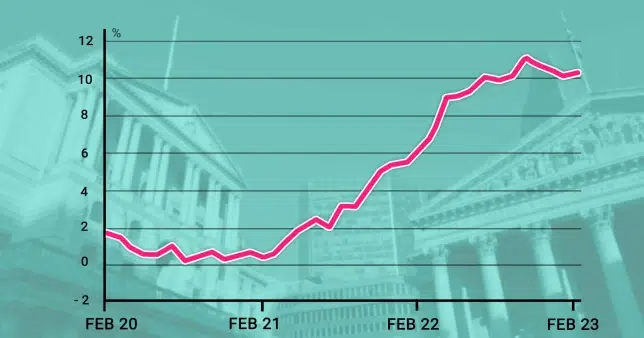

Following Wednesday’s unexpected increase in inflation, the Bank of England declared that interest rates had increased for the eleventh time in the previous two years.

The Monetary Policy Committee (MPC) of the Bank voted seven to two to raise rates from 4% to 4.25%.

In contrast to the 0.4% GDP decline that the Bank had predicted last month, they said they now expect the economy to increase somewhat in the second quarter of the year.

Furthermore, inflation is set to come back down this year despite a surprise increase in Consumer Prices Index (CPI) inflation last month, to 10.4% from 10.1% in January, driven by surging food and drink prices.

The decision marks the 11th time in a row the Bank has hiked interest rates.

It comes after inflation hit a 41-year high at 11.1% in October last year.

The BoE faced a difficult balancing act, weighing up the need to rein in inflation with the worries over banking woes and the possibility they may start to clamp down on lending.

Yesterday’s data – showing inflation rising to 10.4% in February rather than continuing its descent – immediately turned today’s announcement into an almost one-way bet on a quarter-percentage-point increase in Bank Rate.

Last month the raise in interest rates meant it was the highest in 14 years.

The Monetary Policy Committee has voted by a majority of 7-2 to increase the interest rates (Picture: EPA)

A spokesperson from the Bank of England said: ‘Global growth is expected to be stronger than projected in the February Monetary Policy Report, and core consumer price inflation in advanced economies has remained elevated. Wholesale gas futures and oil prices have fallen materially.

‘There have been large and volatile moves in global financial markets, in particular since the failure of Silicon Valley Bank and in the run-up to UBS’s purchase of Credit Suisse, and reflecting market concerns about the possible broader impact of these events.

‘Overall, government bond yields are broadly unchanged and risky asset prices are somewhat lower than at the time of the Committee’s previous meeting.

‘The Bank of England’s Financial Policy Committee (FPC) has briefed the MPC about recent global banking sector developments.

‘The FPC judges that the UK banking system maintains robust capital and strong liquidity positions, and is well placed to continue supporting the economy in a wide range of economic scenarios, including in a period of higher interest rates. The FPC’s assessment is that the UK banking system remains resilient.

‘Reflecting these developments, bank wholesale funding costs have risen in the United Kingdom and other advanced economies.

The Bank of England said the rise has gone up to 4.25%

‘The MPC will continue to monitor closely any effects on the credit conditions faced by households and businesses, and hence the impact on the macroeconomic and inflation outlook.

‘Additional fiscal support was announced in the Spring Budget. Bank staff have provisionally estimated that this could, relative to the February Report, increase the level of GDP by around 0.3% over coming years.

‘A full assessment, including the extent to which these measures could affect supply as well as demand in the medium term, will be conducted ahead of the May Monetary Policy Report.’

Due to a lack of cash, the Covid-19 outbreak, the crisis in Ukraine, and unfavorable mood in the run-up to the August elections, Kenyan corporations have been experiencing difficulties.

As businesses navigate these uncertain times, Marc Merlino, Citi’s Global Head of the Global Subsidiaries Group, visited the area to meet with customers.

The banker was interviewed by Business Daily to learn how they are overcoming the difficulties.

From the conversation you’re having with the multinational clients you bank, what are some of their biggest concerns?

Probably the primary area of concern is the economy. We have had longer-term conversations, strategic discussions with long-term strategic investors looking to build production facilities and employ people and bring multinational expertise to ESG.

The conversations have also pivoted to happiness around the results of the election. And then not so much in terms of who won, but in terms of the peaceful transition of power here. Our multinational clients are always happy when there are stable, predictable, you know, transitions in power.

What about concerns about accessing dollars?

If you look at what is happening, with the Federal Reserve raising interest rates to control historically high US inflation. That action has global implications on emerging market currencies. You know, it is not the Kenyan shilling alone that has maybe lost six percent this year that is under pressure, it is all currencies.

But it’s not just the Fed that raised rates. The Bank of England, and European Central Bank are also doing coordinated monetary policy actions to try and bring down inflation across the board. So yes, there has been what I would call an imbalance in terms of FX demand and supply in the domestic market.

How, do you think, will this imbalance be resolved?

There was elevated demand earlier in the year because of the dividend season. A lot of corporates did not pay dividends during Covid, then they paid in 2022 as a catch-up. So there was significant demand, and we came into an economy that opened up significantly in 2022. Seven and a half percent in 2021 growth means a lot of industries opened up so there was a demand for dollars from manufacturers, oil importers, consumers, capital goods importers, etc.

Kenya imports a lot of consumer goods as well. Lastly, I think this phenomenon was around an abundance of caution going into the election, where you have people holding onto dollars, not because they have no faith in the shilling, but just because of the uncertainty of the electoral period.

But I want to put it to you that the long-term prospects of the shilling are positive, it will stabilise. Supply-demand will normalise and that is a function of time. So a Citi perspective and a banking industry perspective, we do believe that this is just a matter of time before that issue resolves itself.

Citi is one of the banks that have been arrangers for Kenya’s sovereign debt and we saw the cancellation at the beginning of the year. What sort of conversations would you be having with the government in terms of how best to access commercial markets?

We have a very deep relationship with the government of Kenya, and of course, when called upon to assist in the fundraising programme, externally, we will be responsive to that call.

But I think in terms of strategy, in terms of direction, I would refer that question to the Treasury because that’s the authority that will make that decision. Of course, we have our views, and Kenya is a well-regarded and well-known issuer offshore. Having issued in excess of four Euro bonds, Kenya is known in the international market.

So there’s nothing new about Kenya going back to the market once it settles down. We certainly will see Kenya re-approaching the market.

What is the general outlook for sovereign markets?

Most African sovereigns are single B issuers and what we call frontier markets. Frontier markets have seen their yields elevated in the last six to 12 months. Because of that elevated pricing, a lot of the frontier markets have stayed away from issuing Eurobonds so this is not a Kenya phenomenon.

Kenya is not locked out of the market as a country because of something specific that it has done. It’s a broader frontier market phenomenon and sell-off. So I think what you should look out for is what is going to happen on the global stage. Kenya’s long-term fundamentals and prospects are still attractive to the long-term investor.

Do you see the problems around inflation, the rate environment in the big markets resolving soon?

Markets function based on the basic valuation methodology and a market is a discounted present value. But the present value requires you to have a view of the future, and then you discount that based on what a rate is.

The problem is when the view of the future becomes cloudy or uncertain, it becomes very difficult for all the market players.

In terms of portfolio and FDI flows, how do you see this space evolving for Kenya?

Kenya’s prospects remain excellent, we don’t see the long-term customers changing their view because of this temporary dislocation. When we had the election concluded and President William Ruto sworn in, we had flows come back into the equity market, which rallied.

We have seen financial flows exit, but we have also seen corporate flows coming back into the market for long-term investors. On the corporate side, a lot more of the investments that have been delayed have started coming back to the market. Why do I know this? Because we’ve had a good year as Citi-Kenya as client activity has picked up. When our clients do well, our business does well. And that alone is a barometer, the fact that our customers are starting to come back and get on with business.

Who are some of your typical clients here?

We are positioned to focus on three sets of clients. The historical western multinationals that have been here for decades, the emerging champions that are coming out of East Africa, and then the digital champions that are largely being born have been born in the last 10 years.

What is happening now is we are now seeing digital champions. And these are companies that are broadly digital in their approach to things. These are companies that have cross-border ambitions immediately, and there are several great examples.

What happens, in times of greater uncertainty is, we have a lot more conversations with our clients. They are reaching out to us not to get a quote on an FX trade or to talk about a loan or a product. But they want our advice and perspective because things are changing.

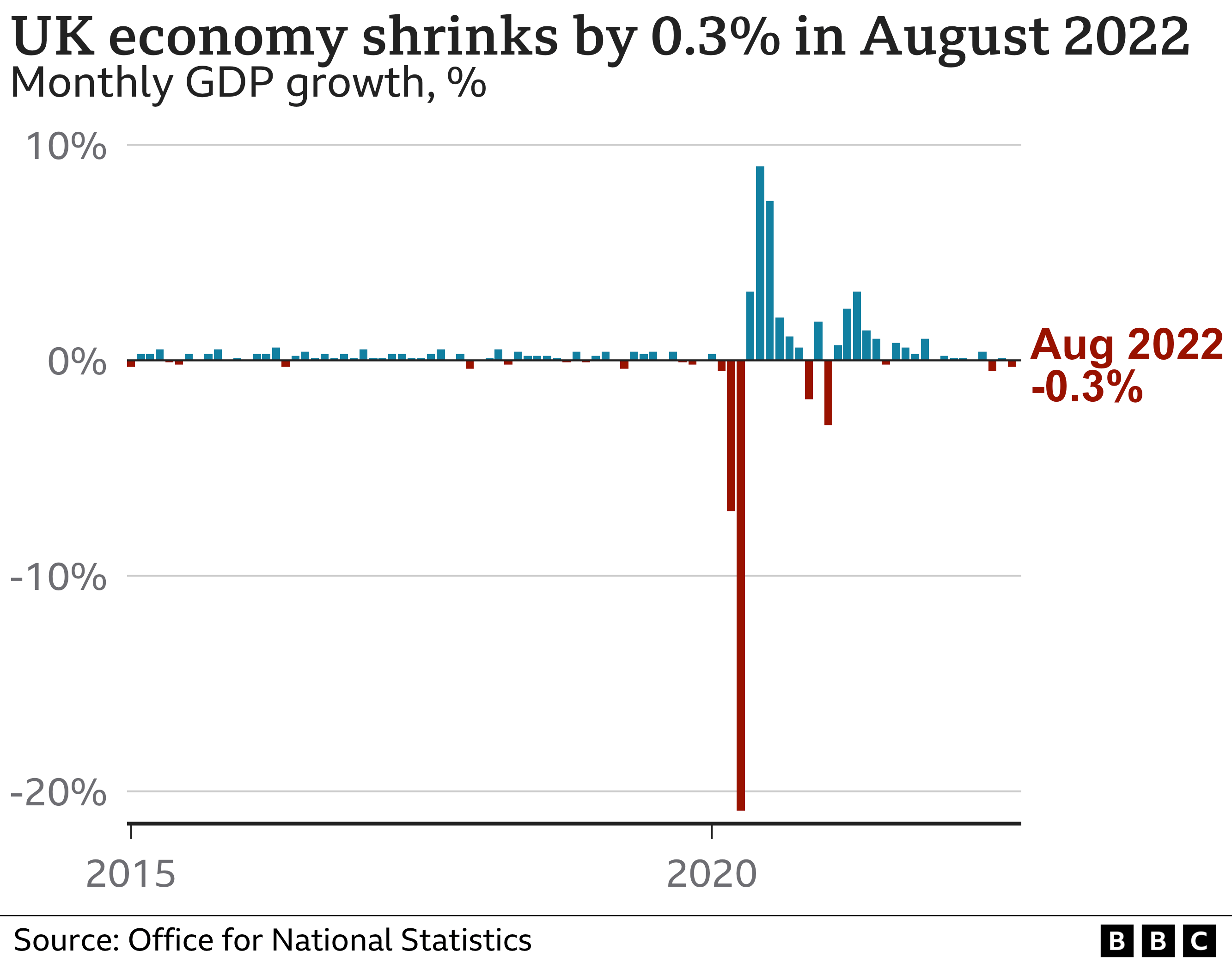

The surprise 0.3% drop came as factories and consumer-facing businesses struggled, according to official figures.

Analysts thought the economy would stall in August but not shrink as costs mount for businesses and households.

Prices are rising at their fastest rate for 40 years, eating into people’s budgets, and outpacing growth in pay.

In normal times, a country’s economy grows and on average, people become slightly richer as the value of the goods and services it produces – its Gross Domestic Product (GDP) – increases.

But sometimes their value falls, and a recession is usually defined as when this happens for two three-month periods – or quarters – in a row, and it marks a sign the economy is performing badly.

The latest data from the Office for National Statistics (ONS) means that in the three months to August, GDP also fell by 0.3%.

The drop in the monthly figure for August was driven by a sharp decline in manufacturing and maintenance work, which slowed down the oil and gas sector, the ONS said.

It marked a fall from July, when the UK economy grew by 0.1%.

What questions do you have on how you might be affected by a recession?

Send your questions to yourquestions@bbc.co.uk

WhatsApp us at +44 7756 165803

Tweet us @BBC_HaveYourSay

Please read our terms & conditions and privacy policy

But ONS Chief Economist Grant Fitzner said that lots of other customer-facing businesses like retail, hairdressers and hotels were “faring relatively poorly” in August.

“The economy shrank in August with both production and services falling back, and with a small downward revision to July’s growth the economy contracted in the last three months as a whole,” Mr Fitzner said.

He added that sports events didn’t generate as much economic value, after the economy had previously been helped by the UK hosting the Women’s Euro Championship in July.

A reduction in the amount spending by the government related to the pandemic was also one of the big causes of the slump in manufacturing, which was hit by pharmaceutical companies cutting back production.

The ONS added that some falls were off-set, however, by some professional services like accounting and architecture.

The construction sector was the only one of the three main parts of the economy to see growth of 0.4% in August.

Some experts expect that September could see an even bigger drop in economic output, with the extra bank holiday for the Queen’s funeral and the period mourning affecting business opening hours, as well as higher costs starting to bite.

Yael Selfin, Chief Economist at KPMG, said that the UK was now “teetering on the edge of recession”.

“The ongoing squeeze on household finances continue to weigh on growth, and likely to have caused the UK economy to enter a technical recession”.

“August’s drop in GDP likely marks the start of a downward trend that will continue deep into next year,” said Samuel Tombs Chief UK Economist at Pantheon Macroeconomics.

Challenges to face

Meanwhile, Suren Thiru, Economics Director for ICAEW (Institute of Chartered Accountants in England and Wales) criticised Chancellor Kwasi Kwarteng’s recent mini-budget for sparking market turmoil and potentially piling extra pressure on firms and families as mortgage rates have been sent soaring.

Mr Thiru said: “The government has needlessly risked a longer recession with any boost from the energy package likely to be dwarfed by a sustained squeeze on UK output from persistently high inflation, punishing interest rate rises and acute financial market turbulence.”

Chancellor Kwasi Kwarteng insisted the government’s energy support package and growth plan will “address the challenges that we face”.

He added said: “Countries around the world are facing challenges right now, particularly as a result of high energy prices driven by Putin’s barbaric action in Ukraine.”

Image source, PA Media

Image caption, The chancellor recently brought forward the date of his plan to balance the government’s finances.

Speaking to BBC’s Today programme, Business Secretary Jacob Rees-Mogg also urged caution in interpreting the most recent ONS monthly figures for August.

He pointed out that monthly figures are often more volatile and “very often subject to revision”.

But he acknowledged that the fall in the economic growth number for August “showed the need for the mini-budget in September to make sure we get back onto a path for growth”.

It comes after the International Monetary Fund (IMF) warned that the worst was still to come for the global economy, while 2023 would “feel like a recession” for many people because of rising costs and the continued fall-out of Russia’s invasion of Ukraine.

The financial institution warned on Tuesday that the UK economy could sharply reduce in 2023 as consumer spending is dented by rising prices and higher interest rates.

It downgraded its forecast for UK economic growth next year to just 0.3% in 2023 – down from 0.5% previously pencilled in.

Rachel Reeves MP, Labour’s Shadow Chancellor, said: “That the IMF yesterday described the “UK like a car with two people each trying to steer the car in a different direction” leaves us an international laughing stock.

She said that the new ONS figures released on Wednesday showed that the UK economy “is still in a dire state because of this Tory government.

“The Conservatives must reverse their disastrous mini-Budget. Any continued failure to do so shows damaging levels of denial from the prime minister and her chancellor.”

The IMF did welcome the news though that the chancellor has brought forward the date for his “economic plan” to 31 October, where he will set out will set out how he will fund tax cuts that he has pledged and reduce debt.

The Bank of England has said it will “not hesitate” to hike interest rates to curb inflation after the pound fell to a record low against the US dollar.

The Bank said it was “monitoring developments closely” and would make a decision on any action in November.

Its statement came after the Treasury said it would publish a plan to tackle debt in a bid to reassure investors.

In Asia currency market trade on Tuesday, the pound rose by more than 1% to top $1.08.

On Monday, some UK lenders said that they were halting new mortgage deals.

Halifax, the UK’s largest mortgage lender, said it would temporarily withdraw all mortgage products that come with a fee due to the market volatility.

Virgin Money and Skipton Building Society have also stopped offering mortgage products to new customers.

Experts said a rise in the cost of long-term borrowing due to the market turmoil meant the cost to lenders of offering new mortgage deals was too expensive.

Sterling fell to an all-time low earlier against the US dollar after Chancellor Kwasi Kwarteng pledged further tax cuts at the weekend on top of Friday’s mini-budget where he announced the biggest tax cuts in 50 years.

The pound had been sliding as global markets reacted to the sharp increase in government borrowing required to fund the cuts.

A weak pound makes it more expensive to buy imported goods and risks pushing up the rising cost of living even further. Imports of commodities priced in dollars, including oil and gas, are also more expensive.

UK inflation, the rate at which prices rise, is already rising at its fastest rate for 40 years.

Some economists had predicted the Bank of England would call an emergency meeting in the coming days to raise interest rates in a bid to stem the fall, as well as calming rising prices.

But the Bank of England instead said it was “monitoring developments in financial markets very closely” and would make a full assessment at its next meeting on 3 November.

Investors are now predicting that interest rates could more than double by next spring to 5.8% from their current 2.25%, to curb high inflation, which is expected to be fuelled by the huge tax cuts announced in Friday’s mini-budget.

‘Not affordable’

Samuel Tombs, chief UK economist at Pantheon Macroeconomics, said if interest rates rise as predicted, the average household refinancing a two-year fixed rate mortgage in the first half of next year would see monthly payments jump to £1,490 from £863.

“Many simply won’t be able to afford this,” he said.

As the deadline of September 30 draws near, many UK citizens are rushing against time to have the £20 and £50 notes they now hold changed by a polymer equivalent.

As many Britons wait in line at its counter, the Bank of England (BoE) has said that it is “experiencing very strong demand” for its services.

The Bank of England Counter is currently open Monday through Friday from 9.30 am to 3 pm and is in high demand.

“There will be lengthy lines, and you might have to wait more than an hour.

When making a trip to the Bank to conduct an in-person exchange, we respectfully ask that you take into account the lengthy wait periods. If you arrive after 2pm, there’s a chance you won’t be served before we close.

Although it is still a legal tender at present, the £20 and £50 notes will cease to be in use and circulation from next month.

People who are in possession of the notes have been asked to deposit them at their banks, some post office branches or with the Bank of England to have them replaced with the polymer version which is said to be “less vulnerable to counterfeiters and more durable”.

According to UK Sky News, the Bank first released the polymer £50 note in 2021, which featured Bletchley Park codebreaker and scientist Alan Turing. This completed the “family” of polymer notes, which also included the £5, £10, and £20 notes.

Following her passing, Queen Elizabeth II’s image is anticipated to eventually be removed on UK banknotes.

Following his accession to the throne, King Charles III’s likeness will be printed on the new currency.