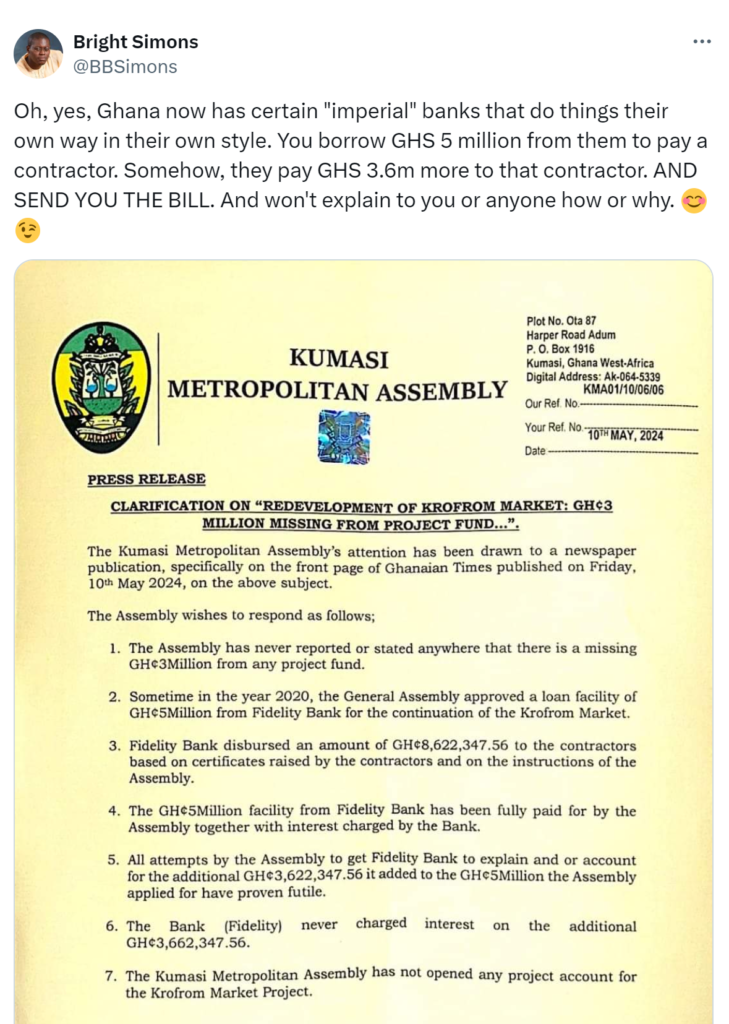

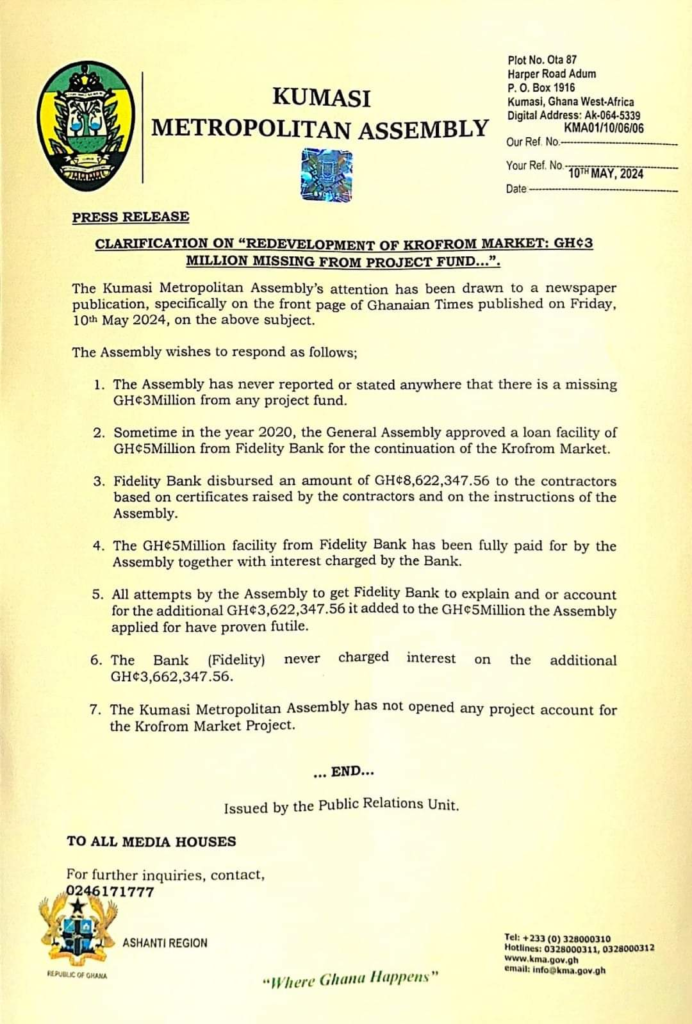

Societe Generale Ghana has been notified that the Societe Generale Group, which holds a 60.22% stake in Societe Generale Ghana, has commenced a strategic initiative.

In a statement dated Thursday, May 9, 2024, the Group added that “If a concrete development were to be decided, a subsequent communication will be made at the appropriate time according to applicable legislation.”

Hakim Ouzzani, the Managing Director of Societe Generale Ghana, clarified that the information circulating about the bank exiting the Ghanaian market did not originate from the Group Head Office in France.

Fitch Ratings had previously forecasted that Societe Generale’s (SG) potential exit from Africa would create substantial opportunities for pan-African banks to expand, either through organic growth or mergers and acquisitions.

“This should stimulate competition and benefit local banking sectors despite some short-term challenges”, Fitch said.

Hakim Ouzzani, the Managing Director of Societe Generale Ghana, clarified that the information circulating about the bank exiting the Ghanaian market did not originate from the Group Head Office in France.

Fitch Ratings had previously forecasted that Societe Generale’s (SG) potential exit from Africa would create substantial opportunities for pan-African banks to expand, either through organic growth or mergers and acquisitions.

“This should stimulate competition and benefit local banking sectors despite some short-term challenges”, Fitch said.

Reports indicate that Societe Generale (SG) is considering exiting Ghana due to challenges related to profitability and stringent regulatory requirements in the financial sector imposed by the regulator.

On 12 April, SG announced the sale of Societe Generale Marocaine de Banques (SGMB) and its subsidiaries to the Moroccan conglomerate Saham Group, following a trend of divestments by French banks in Africa in recent years.

In the past six months, SG has also agreed to sell some of its smaller African subsidiaries and has initiated a strategic review to divest its 52.34% stake in Tunisia-based Union Internationale de Banques. Similarly, other French banks such as BNP Paribas, BPCE, and Credit Agricole have also reduced their African presence over the last decade, with limited operations currently.

The divested subsidiaries may encounter challenges as their risk appetite may be lower than that of local competitors. Furthermore, the exit of highly rated foreign shareholders is often seen as credit negative for subsidiaries. Rating agencies have placed SGMB’s National Ratings on Rating Watch Negative, indicating a potential downgrade upon completion of the sale, as the support from SG may no longer be factored in.

A lower rating or the exit of a foreign shareholder could make it more difficult for the subsidiaries to access the global financial system and correspondent banks, potentially disrupting cross-border remittances, payments, and trade finance activities. However, these challenges are typically short-term, and banks usually have good access to funding from development finance institutions.

“We see significant opportunities for local and regional banks in Africa despite the challenges. Some banking groups with pan-African ambitions should eventually gain enough scale to compete with long-established institutions. Vista Group agreed to acquire several subsidiaries (including some of SG’s) in sub-Saharan Africa in 2023, which would increase its African presence to 16 countries”.

Coris Bank, which operates in 11 African countries, completed the acquisition of SG’s Chadian subsidiary in January and is awaiting regulatory approval for the acquisition of SG’s Mauritanian subsidiary. Vista and Coris are emerging as strong competitors for established pan-African banking groups from South Africa, Nigeria, and Morocco.

The growing competition among pan-African banking groups is expected to stimulate credit growth. French-owned African subsidiaries often face limitations in targeting certain segments of the economy due to their parent bank’s conservative risk approach.

They also adhere to stricter loan classification and provisioning policies compared to locally owned banks, which can hinder growth and profitability. The exit of French banks is anticipated to accelerate credit growth, particularly in lower-risk segments, thereby aiding in maintaining asset-quality metrics.

The withdrawal of French banks from African retail and commercial banking is slightly advantageous for them. They are redirecting their focus to more developed retail banking markets in Europe and activities such as insurance, leasing, and corporate and investment banking, where they can achieve greater synergies.

A reduced presence in Africa aligns with their risk aversion and efforts to optimize risk-weighted assets under European banking supervision, which is more stringent than local supervision for African peers. Additionally, increasing economic uncertainties and geopolitical tensions in some African countries are influencing their strategic reevaluation.