of which only one was successfully resolved within that timeframe. In the second quarter of 2022 (Q2’22), a total of 89 complaints were submitted to PenCom, with just eight achieving resolution, indicating that a substantial 91 percent of the complaints remained unresolved during that period.

It’s worth noting that while PenCom provides data specifically for complaints related to non-remittance of pension contributions, the commission acknowledges that it regularly receives various other types of complaints. These encompass issues such as non-payment or delays in receiving accrued pension rights for retirees of Treasury Funded Ministries, Departments, and Agencies (MDAs); requests for resolution of multiple PIN registrations; delays in the approval of transfers to Retiree Life Annuity (RLA); delays in the approval of programmed withdrawal, temporary access to 25 percent of funds, residential mortgage, voluntary contributions, and NSITF; delays in data-recapture; as well as RSA transfer-related complaints.

Commenting on this situation, Comrade Bisan Olufemi John, Secretary of the Nigerian Union of Pensioners Contributory Pension Scheme (NUPCPS), expressed that the government’s pension arrangement still falls far short of being favorable to both contributors and retirees. According to John, the government’s top priority should be improving customer service and the welfare of pensioners and workers.

John said: “There is no way the government can successfully tackle the myriads of economic challenges without adequately satisfying the yearnings of both pensioners and those workers currently in service. The Federal Government has been struggling with getting the economy to work, but one thing that is clear is that the people are the ones that will contribute mainly to make such a reality come to be.

“The government must first think of the workers, improve on their welfare so they can then contribute their quota adequately to the economy. It should be the people before the economy.”

Also speaking, another pension contributor, Mr. Malachy Eze, stated that the slow response of the pension industry in resolving complaints is having a negative impact on the pension scheme.

Eze said: “Government has failed in many instances to pay group life insurance claims to next-of-kin of deceased civil servants. Scenarios like this should never arise, rather government must provide better opportunities for workers and pensioners to be happy.

“Retirees’ welfare should not just end at the level of being paid their stipends.”

Also speaking, a NUPCPS member, Comrade Olagbayo Johnson, said it is unfortunate that the CPS appears to be failing.

There was a significant 80.81% decline in activity within the secondary bond market during the previous week, resulting in a total transaction volume of GH¢17.34 million.

This reduction was primarily associated with the cautious approach of investors, who demonstrated hesitancy in evaluating cash coupons linked to new bonds.

The drop in activity was partly attributed to decreased trading volumes observed across the 2027-2030 maturity periods of the recent bond issues.

Simultaneously, bond prices experienced consistent upticks, driven by the latest coupon disbursements made by the government.

In light of these developments, it is anticipated that the end-of-month portfolio adjustments conducted by pension funds and other asset managers will contribute to increased activity within the bond market.

Employees facing economic hardship are increasingly tapping into their pension savings held in Retirement Savings Account (RSA) due to financial difficulties, as indicated by recent findings.

Vanguard’s investigation reveals that in the first quarter of 2023 (Q1’23), RSA account holders under the Contributory Pension Scheme (CPS) withdrew a total of N3.02 billion from their Additional Voluntary Contribution (ADV). This amount marks a significant 240.1 percent increase from the N887.9 million recorded in the fourth quarter of 2022 (Q4’22).

According to the report from the National Pension Commission (PenCom) for Q1’23, the number of RSA holders making withdrawals from their ADV rose quarter-on-quarter (QoQ) to 1117 during the period, representing a 94.6 percent increase from the 574 withdrawals in the preceding quarter (Q4’22).

Additional Voluntary Contributions (ADV) are supplementary funds that workers can choose to add to their mandatory pension contributions, serving as additional retirement savings.

Under the Pension Reform Act (PRA) 2014, employees are allowed to make ADV contributions to their RSA in addition to their compulsory pension contributions, with the aim of enhancing their retirement benefits.

In terms of RSA registrations, Stanbic IBTC maintained the largest market share of 28 percent with 23,586 new registrations during Q1’23. Access Pensions Limited followed with an 11 percent market share and 9,546 new registrations, while ARM Pension Managers Limited ranked third with a 9.2 percent market share and 9,546 new registrations.

On the other hand, NPF Pensions Managers and Nigerian University Pension Management Company had lower numbers of new RSAs with only 131 and 179 respectively, representing a small fraction of total registrations. Guaranty Trust Pensions Managers Limited recorded 879 new RSAs, accounting for 1.1 percent of total registrations.

After nearly a decade of discussion over the restricted investment possibilities for employee retirement contributions, pension money will soon be invested in the real estate market.

This is because the National Pensions Regulatory Authority (NPRA), regulator of the pension space, has disclosed that the Pensions Act, Act 766, is being reviewed to diversify investment options of pension funds from the current fixed income market to other sectors – such as real estate, private and debt equities – in what could be described as a win for the economy.

The move became necessary following the Domestic Debt Exchange Programme (DDEP), NPRA’s Chief Executive Officer, Hayford Attah Kruffi, told the B&FT in Accra on the sidelines of a winding-down ceremony of the Swiss Secretariat for Economic Affairs (SECO)-supported project with the Authority.

“The NPRA is reviewing the investment guidelines. In fact, the sector minister has given me a deadline to complete the review and get back to him; so that we can undertake some kind of forbearance and also encourage trustees to move into some kind of alternative investments, rather than just the traditional investment areas.”

The NPRA investment guidelines guide trustees as far as investment of pension funds are concerned, primarily government bonds.

The review comes as no surprise, as implementation of the DDEP has shown that overexposure of pension funds to government papers will not only affect the retirement income of workers but literally bring the business of corporate trustees to the brink of collapse – with dire consequences for the business of other pension-related service providers with its related unemployment issues.

Some of the investment areas under consideration include real estate for example, Mr. Krufi said, adding that the funds will be allowed to be invested in private equity and private debt equity, among others, going forward.

The review’s overarching goal, he explained, is to ensure that “we can move away from the fixed income market or diversify pension investments in the country”.

Asked when the review will be completed, he responded “very soon” without giving a specific timeline. He added that: “We have to consult our stakeholders. As regulators, we don’t hold a repository of knowledge. Before you can have a very effective review, you have to ensure that all your stakeholders are on board”.

Reacting to whether the review process is long overdue, he said the existing law has served a good purpose and helped grow pension assets to about GH¢50billion – explaining that in an economy time changes, and “you will also have to review your investment decisions. For example, when you want to invest now, you have to consider things like the environment, governance and the rest. These things were not part of investment decision-making some years ago, but because of changes in society…”

The need to rethink investment options for pension funds was supported by Dr. Simone Haeberli, deputy Head of Mission and Head of Cooperation for the Swiss Embassy in Accra.

She said: “We saw through the current economic challenges and the debt exchange programme that, maybe, there is a need for a review of the Pensions Act; because pensions should have other opportunities than just investing in government bonds. This is something that needs to be looked into and government is already taking care of it; and I think that is a very good step for the pensions industry’s future”.

SECO project

In 2008, Ghana’s pension system was reformed with passage of the National Pensions Act 2008 (Act 766). The Act introduced the contributory 3-Tier Pension Scheme and established the National Pensions Regulatory Authority (NPRA), among other key provisions that seek to improve the country’s pension benefits and administration.

As a young regulator, the Authority faced a number of challenges in meeting its mandate. Therefore, the NPRA through government requested support from the Swiss government through the Swiss Secretariat for Economic Affairs (SECO) to provide needed capacity for the Authority to help it become a credible regulator.

The two-phase project started in 2014 and the second phase began in 2019. The total amount financed by Switzerland was 4.2 million Swiss Francs (approximately GH¢50million).

The project was aimed at strengthening institutional capacity with regard to supervision and regulation: including strengthening the NPRA’s governance and management structure; developing the NPRA’s legal and regulatory framework as well as supervisory compliance policy and programme – namely developing a Risk-Based supervision (RBS) strategic framework among other elements.

The project achieved among others the establishment of a Risk-Based Supervision System to provide efficient and effective supervision and regulatory oversight of the entire pension industry.

The project has been successfully completed, with some of the key results being the following: training the board of directors and management of the Authority to help create synergies in governance and management of the Authority; the establishment and implementation of a Transitional Risk-Based Framework and supervision systems for the Authority; and strengthening the Authority’s supervisory compliance, especially in its SSNIT oversight.

“The NPRA expresses its profound gratitude to the Swiss government for the support that has strengthened the Authority’s governance structure and enhanced its supervision and regulatory functions.

“The Authority is also grateful to the government of Ghana and its agencies which also provided assistance and support to facilitate the project’s implementation,” a statement from NPRA read.

Corporation beyond SECO

“We have quite a large investment or cooperation portfolio with government and the people of Ghana. Ghana is one of our longstanding partners in Africa, and we work along various fields ranging from micro-economic support to decentralisation support. So one of the large, incoming projects is to support the District Assemblies’ Common Fund to perform very well. We are also very active in the financial sector,” Dr. Haeberli noted.

She added that her country is also looking to cooperate with the Ghana Stock Exchange, Ghana Commodities Exchange, in addition to some value chain activities: “Aside from cocoa, we are supporting producers of cashew nuts and oil palm to improve productivity. We are also in collaboration with the Ministry of Energy to promote renewable energy – cleaner energy sources and efficiency with the aim of promoting a cleaner Ghana”.

The self-employed and employees in the informal sector have been urged to join the Social Security and National Insurance Trust (SSNIT) Pension Scheme, which would provide them with a retirement income when they are unable to work.

Mr. Charles Akwei Garshong, Public Affairs Manager of SSNIT, who gave the encouragement, cautioned the self-employed against preferring treasury bills to the SSNIT Pension Scheme, saying, “Investing your money in treasury bills will not yield you more returns than what SSNIT will be paying you during your retirement.”

He said apart from regular annual increases on pension allowances, SSNIT also paid any contributor who is declared unfit (invalidity pension) to continue working, monthly pension allowances no matter his or her age before being declared unfit to continue working.

He was speaking at a sensitisation workshop for media practitioners in Tamale on the SSNIT Pension Scheme to equip them with information to help create content to encourage the self-employed and workers in the informal sector to join the SSNIT Pension Scheme.

Participants were drawn from the Northern and Upper East Region.

The sensitisation workshop was in line with the Self-Employed Enrolment Drive (SEED) of SSNIT, which focuses on extending pension coverage to the self-employed and workers in the informal sector.

Statistics show that about 85 percent of the country’s economy is informal, comprising 6.7 million self-employed people from a total working population of 9.9 million.

However, only about 34,000 active SSNIT contributors are self-employed.

This necessitated the SEED, which was a repackaging of the tier one pension, to provide social protection to such workers (self-employed and workers in the informal sector) by providing them with a regular source of income during retirement.

He reiterated that the SSNIT Pension Scheme was not created for just public and formal sector workers but for all workers in the country, including the self-employed and informal sector workers.

He said SSNIT was focused on reducing old-age poverty, which arose when people did not have pensions to rely on, hence the need for the self-employed and workers in the informal sector to join the pension scheme.

A pension scheme project being tested by the Ghana Cocoa Board(COCOBOD) has received positive feedback from cocoa farmers in Anomawobidi and Wassa Manso in the Western region’s Mpohor and Ahanta West Districts.

Launched at New Edubiase in the Ashanti Region in August 2021, the scheme, when operational, would target about 800,000 registered cocoa farmers benefitting from a retirement plan to promote their lives.

A separate engagement was held between the farmers and Mr Fiifi Boafo, the Head of Public Affairs, COCOBOD, at Anomawobidi and Wassa Manso, to discuss the modalities, processes of registration, and benefits for farmers under the Cocoa Management System.

Some of the farmers, who spoke with the Ghana News Agency, said they were “really in love” with the initiative which would give them relief in their old age.

They, however, wished that COCOBOD would institute prudent management systems that ensure the sustainability of the scheme no matter which government was in power.

Mr Vincent Fynn, a cocoa farmer, pleaded that a school policy be activated along with the scheme, to enable the farmers to access scholarships for their children’s education.

“We have many brilliant children here, but due to the lack of finances, many of them cannot climb higher on the educational ladder…we really need directions and assistance to end the cycle of poverty among rural farmers like me,” he said.

Mr Benedict Ghansah, another farmer, complained about the poor road network, lack of potable water and electricity in the Anomawobidi community and stressed the need for COCOBOD to redeem their promise to help address the situation.

Giving further details of the scheme, Mr Boafo said a five per cent contribution would be deducted from every bag of cocoa sold at the depot, after which the government and COCOBOD would add one per cent to support the scheme.

“For example, if a bag of cocoa is GHS800, five percent will give you GHS40.00 and this is what is set aside for it to grow so that at old age you will benefit from a lump sum,” he explained.

He said the fund was regulated and bound by law and no government could change it.

He further indicated that the National Pensions Regulatory Authority (NPRA), had already developed the modalities with nine trustees in place to ensure the prudent management of the scheme.

The goal was to provide life security for organised cocoa farmers during their retirement age, giving them a year-on-year withdrawal benefits to help meet some pressing needs.

“Each contributor is also entitled to a lump sum and monthly benefits at the ripe age of the scheme, and we are using the cocoa registration card as a basis for membership, and you should be a cocoa farmer to benefit from the programme,” he said.

Additionally, the cocoa card is what would be used for the distribution of farm inputs and called on farmers who had not yet registered, to do so on time.

He said the tier 3 Pension Scheme was managed by Trustees to ensure transparency and good governance and encouraged the farmers to sustain the enthusiasm demonstrated for the successful roll out of the scheme.

In central Paris, protesters and police have once more exchanged blows over the French government’s proposed pension reforms.

Police fired tear gas to disperse the thousands of protesters who set fires and some of whom tossed firecrackers at them.

Since President Emmanuel Macron chose to enact the divisive measures to raise the retirement age from 62 to 64 without a vote, there have been two nights of disturbance.

No-confidence motions have been filed against his government in response.

The first was signed by independents and members of the left-wing Nupes coalition in parliament, while a second came from the far-right National Rally party.

Both are expected to be debated early next week.

Marine Le Pen, leader of the National Rally MPs in parliament, called the decision to push through the pension changes “a total failure for the government”.

Police made dozens of arrests during the unrest at Place de la Concorde, not far from the parliament building.

Protests also took place on Friday in other French cities – notably Bordeaux, Toulon and Strasbourg.

“We won’t give up,” one demonstrator told AFP news agency. “There’s still hope that the reform can be revoked.”

Another told Reuters that pushing the legislation through without a vote was “a denial of democracy… a total denial of what has been happening in the streets for several weeks”.

The government has said the changes to pensions are essential to ensure the system is not overburdened and prevent it collapsing.

But many people, including union members, disagree and France has now seen more than two months of heated political debate and strikes over the issue.

Transport, public services and schools have all been affected, while a rolling walkout by waste collectors has seen thousands of tonnes of rubbish left on the streets of the capital.

Fuel deliveries have also been blocked and there are plans to stop production at a large refinery in Normandy in the coming days.

“Changing the government or prime minister will not put out this fire, only withdrawing the reform,” said the head of the moderate CFDT union, Laurent Berger.

Investment guidelines are both consumer protection and risk management tools that put checks and balances on the players entrusted to invest the “sweat” retirement capital of workers for safe but fair returns. They are also used to direct patient pensions capital into productive sectors of the economy, so it acts as a balancing tool between consumer protection and impacting on the economy.

With private pension funds having grown from GHS6.79bn in 2016 to GHS22bn in 2020, new investment guidelines have been gazetted and introduced in the private pensions industry by the National Pensions Regulatory Authority (NPRA) with the intent to have pensions impact more on the economy. This is the third guideline that has been introduced since the beginning of private pension regime in 2010.

The 2011 guideline was very conservative with the type of asset classes and rightfully so. The 2017 guideline introduced Bank Securities, Infrastructure Bonds, Cocoa Bonds, Private Equity Funds, Unit Trusts, Mutual Funds and Exchange Traded Funds, that hitherto did not exist, to essentially expand the assets classes and to impact on the economy. The 2020 guideline has also added more products, ie. Private Debt Funds, Repurchase Agreements, Direct Property Investments, Project Finance, Green Bonds and also introduced a mandatory Constituent Fund, making a wide range of investment and securities products available to the Fund Managers.

Reading from the new guidelines, it will be observed that whilst more high risk products have been introduced that will benefit the development of the securities market and investment banking in general, certain limits and conditions that put checks on the service providers have been relaxed or made flexible, with little or no recourse to them once they are working within a guideline which the Regulator has approved. Also it gives an impression that the new guidelines were prepared more with what players especially Fund Managers can make from the funds and its impact on the stock exchange, investment banking landscape and the economy rather than the protection of consumers for a safe return. It took sixteen years to review the 2011 guideline but in just three years the 2017 has been reviewed. Have we allowed the 2017 guideline enough time to exhaust its impact and its usefulness? What structural changes have all of a sudden happened in the economy and investment market that will allow the funds to take advantage of, for better returns?

The paramount interest for private pension funds is adequate retirement income for the worker through safe and fair returns and not just to collect contributions from workers to help develop either the stock market, investment banking products and support Governments fiscal policy and projects. If the stock market is doing well, investment products and instruments are safe with fair returns and Government projects have good cash flows, private pension funds will naturally flow into them to support the economy. It is neither a social fund or free money just because the funds can be available for a relatively long term.

Let’s go through the key changes and additions made in the new investment guidelines and give an opinion.

RISK INVESTMENT AND RISK MANAGEMENT COMMITTEE (IRMC)

A Risk Investment Management Committee (IRMC) has formally been introduced and this is laudable. The role of the IRMC is to determine the acceptable risk appetite of the scheme by putting in place the needed risk tolerance limits and is a good corporate governance tool. The challenge is that it has been made mandatory for all schemes.

In my opinion, it should have been limited to the Corporate Trustee as a corporate entity at their Board level and only standalone Employer Sponsored Schemes. Employer Sponsored Schemes are big enough to be self-managed and are not under the control of the Board of that particular employer, hence must have an IRMC. All other schemes that are registered by the Corporate Trustees in terms of corporate governance are under the direction and control of the Board of the Corporate Trustee, hence the IRMC at Board level would have been the appropriate body to be responsible for all investment risk management for the registered schemes. Why must every registered schemes have an IRMC?

The individual schemes registered by Corporate Trustees are not likely to afford the type of financial risk management expertise needed for each scheme. Who is going to be responsible for the cost of such committees since the skillset will not come cheap? Is it also likely that individual schemes might not even generate enough fee income to afford such a committee? Should the IRMC be at the board level of the Corporate Trustee, the IRMC would be taking care of all the schemes and the fees will have to be borne from the resources of the Trustee and not the schemes? This should be reviewed again to limit it to only the Board level of Corporate Trustees and Employer Sponsored Schemes to avoid practical implementation challenges and unnecessary cost to the schemes.

The Corporate Trustees must bear in mind that the fiduciary relationship is between them and the contributors and not the Fund Managers hence as it stands, the IRMC must at the scheme level put in place investment policies that will put checks on the Fund Managers who want to take advantage of the flexibilities in the new guidelines. At the end of the day, as Trustees, you are on your own should anything go wrong.

ALLOCATION TO GOVERNMENT OF GHANA (GoG)

GoG Securities

This has been increased from 60% to 75%. The reason being that there are limited investment products and pension funds have willingly been seeking grants of waivers from the Authority to exceed the GoG maximum allocation. Whether or not the request to exceed GoG maximum allocation were willingly made by the Corporate Trustees or by compulsion is another issue. Once the NPRA was in 2017 made to report to the Ministry of Finance as a second Ministry aside the Ministry of Employment and Labour Relations, it was not far-fetched to realise that the private pension funds were going to be targeted as a source of balancing the government’s debt financing and re-financing needs.

NPRA reporting to two ministries is a governance challenge more so when pension is more of a labour relations issue from the perspective of protecting consumers to secure fair and safe returns whilst impacting on the economy than government financing but this discussion which is of course debatable would be left for another day. NPRA has the power to grant waivers but for transparency, NPRA should be able to publish all the schemes, who ask for waivers, and by how much they exceed their limits for public consumption.

Local Government and Statutory Agency Securities

This involves Municipal and Local Government Bonds, Cocoa Bonds/Bills as well as Statutory Agency Bonds/Bills. and has been increased from 15% to 25% with the limit of maximum of 5% per issuer removed. Adding this to the GoG securities of 75 % technically gives government a 100% access to the private pensions funds with no per issue limits. Either it is to ratify the difficulty in rebalancing the portfolios of those who asked to exceed the limits, since waivers cannot be in perpetuity or there is an unseen influence.

If all funds go to government then we have created what the old SSNIT used to be, where governments have used pension funds as a lender of last resort for both liquidity management and political social projects that have no economic returns. If governments can technically have access to 100% of the private pension funds which can also be used to refinance existing debts with no underlying economic projects, then how does it impact on the economy?

Private pension funds are not welfare funds for social interventions but are pure capitalist funds that require economic returns and cash flows. They can be used to build a three lane highway road from Accra to Kumasi but need to be tolled and collections made by the investors over a period to make economic returns with steady cash flows.

Governments being able to have 100% of the funds is a concentration risk no matter how it is seen since government policy can impact negatively on these funds. A Government in distress can exchange original securities for new ones with less favourable terms and here, the scheme either accepts the lower returns or takes a “haircut”. This actually happened to some schemes that had investment in some of the banks that recently collapsed. You better cut your losses than have 100% of zero.

ALLOCATION TO CORPORATE DEBT SECURITIES

New asset classes of Green Bonds and Asset Backed Securities (ABS) have been introduced. The percentage of value per issuer as well as percentage of Asset Under Management (AUM) per issue have been increased from 5% to 10%. With total AUM increasing from GHS6.76bn in 2016 to GHS22bn in 2020, increasing the limits unnecessarily puts the funds more at risk. The old limits because of the astronomical growth in AUM, would still have increased the values into corporate debt securities of bonds, debentures etc. With just twelve years of private pensions and retirement payments just starting in 2020, it is too early to double the limits since we are still in the conservative phase of safe returns. In any case, only about 4% of the allocated limit of 35% was utilized as at 2020 so there was room for utilization. Is the investment guideline a securities product development tool for Fund Managers or a pension consumer protection tool?

Asset Backed Securities

Asset Backed Securities (ABS) have been added to Mortgage Backed securities (MBS). ABS are created by pooling together non-mortgage assets, such as auto loans and credit card receivables. What are the acceptable assets and why do we want to do this at this time? A clear opportunity for rogue Fund Managers, banks or other finance houses to off load existing toxic illiquid assets, hardcore loans or receivables to the pensions funds to clean their books if not monitored. Do we have the legal framework for ABS? At least for MBS we have.

Green Bonds

These are bonds that are issued for which the underlying projects must have positive environmental and climate impacts. They have been given 5% allocation that does not count towards the 35% maximum of corporate debts. This will nudge investments into these bonds.

There is currently no official overarching regulation that defines a green bond and the principles that do exist are voluntary rather than legally binding. In practice, many issuers tend to follow the four core components of Green Bond Principles (GBP) of the use of the proceeds, process of the Project Assessment and Selection, Management of the Proceeds and lastly its Reporting. It is recommended that the Regulator, NPRA, must pre-approve any such bonds making sure that the four core components have been met before pension funds are made to invest in them. The reason being that they do not count towards the mandatory limits allocated to the asset class and they can be abused.

ALLOCATION TO LISTED ORDINARY SHARES/NON-REDEEMABLE PREFERENCE SHARES

The allocations remained the same at 20% which still makes more funds available due to the astronomical growth in the AUM over the past years. The challenge is the per issuer limit which was a maximum of 10% of shareholder funds of the corporate entity has been changed to 10% of the market capitalization. The two are different with the former more conservative allowing the pension funds to limit and share the risk with the other shareholders. Using market capitalization increases value at risk to the pension funds since they can be either undervalued or overvalued by the market players to affect the price-to-book ratio. Why do we want to complicate issues? It gives a feeling we just want to develop the securities market with the intended transaction fees going to the Fund Managers without thinking of risks to the contributors’ funds. Meanwhile only about 3% of the allocated 20% was utilized at the end of 2020. Safe and fair returns is the cardinal rule in this early stages of our private pensions space.

ALLOCATION TO BANK SECURITIES

Banks impact more on the private sector economy but the limits were left unchnaged. If they have more patient funds it will impact on more people by way of ability to give relatively long term loans. In any case, the funds have grown so in terms of value, more funds will be available to banks anyway. Perhaps the recent shocks in the banking industry has put the Regulator on caution but still one of the safest aside government securities.

The one week “cooling off” period for matured investments to be reinvested with the same bank after a rollover has been expunged. Now the proceeds must be paid to the custodian banks with no rollover allowed. Was this a mistake? The onus is now with the Corporate Trustees to move the funds around within the banking system. A reduction of the “cooling off” period would have been preferable at this time.

Repurchase Agreements

Repurchase Agreements (REPOS) have been added which will be helpful for the banks to raise short term funds. The bank can sell securities to the pension fund and later buy them back at an agreed price. The type of repo and security should have been specified even if it seems obvious. Maturity periods can range from overnight to a year and some may be open hence limits should have been placed on the type of maturity periods that is permissible. The investment guideline is a financial risk management tool and not a product development tool hence any risks need to be mitigated, unless there are no inherent risks to be mitigated in repos to protect the fund.

More importantly, REPOS operate mainly within the lending and borrowing segment of the money market and so therefore, it is not too clear if allowing pensions in the REPOS markets breaches sections 178(2)(c)(d) of the National Pensions Act, 2008 (Act 766) which states that “a privately managed pension fund shall not make short sales” and “a privately managed pension fund shall not borrow for investment purposes” respectively.

ALLOCATION TO ALTERNATIVE INVESTMENTS

An alternative investment (AI) is a financial asset that does not fall into traditional or the conventional investment asset classes of equity/income or money market categories. Comparably, AIs are complex, not heavily regulated and come with higher degree of risk. They come with high fee structures as well and require a longer investment period for any material gains to be realized.

The allocation to AI has been increased from 15% to 25%. The more one reads the new guidelines the more one notices the influence of Fund Managers and unseen hands in the crafting of this guideline and for what purpose?

In the old guideline, this used to be specifically limited to Real Estate Investment Trusts (REIT), Private Equity Funds (PEF) and External Investment in Securities. The new guideline has added categories of Project Finance, Private Debt and Direct Property Investments which increases the associated risks and likely to benefit private individuals and their businesses. NPRA must keep an eye on the beneficial owners of the businesses where these funds are invested to curb conflict of interest transactions and related party transactions between the Corporate Trustees, Fund Managers and the third parties.

Project Finance

This has been defined by the guideline as a funding/financing of infrastructure, industrial projects and public services using a non-recourse or limited recourse financial structure. Non-recourse projects will entitle the scheme to the profits of the project being financed and no other assets of the borrower can be seized upon default. They normally have distant repayment prospects and uncertain returns.

By the guidelines, all Project finance must have Government or Government Agency participation. Under normal circumstances this should give some comfort but with the recent political climate where a change in government brings most government related projects to a halt even if temporary, it rather poses a risk to the pension funds more so when it is on non-recourse basis.

Financing of industrial projects can be complex especially once Government is involved with the apparent political risk. Once not completed the pension fund is stuck with a “white elephant”. Since the only collateral is the project, once started there is the likelihood of cost overruns which the scheme has no choice but to keep on investing more funds till it is completed. It is not easy cutting your losses or disposing off such projects that may be specialised in nature with no alternative uses. For example, building a new stadium, who are you going to sell it to?

The board of Corporate Trustees and executives together with the Fund Managers who advised and decided to venture into such non-recourse investments that fail must be prosecuted for causing financial loss to the scheme. If it goes well good luck. How is the guideline protecting the pensions funds with a non-recourse financing arrangement? With the high political risk in such government related industrial or public services projects it should be expected that it will be with recourse to the Government. This is obviously an arrangement for Governments to avoid contingent liabilities but at whose cost? Is it the pension funds?

If the borrowers believe in what they want the financing for, they must, at least till the project is completed be with recourse to them. Once the cash flows have been properly ascertained, to be in control of the project risk management, avoid cost overruns possibly through corruption and eliminate political risk, the private pension funds might as well take the Government out and finance these projects on a Build-Operate-Transfer basis, through Special Purpose Vehicles (SPVs). We do not want another old SSNIT type of arrangements where Governments directed pension funds into projects they took credit for but the liability solely falling on SSNIT at no economic value. The challenge is, do the Corporate Trustees have the expertise in project finance evaluation and risk management?

Private Debt Funds

These are investment pools that extend debt to privately owned companies as a form of debt financing or source of capital. The beneficial owners of these companies must be known otherwise, private pension funds will be used by some rogue Fund Managers and Corporate Trustees to finance their companies and that of family and friends. There is the possibility of replacing their existing stakes in distressed companies with the pension funds and walk away as long as they are within the NPRA guidelines.

If we want pension funds to support private businesses, which is acceptable, the risk will be minimized if the money is channeled through the banks as investment, for the banks to on lend to the businesses since they have the expertise to assess the credit risk. The risk can be transferred to the banks by way of direct investment but for syndicated loans. At the end of the day the pension fund is not directly taking up the risk of a company but would get the funds back from the bank with a fixed known return even if the business is not doing well due to economic downturns. Private Debt Funds may be introduced later but not at this time when COVID has added another layer of risk to businesses and made the economy unpredictable. Private pension funds are not social or “stimulus” funds.

Here again, the board of Corporate Trustees and executives together with the Fund Managers who advised and decided to venture into such investments must be prosecuted for causing financial loss to the scheme if there is a default, if the risk could have been avoided or there exist traces of conflict of interest deals.

Direct Property Investment

This is defined by the guideline as real estate property purchased or developed through direct investment by a scheme. Unlike REITs, where the schemes invest in real estate without owning or managing the properties, this is directly buying and owning of residential and commercial properties such as office buildings, industrial parks, retail complexes and shopping malls which must be for economic returns.

Somehow the guidelines, requires that all direct investments in Real Estates to have Government or Government Agency’s participation which should ordinarily give some comfort. Are Governments into economic real estate development? I just hope we are not looking at affordable housing social schemes by Governments. In as much as private pension funds are to impact the economy they are not welfare or social funds.

The caution is not to allow pension funds to be used to off load locked up funds of real estate developers in properties they are not able to get the needed rental incomes or buyers or no more interested in. Just satisfying the conditions laid down in the guidelines to transfer risk to the private pension funds should be a concern eg. releasing equity in some non-economic SSNIT projects for liquidity purposes.

The NPRA now has dual reporting lines to the Ministry of Finance and Ministry of Employment and Labour Relations, each with different motives. Between the two Ministries who wins the battle of interplay between protecting consumers and public finance? Do the Corporate Trustees and the Regulator have the expertise to evaluate and take such decisions or approve such direct property investments? Are we ready for this in just twelve years of introducing private pensions?

To deal with this, the Corporate Trustees may need to set up a Special Purpose Vehicle (SPV) with the expertise, pool funds together to share the risk in venturing into this.

CONSTITUENT FUNDS

Under Regulation 22 of L.I. 1990, a registered scheme may consist of a single constituent fund or two or more constituent funds which shall be approved by the Authority. Once a scheme decides to have multiple constituent funds, each fund is to have different investment policies.

Now the new guideline has made it mandatory for tier 2 schemes to use the Constituent Fund Structure on the basis of age differentials with members being elected into particular age brackets as follows:

Constituent Funds for Tier 2 Schemes shall comprise:

Type of Fund

Age Bracket

Fund 1 – Moderately Aggressive Portfolio

Default – 15 to 44 years

Fund 2 – Moderately Conservative Portfolio

Default – 45 to 54 years

Fund 3 – Conservative Portfolio

Default – 55 to 60 years

Fund 4 – Aggressive Portfolio

By formal request

There are both legal and operational challenges with the above mandatory requirement. Legally, the law makes it optional for the Corporate Trustees to make that choice but the guideline is making it mandatory. This is an issue for the Corporate Trustees and as they say what was the “spirit” of the framers of the law.

Operationally, investment decision that will require such “immunization or liability matching strategies” will depend on the risk profile of the members of the Corporate Trustee or the scheme as well as the value of assets under management, but the guideline is making it mandatory. If this is the case, then the expected minimum bench mark returns should have been indicated for each category to protect the consumer. If that cannot be done, then Constituent Funds should not have been made mandatory.

This will only create new Constituent Fund products by Fund Managers where the basket of assets being invested in cannot be questioned by the Corporate Trustees leaving pension funds in the hands of maverick Fund Managers with little room for the Corporate Trustees to rebalance their portfolios. Fund 4 which is the “Aggressive Portfolio” for example is by formal request from a scheme member. Also the rules in paragraph 106 of the guideline allows the contributor with formal application to the Trustee, to switch from one Fund Type to another within a given scheme, once in twelve (12) months without paying fees, subject to exceptions when 55 years.

How financially sophisticated are the contributors to take such decisions? Contributors by this arrangement will need independent financial advice to be able to take such decisions and Corporate Trustees must insist on that before accepting such an election. Once a member makes that election, what will be the role of the Corporate Trustee towards the member? Does it change from a trust relationship to financial advisory?

Are we trying to move to the American type of Individual Retirement Accounts (IRA) where the member is responsible for her own investment decisions and must rely on financial advice from licensed third parties? In Ghana, Corporate Trustees are not licensed to give financial investment advice hence this falls back to the Fund Managers. Someone must owe a fiduciary duty to the member who is advised to elect to Fund 4 or switch between the Constituent Funds and must be able to be sued for wrong advice. I foresee Fund Managers now directly engaging pension fund contributors, advising them to switch funds, attempting to get powers of attorney from such contributors who opt to switch funds to manage their account for them for a fee. What a complex arrangement? Now between the Corporate Trustee and the Fund Manager who becomes the principal and agent?

Obviously those earning high salaries are in the older age brackets and would have invested for a longer period so most likely to have larger constituent AUMs to attract relatively better rates for the younger age group to be able to benefit from the sort of rates the older group can attract. The younger ones in the age bracket of 15 to 44 years are being forced to belong to Fund 1, which will most likely have instruments with longer dated maturities and more of equities. This will allow for Governments to borrow for longer terms and it will boost the stock market but at whose expense? On the Government side, the impact can only be felt if the funds are used in productive sectors with good cash flows and not to just re-finance existing debt. On the stock market, where are the good stocks? They seem to be in the banking, telecommunication and oil industries? How many are Ghanaian owned? Do we just want to give money to Governments for longer periods and support the stock market for the sake of it?

If the Regulator wants to nudge the industry towards Constituent Funds, then the best it can do is to just indicate the age brackets as done for the schemes who want to have such strategies. Even that the actual age brackets will differ from scheme to scheme and I believe it is for this reason the L.I 1990 made it optional instead of mandatory as a financial risk management tool. What if a scheme has only one member between the age bracket of 15-44 years contributing only GHS200 a month? What financial instruments in Fund 1 can deal with this? Buy shares?

The three-tier pension scheme is just about twelve years which is still infant when it comes to pensions, with the decumulation period having just started in 2020. It will take some good data analytics and financial risk management to make constituent funds mandatory and must be based on some compelling identified risks in the present system.

What will be the motivation or compelling reason for the mandatory introduction of Constituent Funds and the associated complications for contributors with little or no financial sophistication making their own investment choices? It is not surprising that the Working Group recommended a transition period of 12 months for its Implementation.

Does the Regulator want to take responsibility for non-performance of investment portfolios because the Corporate Trustees have been put into strait jackets? What is the role of the IRMC then? What risk are they supposed to be managing with the mandatory Constituent Funds? All that Corporate Trustees have to do now is to profile their clients to fit the pre-determined Constituent Funds and there is no risk appetite to be determined since Constituent Funds are in themselves risk appetite tools. The contributor has been given the power to make an election between the Constituent Funds. Based on what information will the contributor do that? Whose responsibility is it to inform the member of poor performance? How financially sophisticated are the contributors to do that?

In any case as it stands now, I humbly request the Regulator to publish the Assets Under Management (AUM) of all the trustees, the annualized rates of return of the schemes as well as the performance of the Constituent Funds of all the schemes, for the contributors to be able to make informed decisions as to which Constituent Fund to invest in or Trustee to engage. The contributors need perfect knowledge to take decisions as to which Trustee to use so they can take advantage of the porting “window” in the law.

My recommendation, however, is to scrap it for now and keep it as an option in the” spirit” of the framers of L.I. 1990 as a portfolio risk management immunization tool for schemes. As the saying goes “if you show the people the way and prescribe how they should get there, then you should be made responsible for the outcome”. The Regulator will be blamed by the Corporate Trustees and Fund Managers for any poor performance and attribute it to their hands having been tied with the Constituent Funds.

THE PERFORMANCE OF THE 2017 GUIDELINES

The previous 2017 guideline already had the tendency to allow pension funds impact on the economy. It introduced Bank Securities, Infrastructure Bonds, Cocoa Bonds, Private Equity Funds, Unit Trusts, Mutual Funds and Exchange Traded Funds, that hitherto did not exist but specific limits were put in place to avoid concentration risk even with Government of Ghana Securities and to mitigate inherent risks in those new financial products. Consumer protection as well as safe and fair returns was paramount.

The table below shows the asset allocation as at December 2020

Asset Class

Percentage of AUM Allocated(Tier 2 & 3)

Limits

Comment

GoG Securities

65.55%

60%

Exceeded. Limit now increased to 75%

Local Government and Statutory Agency Bonds

14.54%

15%

Almost Utilized. Limit now increased to 25%

Corporate Debt Securities

3.93%

35%

Under Utilized. Limit of 35% maintained.

Bank Securities and Other Market Securities

6.95%

35%

Under Utilized. Limit of 35% maintained.

Collective Investment Schemes

2.06%

15%

Under Utilized. Limit of 15% maintained.

Ordinary Shares/Non-Redeemable Preference Shares

2.95%

20%

Under Utilized. Limit of 20% maintained

Alternative Investments

1.03

15%

Under Utilized. Limit increased to 25%

Source: NPRA 2020 Annual Report

From the table, with Bank Securities being as low as 6.95% of AUM, it is possible some Corporate Trustees will not have the liquidity to pay off maturing retirement benefits because they have over exposed themselves to long term Government Securities, unless of course the contributions and the coupon being received are enough to meet maturing benefit payments. Why should GoG securities be exceeded when there is a lot of room in Bank Securities and other Money Market Securities? The government is competing with the private sector which we say should be the engine of growth.

The listing of the asset classes has been arranged in order of low risk to high risk. Alternative Investments which is the highest of risk and has less regulation was the least utilized yet the limit has been increased to 25%. What is motivating this?

A critical statement under “temporary violations” in the old guideline which was to put a check on Corporate Trustees and the Fund Managers in the case of a temporary violation of the assets allocation limits has been expunged from the new one. It said “pending the rebalancing no further purchases of securities within the relevant asset class shall be made except under long term Government securities where additional securities ought to be purchased”. The import of this was, if you violate the limits only do safe long term Government securities whilst rebalancing the portfolio within a given 60 days’ window. Why has this been removed to give the service providers a field day? Even in the banking sector if a bank violates the capital adequacy ratio, the ability to lend is curtailed.

I get the feeling this new guideline had a lot of influence or lobbying from the Fund Managers. They have been able to remove certain recourse or risks to themselves, put in flexibility in using the funds, introduced their investment products to use private pension funds as a source of funding that hitherto had no funding source either due to the inherent higher risks or other reasons.

CONCLUSION

Yes, private pension funds must impact the economy as it has in other jurisdictions but in those jurisdictions the laws punish those who abuse the funds and projects are undertaken with little or no political risks. The shopping malls, office complexes, road and railway networks that we see in those jurisdictions have economic returns and cash flows.