In the aftermath of her loss in the New Patriotic Party (NPP) parliamentary primaries, Dome-Kwabenya lawmaker Sarah Adwoa Safo has quashed rumors suggesting her potential run as an independent candidate in the upcoming December elections.

Asserting her unwavering commitment to the core values of the NPP, Adwoa Safo explicitly stated that she has no intention of running as an Independent Candidate in the forthcoming December 7, 2024, presidential and parliamentary elections or at any foreseeable point in the future.

In an official statement, Adwoa Safo highlighted her enduring dedication to the NPP’s shared values and the collective goal of securing victory in the December 7, 2024, elections alongside Dr. Mahamudu Bawumia in their pursuit to “break the 8.”

‘’My attention has been drawn to several recent misinformation and speculation in the media regarding my political future in the Dome-Kwabenya Constituency in particular and the New Patriotic Party as a whole’’.

‘’I wish to clarify, that despite the setback and outcome of last Saturday’s parliamentary primaries in Dome-Kwabenya, I remain steadfast in my commitment to the shared values of the New Patriotic Party and our corporate quest to break the 8 with H.E. Dr. Mahamudu Bawumia come December 7, 2024’’.

She explained that ‘’As a three-term Member of Parliament and a true party person, I am cognizant of the fundamental principles which underpin the Danquah-Dombo-Busia tradition for which internal competition and afterward cooperation, remains the guiding light’’.

She further used the opportunity to express her eternal appreciation to the good people of Dome-Kwabenya Constituency especially the hard-working Polling Station Executives for the opportunity to represent their interests and aspirations in the august house of Parliament in the last 12 years, adding that ‘’It has been a real honor and privilege working for and with you on matters and issues that border on our common interests and for which I do not take lightly. From the depths of my heart, I say Thank You’’.

‘’For the next few months, I remain dedicated to working collaboratively with the Leadership of the party in the constituency in collectively pursuing goals to unite us for the task ahead in campaigning to maximize our votes for both Parliamentary and Presidential candidates and in Parliament, to execute Government business expeditiously’’ she concluded in the statement posted on her Facebook page.

Adwoa Safo faced defeat at the hands of the Chief Executive Officer of the Free Zones Authority, Mike Oquaye Jnr, who secured over 1194 votes, while Adwoa Safo garnered 328 votes. A third candidate, Sheela Oppong Sakyi, placed third in the contest with just over 100 votes.

Ladies, let’s be honest; the default gift options for our boyfriends often revolve around boxers and singlets. Isn’t it time we added a dash of creativity to the mix? If you’re seeking something unique to surprise your man, here are some imaginative gift ideas that go beyond the usual suspects.

Gadgets for Tech Lovers: For the tech enthusiast, consider trendy and useful items like wireless earbuds or a smartwatch. Every use becomes a reminder of your thoughtful gift.

Food and Drink for the Foodie: If your boyfriend enjoys exploring new culinary delights, go for something special like quality coffee, a set of unique beers, or perhaps some artisanal hot pepper sauces. Add flavor to his day in a fun and delicious way.

Fashion Items that Break the Mold: Swap out the typical boxers or singlets for a stylish leather wallet, a classy watch, or a cool T-shirt from his favorite brand. These gifts are both practical and fashionable.

Experience Gifts for Fun Times: Plan a memorable day out – surprise him with a special date, tickets to a concert, or a game he’s been eager to see. Create lasting memories together.

Gifts Tailored to His Hobby: Consider his hobbies and interests. For a fitness enthusiast, new workout gear or a fitness app subscription could be perfect. If he loves reading, find a compelling book he hasn’t read yet. These gifts show you understand his passions.

Remember, it’s all about bringing a smile to his face. Whether it’s a gadget, something related to his hobby, or planning a special day, what matters most is that you’ve put thought into what he likes. So, step away from the typical boxers and singlets; surprise him with something truly different!

Night blindness, or nyctalopia, extends beyond difficulties seeing in the dark; it signals an underlying issue affecting low-light vision. Let’s illuminate the causes, symptoms, and treatments associated with this condition.

Root Causes: Night blindness can stem from various factors. A prevalent contributor is a deficiency in Vitamin A, crucial for a healthy retina. Other triggers encompass cataracts, retinitis pigmentosa, certain medications, and genetic factors. Awareness and preventive care are essential given the diverse origins of this condition.

Symptoms: Indications are often evident – challenges in transitioning from well-lit to dimly lit environments or struggling with nighttime driving visibility. These signs should not be overlooked, as they may point to deeper health concerns.

Treatments: The positive aspect is that addressing night blindness hinges on identifying its cause. For Vitamin A deficiency, dietary adjustments and supplements prove beneficial. Conditions like cataracts may necessitate surgical intervention. Early detection and intervention are pivotal, prompting timely consultation with healthcare professionals for symptomatic individuals.

Prevention Measures: Prevention surpasses cure. To avert night blindness, uphold a diet rich in Vitamin A, utilize protective eyewear in bright settings, and adhere to regular eye check-ups. Prioritize the well-being of your vision – it’s invaluable!

Night blindness transcends a mere inconvenience; it can be a signal necessitating medical attention. Always heed your body’s signals, stay informed, embrace a healthy diet, and never underestimate the importance of routine eye examinations. Safeguard your vision – it’s your gateway to the world.

When it comes to indulging in a cold beer, moderation is often emphasized, but did you know that beyond being a refreshing beverage, beer can offer some surprising health benefits?

A Toast to Heart Health: Research suggests that moderate beer consumption may positively impact heart health. The alcohol and specific compounds, like flavonoids, in beer can enhance blood circulation and reduce inflammation, potentially lowering the risk of heart disease.

Building Stronger Bones: Beer contains dietary silicon, crucial for bone health. Moderate consumption could contribute to stronger bones, potentially minimizing the risk of osteoporosis.

Boosting Brain Health: Surprisingly, beer may have cognitive benefits. Studies indicate that moderate beer drinking could lower the risk of Alzheimer’s and cognitive impairments, thanks to silicon content that protects the brain from aluminum effects.

Kidney Care with Every Sip: Beer might be advantageous for your kidneys. A study found a link between beer consumption and a reduced risk of developing kidney stones, attributed to the high water content and diuretic effect helping prevent stone formation.

Fights Gum Disease: Hops, a key ingredient in beer, contains compounds with antibacterial properties. These properties can combat oral bacteria associated with tooth decay and gum disease, contributing to better oral health.

While these health benefits are intriguing, moderation remains crucial. Excessive alcohol consumption can lead to adverse health effects.

So, while you enjoy your beer, savor it within healthy limits to maximize these unexpected benefits.

Sipping on your favorite brew can be more than a leisure activity – it’s a toast to your health! Cheers to that!

The Member of Parliament for Ningo Prampram, Sam George, is pressing the Public Accounts Committee (PAC) of Parliament to declare Rev. Dr. Ammishaddai Owusu-Amoah, the Commissioner-General of the Ghana Revenue Authority (GRA), persona non grata.

He asserts that Owusu-Amoah has been working without a government contract since October 2021, having exceeded the retirement age, raising concerns about potential illegality in his position. During a recent Public Accounts Committee (PAC) session, Sam George highlighted the age-related issues surrounding the GRA Commissioner-General.

In an interview on Citi FM, Sam George expressed his intention to formally write to Speaker of Parliament Alban Bagbin and the finance committee, urging them exclude Owusu-Amoah from all Public Accounts Committee’s engagements.

“I know for a fact that the GRA Commissioner-General, since turning 60 years old in October 2021, has not had a contract. This is not the first time I’ve raised this matter directly with the Commissioner-General, drawing his attention to the fact that he’s engaged in illegality,” he said.

He added: “I will be raising this with the Speaker [Alban Bagbin] as well when Parliament reconvenes, drawing the attention of the Speaker and the finance committee to the fact that Dr. Ammishaddai Owusu-Amoah must be declared persona non grata before PAC. We should not entertain someone who has no legal basis.”

“He has engaged in a number of dubious and unscrupulous contracts. The whole country knows about the $100 SML contract. He has been used to carry out all the legalities for Ken Ofori-Atta [Finance Minister]. Why have they kept Dr. Ammishaddai Owusu-Amoah in the post, if not that he’s facilitating corruption and blatant stealing at GRA? This must be a cause of worry for all of us.”

In a notable accomplishment, 22-year-old Adwoa Tima Awuah has earned a coveted spot in the finals of the esteemed Miss Germany awards, a platform renowned for recognizing women for their societal contributions, as reported by Graphic Showbiz.

Miss Germany has transcended traditional beauty standards to become an accolade honoring women actively involved in societal responsibilities and impactful projects benefiting the German community. Adwoa Tima Awuah, the founder of the Yemiyiefo Foundation (YFM Ghana), has secured a place as a finalist, lauded for her outstanding contributions.

Established in 2021, the Yemiyiefo Foundation focuses on supporting young girls in rural areas of Ghana, ensuring their completion of Junior High School (JHS) and transition to Senior High School (SHS).

The foundation has already granted 15 full scholarships to girls in underserved communities for JHS education and conducted Life Skills workshops, reaching over 1000 Junior High School students in the Eastern and Central Regions of Ghana.

In addition to her impactful work in Ghana, Adwoa is actively engaged in a mission to improve the lives of African immigrants in Germany. Her project involves offering psychosocial services to aid the integration of migrants into German society.

Notably, Adwoa Tima Awuah stands out as the youngest and sole black candidate among the top 10 finalists in the Miss Germany competition. The grand finale is set to take place on February 24 at Europapark, Germany.

Articulating her mission at Miss Germany, Adwoa emphasized, “As a former migrant from Ghana to Germany, I know how challenging migration and integration can be, especially without sufficient support. My mission at Miss Germany is to create more empathy for migration and integration with a documentary. I also work at a psychosocial center to support migrants, especially the African community. This trip is more than a mission. It is my connection to my roots, the challenges of my family, and the difficulties of all those who had to leave their familiar surroundings and start anew in Germany.”

On January 26th, 2024, a heartwarming celebration unfolded as Lawyer Stephen Asante Bekoe and his son, Paa Kwasi Adom Asante, marked a significant milestone by graduating with Master’s degrees in Law from the esteemed University of Ghana School of Law.

Lawyer Asante Bekoe achieved a remarkable feat by earning his LLM in Natural Resources Law, while his son, Paa Kwasi Adom Asante, excelled in his studies, graduating with an LLM in Energy Law.

Beyond their academic accomplishments, Lawyer Asante Bekoe has a rich history of leadership roles and contributions to various organizations.

He proudly serves as the National President of the Okuapemman Past Students Association and holds the prestigious position of President of the Ghana Canoeing Federation.

In addition to these roles, Lawyer Asante Bekoe is dedicated to the betterment of society, serving as a board member of the Ghana Library Authority and contributing as a member of the Legal and Constitution sub-committee of the Ghana Olympic Committee.

The achievements of both father and son stand as a testament to their commitment to academic excellence and service to the community.

Andre Dede Ayew, the captain of the Black Stars, has formally apologized for the team’s performance at the 2023 African Cup of Nations (AFCON).

In a recorded video message, Ayew expressed regret for the team’s winless campaign that led to their exit in the group stage, including a loss to Cape Verde and draws against Egypt and Mozambique.

“These past days have been very difficult for every Ghanaian football fan and myself. I would like to apologize for the results at the AFCON that we just exited; we know that we should have done better,” Ayew stated, taking full responsibility as the captain.

He acknowledged the disappointment of the fans, emphasizing that setbacks in football make a team stronger. Ayew assured Ghanaians that the Black Stars would rise again and promised to put the nation’s flag back where it belongs.

In response to the criticism and public outcry, the Ghana Football Association (GFA) also issued a public apology.

The GFA acknowledged the frustration and disappointment of Ghanaians and accepted full responsibility for the Black Stars’ performance, expressing sincerest apologies to the nation and all stakeholders.

Get ready for a musical extravaganza as Ghanaian rap sensations Kojo Fyneboy and Danito gear up to showcase their lyrical prowess on the Today’s TV Sunday special show.

Hosted by the charismatic Kojo Pooley, the event is scheduled for Sunday, February 4, 2024.

Initiated by the renowned music promoter Mixtic Romras, this rap battle promises to be a stage where both artists can flaunt their unique styles and lyrical dexterity.

With reputations hanging in the balance, Kojo Fyneboy and Danito are prepared to deliver a performance that will enthrall audiences nationwide.

Excitement is buzzing among fans and music enthusiasts as they eagerly await the clash of these titans. With high stakes and anticipation building, the countdown to the showdown has begun.

His Excellency Boniface Gambila, Ghana’s Ambassador to Burkina Faso, has dismissed assertions implying that Burkina Faso’s exit from the Economic Community of West African States (ECOWAS) would strain the ties between the two neighboring countries.

Ambassador Gambila underscored that despite Burkina Faso’s decision to withdraw from ECOWAS due to dissatisfaction with the regional body’s management of critical issues, the personal and diplomatic connections between the leaders of Ghana and Burkina Faso remain strong.

He expressed confidence that Burkina Faso’s departure from ECOWAS would not result in adverse trade implications for Ghana. Ambassador Gambila cited the enduring closeness between the two presidents and the deep historical bond shared by the nations as factors ensuring the resilience of diplomatic and trade relations.

“Our two presidents are very close, and historically, the fact that we are brothers and sisters, this would not affect us. I am very optimistic. Don’t let any security analyst sit back there and frighten you. There would be nothing of the sort,” Ambassador Gambila affirmed in an interview with Bolgatanga-based A1 Radio.

The withdrawal of Burkina Faso, alongside Mali and Niger, from ECOWAS was motivated by grievances over what they deemed as unfair treatment by the regional organization.

Despite concerns voiced by certain international trade experts about the potential adverse effects of these exits on trade and diplomatic relations, Ambassador Gambila brushed aside such notions. He affirmed the enduring strength of the Ghana-Burkina Faso relationship in the face of regional transformations.

In a significant development, the Nana Addo Dankwa Akufo-Addo government has officially declared its intention to review the flagship Free Senior High School (Free SHS) program.

This revelation comes as part of the information presented in the International Monetary Fund’s (IMF) latest report on Ghana’s US$3 billion bailout programme.

The pertinent details of this policy shift are outlined on page 76 of the comprehensive 155-page report, falling under the section titled ‘PUBLIC SPENDING EFFICIENCY.’

Within this segment, the government articulates its plans, which extend beyond the Free SHS program to include recalibrating the expenditure portfolio of Municipal and District Assemblies (MDAs) responsible for social spending.

This strategic move suggests a broader commitment to enhancing public spending efficiency and highlights the government’s proactive stance in evaluating and adjusting key initiatives for the overall benefit of the nation.

The decision to review the Free SHS program, a cornerstone of the government’s education policy, is likely to spark discussions and debates on the potential implications and desired outcomes.

The relevant portion on education read: “The key objective is to shift the composition of spending by these MDAs towards targeted and well-designed interventions.

“In addition to functional review of relevant MDAs, we will carry out a comprehensive assessment of public sector wages, including in education and health sectors.

Just weeks ago, the government found itself embroiled in a verbal exchange with former President John Dramani Mahama, who pledged to review the Free Senior High School (Free SHS) program if elected in 2025.

Despite the government’s staunch defense, led by the education minister, asserting that the program requires improvements rather than a review, the debate surrounding the Free SHS policy remains contentious.

The Free SHS policy, a cornerstone of the government’s education initiatives, focuses on eliminating financial barriers by absorbing fees approved by the GES council. Its objectives include not only enhancing accessibility by removing cost constraints but also improving educational quality. This is achieved through measures such as providing core textbooks and supplementary readers, implementing teacher rationalization and deployment strategies, and other impactful initiatives.

Furthermore, the policy aspires to address the anticipated surge in enrollment by expanding physical school infrastructure and facilities. As the government and former President Mahama lock horns over the future of the Free SHS program, the debate underscores the significance of this education policy and its potential impact on the nation’s educational landscape.

“In the education sector, we will review and rationalize the Free Senior High School (SHS) program. We will continue our support to tertiary education, take targeted measures to improve foundational learning (e.g., increasing capitation grants) and introduce reforms with the help of development partners to improve overall learning outcomes.”

The December 18, 2023 report was titled: “STAFF REPORT FOR THE 2023 ARTICLE IV CONSULTATION, FIRST REVIEW UNDER THE ARRANGEMENT UNDER THE EXTENDED CREDIT FACILITY, REQUEST FOR MODIFICATION OF PERFORMANCE CRITERIA, AND FINANCING ASSURANCES REVIEW.”

This study investigates how Ghana’s domestic debt crisis in 2022/2023 has affected economic growth. It scrutinizes the constraints imposed by debt overhang, crowding out, and debt reduction effects. The crisis, triggered by pre-existing imbalances and external shocks, led to a full-blown macroeconomic downturn, hindering the post-COVID-19 recovery.

Facing a mounting fiscal deficit and escalating debt levels, Ghana embarked on an aggressive debt restructuring program to achieve a more sustainable debt-to-GDP ratio by 2028. The restructuring efforts target rationalizing development spending, aligning the Producer Purchase Price (PPP) setting process with financial constraints, and enhancing oversight. The study discusses the challenges encountered and the potential economic implications of these restructuring

Examining historical patterns, this section delves into sovereign debt issues and restructuring experiences. It explores the challenges faced by countries during debt restructurings or defaults, emphasizing the impact on the macroeconomy. Stylized facts emerge, highlighting the effects of debt operations on recessions, exchange rates, and recovery. The discussion provides insights into the economic turbulence surrounding debt crises and the subsequent recovery processes.

Drawing from past experiences, this section considers factors influencing a country’s ability to regain access to external financing after a debt restructuring. It explores how the type of restructuring, the cost for creditors, and the economic conditions during and after the restructuring can impact a nation’s access to international debt markets. The study also evaluates the historical context of debt restructurings and their implications for subsequent economic stability and growth.

Overview of Ghanaian economy in the Pre-DDEP period

By the end of the 3rd Quarter of 2021, Ghana’s fiscal vulnerability had been evident to the market resulting in a loss of market access largely consistent with the country’s struggle to manage its public debt since independence.

In all of Ghana’s program engagements with the International Monetary Fund (IMF) debt unsustainability has been recurring reflecting a weak fiscal regime of expenditure rigidities and low domestic revenue mobilization.

The latest IMF Supported Program is unique given the number of prior actions the country had to undertake to qualify for help from the IMF including taking a comprehensive approach to restructuring the country’s public debt with the domestic debt restructuring being a condition precedent to getting IMF Board approval.

Unlike the case of Zambia, which excluded the domestic debt from its debt restructuring to protect the domestic financial system, Ghana applied the most aggressive debt restructuring which was first announced on December 5th, 2022. Arguably the first of its kind in the history of the country.

Government instruments (excluding only treasury bills) held across households (including pensioners), financial institutions, body corporates, and resident and non-resident investors were considered to be in the universe of eligible bonds.

The country’s economic fundamentals had deteriorated to the extent that the traditional fiscal consolidation measures embodying expenditure restraint and revenue enhancement measures were considered to be inadequate and therefore restructuring had become fundamental to restoring fiscal sustainability.

The Ghanaian economy has witnessed poor revenue growth, and low export earnings from cocoa, gold, and oil because of over-dependence on international capital markets and low tax capacity over the past decade. The country’s debt stock as a result has increased considerably over the past decades – a trend generally connected with expansion in the size of government expenditures.

Ghana’s economy entered a full-blown macroeconomic crisis in 2022 on the back of pre-existing imbalances and external shocks. Large financing needs and tightening financing conditions exacerbated debt sustainability concerns, shutting off Ghana from the international market.

Large capital outflows combined with monetary policy tightening in advanced economies put significant pressure on the exchange rate, together with monetary financing of the budget deficit, resulting in high inflation. These developments interrupted the post-COVID-19 recovery of the economy as GDP growth declined from 5.1% in 2021 to 3.1% in 2022. World Bank (2022) found that the fiscal deficit widened slightly to 15.2% of GDP in 2020 but further improved to 12.1% of GDP in 2022 due to higher spending.

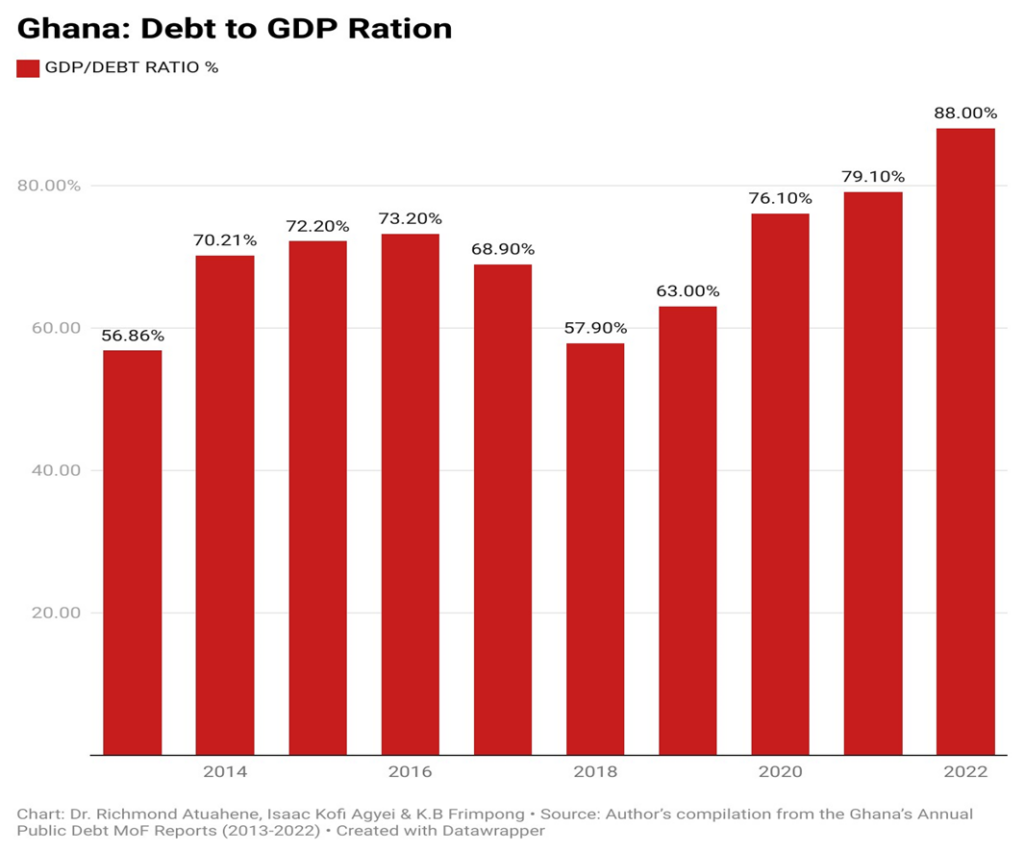

Public debt declined from 79.6% in 2021 to over 88.1% of GDP in 2022, as debt service-to-revenue reached 117.6%. The country’s debt overhang sets in when the face value of debt reaches 60 percent of GDP or 200 percent of exports, or when the present value of debt reaches 40 percent of GDP or 140 percent of exports.

The monetization of fiscal deficits., and Bank of Ghana lending to government through ways and means advances have risen to GHS 50 billion in 2022, exceeding the threshold set by Bank of Ghana Act 2002 Act 612 as amended Act 2016 Act 918 Section (2) the total loans, advances, purchases of treasury bills shall not at any time exceeds 5% of the total revenue of the previous fiscal year.

These ways and means advances are temporary overdraft facilities provided to the Government of Ghana (GoG) to help with financial difficulties caused by a cash flow mismatch by bridging the gap between expenditure and revenue receipts.

This level of borrowing from the Bank of Ghana to finance fiscal deficit was unsustainable, fueled inflation, and endangered growth. In Ghana, deficit financing has led to borrowings from multinational finance institutions, such as the International Monetary Fund (IMF), the World Bank, the African Development Bank (ADB), and Euro-markets amongst others.

Unfortunately, the rising national debt in Ghana began to outweigh the country’s revenue generation capacity and draw down on foreign reserves, hence stifling the much-needed public capital investments and economic productivity.

Also, it has been reported that these borrowed funds are often mismanaged and misapplied, hence, were not used for economically productive activities, leading to debt burden, capital flight, and economic instability in the long run.

Ghana has accumulated huge debt with the rising cost of debt service which has undermined economic stability as domestic investments are being crowded out by the rising cost of debt servicing. Komlan and Essosinam (2022) opined that nations like Ghana that adopt unsustainable fiscal policies have an ever-increasing debt-to-GDP ratio that violates their budgetary restraint.

High debt levels resulted in high debt servicing, which has led to a low amount of money available for investment in infrastructure and other economic sectors.

Ghana’s debt profile continued to increase in the face of expanding fiscal deficit and low revenue-generating capacity. This was concerning because the country’s debt profile became more and more dominated by commercial debt.

Weak fiscal and economic performance over extended periods led to an unsustainable fiscal situation for Ghana in 2022 which led to the domestic debt restructuring. The debt exchange perception has increased the risk of Ghana government securities as expected to significantly blunt confidence in the Ghanaian economy in general, thereby affecting the creditworthiness of private institutions as well as individuals.

This has translated into a further cut in letters of credit lines to domestic banking institutions, which have had grave implications for external trade and the stability of the local currency (Cedi). The Ghana Domestic Debt Exchange (DDEP) was launched on 5th December 2022.

It was designed to offer relief to fiscal accounts through a sizable reduction of the coupon rates as well as through the extension of maturities on most domestically issued bonds.

While par-neutral, the exchange aimed to provide a solid foundation for reducing Ghana’s debt to sustainable levels in the medium term via offering an effective cap on interest payments on public debt and stronger growth prospects. Without effective debt restructuring, reduction, or forgiveness, middle-income debtor nations risk falling into a debt trap with debt overhang where economic policies focus solely on servicing unproductive debt repayments to creditors and propping up an unfair global financial system.

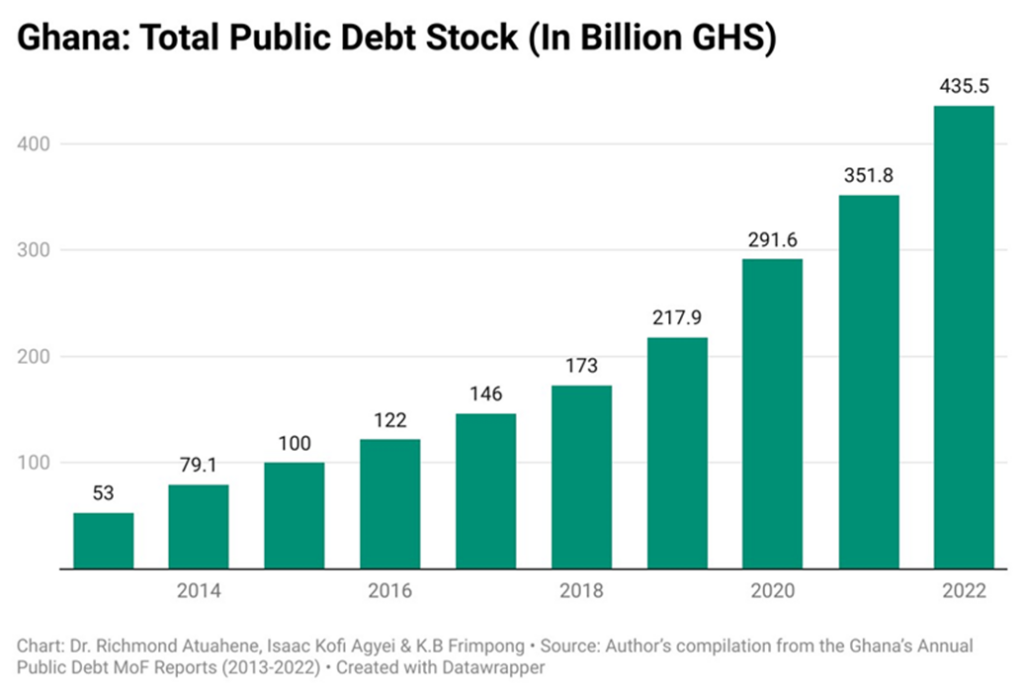

AN OVERVIEW OF GHANA’S PUBLIC DEBT SITUATION OVER THE PAST DECADE

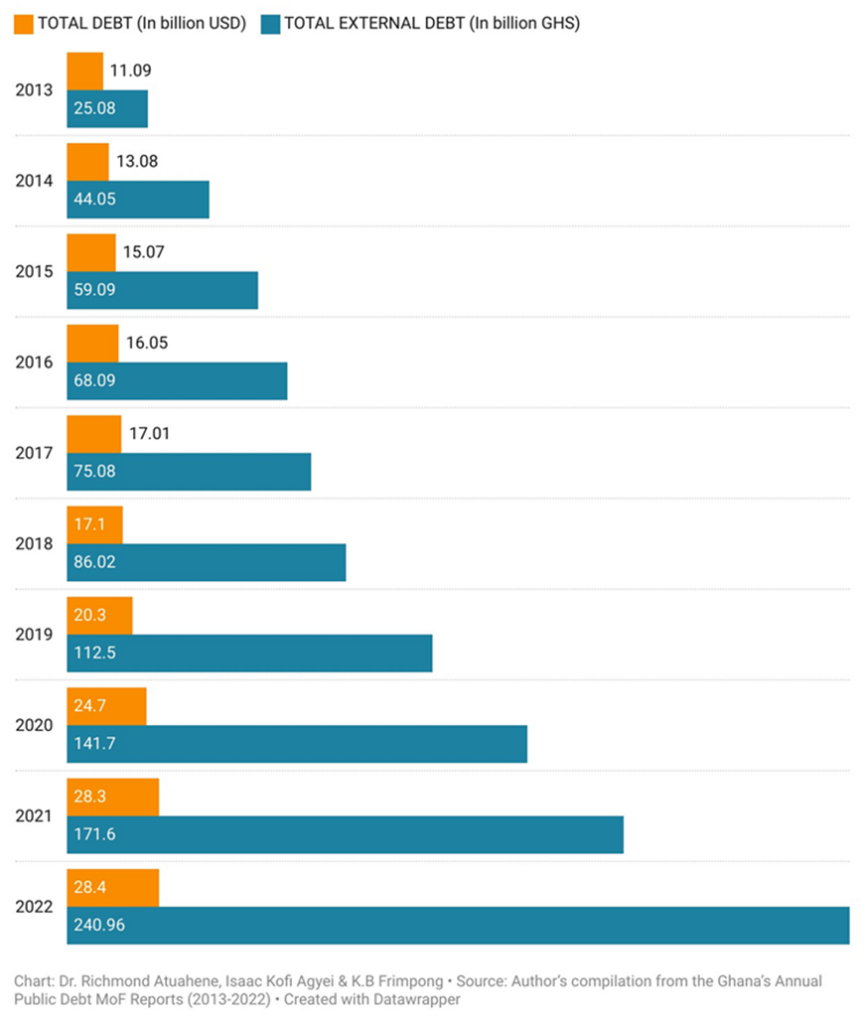

According the Ministry of Finance posited that Ghana’s total public debt in 2012 was GHC 35.9 billion (US $19.2 billion) thus represented 47.8% of GDP after rebasing in 2010 but increased significantly to GHC 53.1 billion (US$24.4 billion) or 56.8% of GDP in 2013.

In 2014, Ghana’s public debt rose to GHC 79.5 billion (US$ 24.7billion) or 70.2% of GDP and further increased significantly to GHC 100.2 billion (US$ 26.4 billion) in 2015 thus representing 72.2% of GDP.

By the end of December 2016, the public debt stock stood at GHC 122.2 billion (US$ 29.3 billion) thus representing a debt/ GDP ratio of 72.5%. Ghana’s public debt stock stood at GHC 146.6 billion (US$ 32.3 billion) at the end of 2017, up from the 2016 figure of GHC 122.3 billion (US$ 29.3 billion).

The total public debt as a percentage of GDP declined from 73.2% in 2016 to 69.8 % of GDP in 2017. Ghana’s public debt stock as of the end of December 2018 was GHC 173.1 billion (US$ 35.9 billion) representing 57.9% of the rebased GDP.

According to the Ministry of Finance and Economic Planning Annual Debt Review (03/2019), a large part of the 2018 public debt stock additions of GHC 11.1 billion resulted from the banking sector bail-out program of the government.

The cost incurred by the government to clean up the banking sector impairments resulted in the public debt increasing by 3.2% of the rebased GDP. Excluding the bail-out costs, however, the stock of public debt amounted to GHC 163.4 billion (US$ 33.9 billion) thus representing 57.9% of rebased GDP as of the end of December 2018.

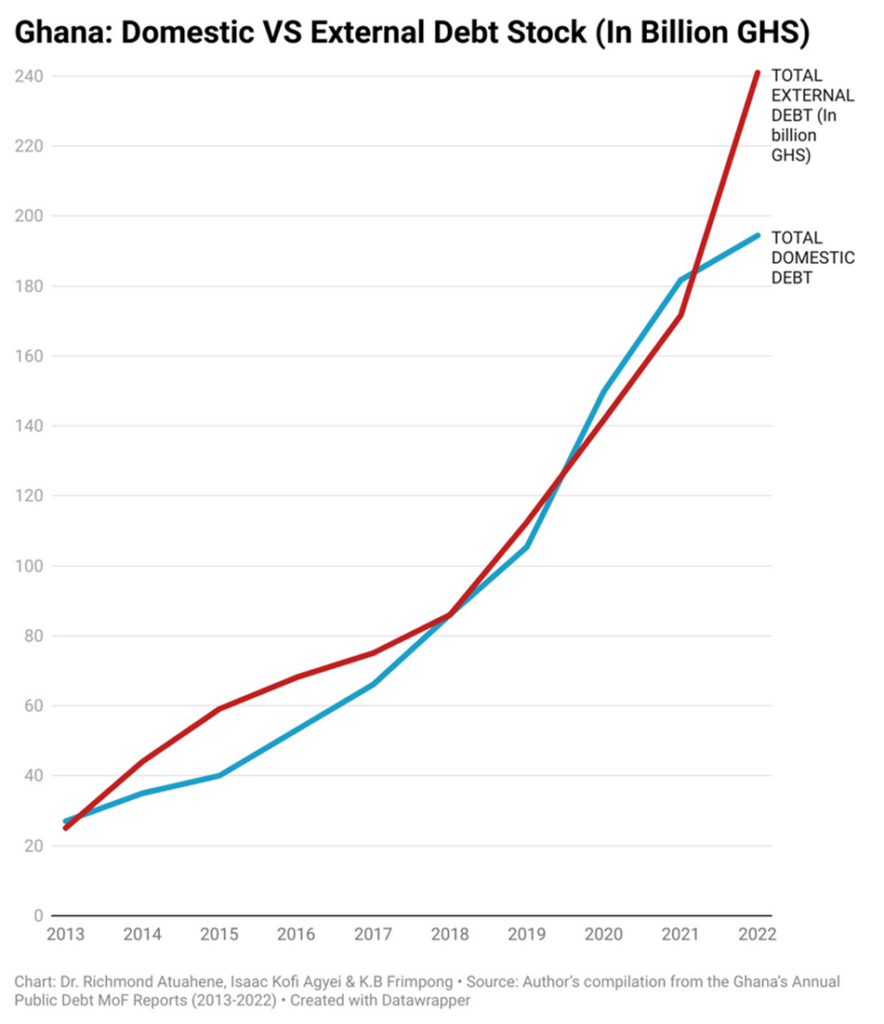

At the end of December 2018, the stock of external debt was GHC 86.2 billion (US 17.9 billion) representing 28.9% of GDP while the domestic debt stood at GHC 86.78 billion which represented 28.9% of GDP. By the end of June 2019, the stock of public debt rose to 59.2% of GDP (GHC 204 billion compared with December 2018 representing 57.9% of rebased GDP.

Thereafter, domestic debt increased very sharply, reaching GH₵86.2 billion in 2018 and then to GH₵94.8 billion at the end of May 2019. This indicates that domestic debt increased by GH₵4.1 billion between 2000 and 2008, GH₵13.6 billion between 2008 and the end of 2018 later increased to GHC 94.8 billion at the end of May 2019.

Total domestic debt stood at GH₵86.889.3 billion at the end of December 2018, indicating an increase of GH₵6.0 billion by the end of March 2019. Ghana’s debt stock as of the end of December 2018 stood at GHC173,068.7 billion (US$ 35,858 billion) comprising external and domestic debt of GHC 86,169 billion (US$ 17.868 billion) and GHC 86.9 billion (US$18.020 billion) respectively.

This represented 57.9% of the debt/GDP ratio. External and domestic debt accounted for approximately 49.7% and 50.3% respectively. The Cedi recorded a cumulative depreciation of 8.4% against US$ as of the end of December 2018 and this impacted negatively on external debt.

The total public debt stock has increased from GHC 173 billion at the end of December 2018 to GHC 198 billion at the end of March 2019 further increasing to GHC 204 billion at the end of June 2019. The external debt stock increased from GHC 86.2 billion as of December 2018 to GHC 115 billion at the end of June 2019.

Similarly, the domestic debt component has also increased from GHC 86.9 billion at the end of December 2018 to GHC 99.8 billion at the end of March 2019 but declined to GHC 94.6 billion. Ghana’s total public debt rose to 54.8% of the GDP (GHC 198.0 billion) at the end of March 2019 compared with 57.9% of the GDP at the end of December 2018 but increased further to GHC 204 billion or 59.2% of GDP in June 2019. Of the total public debt stock of GHC 198 billion, GHC 11.0 billion or (3.2% of GDP) represented bonds issued to support the banking sector cleanup.

As a percentage of the GDP, the external debt has declined marginally from 29.6% in 2018 to 26.3 % at the end of March 2019, while domestic debt increased from 29.3% in December 2018 to 31.2% at the end of March 2019. The stock of public debt rose to 59.2% of GDP (GHC 204 billion) at the end of June 2019 Of the total debt stock, domestic debt was GHC 94.6 billion (27.5% of GDP) while external debt was GHC 105. 4 billion (30.6 % of GDP) and the end of June 2019.

The accumulation of public debt has been a direct result of the gap between unplanned expenditures and revenues, which has widened due to the inelasticity of debt servicing and infrastructural needs, deteriorating terms of trade, and the failure to improve and enhance revenue collection over the long period. Ghana’s public debt stock stood at GHC 173.1 billion (US$35.9 billion) at the end of December 2018.

This was made up of GHC 86.2 billion or (US$ 17.9 billion) of external debt and GHC 86.9 billion or (US$ 18 billion) of domestic debt Also, persistent currency depreciation over the period contributed to the stock of Ghana’s public debt of GHC 204 billion (US$ 38.7 billion) at the end of June 2019.

According the Ministry of Finance and Economic Planning (29/07/ 2019) opined that the total public debt has increased from GHC200 billion (58.1% of GDP) at the end of May 2019 increased further to GHC 204 billion (US$ 38.7 billion) at the end of June 2019 representing 59.2% of GDP nearing the high distress threshold of 60% set by the IMF/World Bank.

The share of the external debt stock increased from 50.2% at the end of December 2018 to 52.8% at the end of June 2019 mainly driven by the issuance of Eurobonds of US$ 3 billion in March 2019. The IMF also disbursed an amount of SDR132.84 million (US$184.30 million) in March 2019 after their 7TH and 8th reviews of the Extended Credit Facility Program. On account of these two major inflows, a net amount of US$ 2.9 billion, equivalent to approximately GHC14.8 billion was added to the debt stock.

The increase in the external debt stock amounted to GHC 23.8 billion between December 2018 and June 2019 reflecting a volume transaction of GHC 14.8 billion and exchange rate depreciation of GHC 9 billion (MOF, Mid-year Fiscal Policy 29/07/2019).

Ghana’s public debt stock increased from GH¢218.2 billion (US$39.4 billion) in 2019, representing 62.4 percent of GDP, to GH¢291.6 billion (US$50.8 billion) in 2020, representing 76.1 percent of GDP. The increase resulted mainly from increased fiscal deficit and primary balance deficit, exchange rate depreciation, disbursement of existing loans, and contracting of new loans.

Ghana’s public debt as of end-December 2021 was GH¢351.7 billion (US$58.6 billion), comprising external debt of GH¢170.billion (US$28.3 billion) and domestic debt of GH¢181.8 billion (US$30.3 billion), respectively.

The domestic debt stock compared to the external witnessed a relatively higher nominal increase, attributable to net issuances of domestic instruments to pay down the cost incurred from the crystallization of contingent liabilities in the energy sector and the financial sector bailout, while the external debt rose mainly on account of disbursements due on new and existing loans, the Eurobond issuance in March 2021, and fluctuations in the exchange rate over the period under review.

In 2022 due to high inflation, interest rates, and portfolio reversals, issuances of Government securities remained under pressure, highlighted by weak demand, and various undersubscriptions during the year. The provisional stock of public debt increased from GH¢351billion (US$58.6 billion) in 2021 to GH¢435.3 billion (US$52.3 billion) at the end of December 2022, representing an increase of 23.7 percent.

The depreciation of the cedi alone accounted for GH¢67.1 billion (equivalent to 88.1%) of the increase in the debt stock at the end of December 2022 (Ministry of Finance, 2013-2022). billion), respectively.

The domestic debt stock compared to the external witnessed a relatively higher nominal increase, attributable to net issuances of domestic instruments to pay down the cost incurred from the crystallization of contingent liabilities in the energy sector and the financial sector bailout, while the external debt rose mainly on account of disbursements due on new and existing loans, the Eurobond issuance in March 2021, and fluctuations in the exchange rate over the period under review.

In 2022 due to high inflation, interest rates, and portfolio reversals, issuances of Government securities remained under pressure, highlighted by weak demand, and various undersubscriptions during the year. The provisional stock of public debt increased from GH¢351billion (US$58.6 billion) in 2021 to GH¢435.3 billion (US$52.3 billion) at the end of December 2022, representing an increase of 23.7 percent.

The depreciation of the cedi alone accounted for GH¢67.1 billion (equivalent to 88. %) of the increase in the debt stock at the end of December 2022 (Ministry of Finance, 2013-2022.). The increase in the debt-to-GDP ratio of 88% led to the realization that Ghana’s debt was not sustainable.

The sharp deterioration in terms of trade, higher interest rate changes on non-concessional loans, huge currency depreciation, and higher fiscal deficits are often mentioned as some of the major causes of the rapid growth of the domestic debt crisis in Ghana over the past decade. Debt has already placed a significant burden on Ghana’s economy and society, and the country has fallen back into a debt trap, with economic stagnation possible increases in poverty rates, and failure to implement the Sustainable Development Goals.

First, one of the major factors that has contributed to Ghana’s domestic debt crisis was the unproductive use of borrowed funds. Funds have not been used judiciously. Ghana with huge infrastructural deficits, borrowed funds to supplement its small domestic revenue but invested in unproductive and uneconomic viable ventures. The huge borrowing was expected to generate higher returns on capital compared to that of some emerging economies.

However, borrowed funds have not been invested in productive and commercially viable ventures capable of generating enough economic returns that could have been used to service the debt and eventually pay back the debt. Using part of Eurobond proceeds in financing a major project like Cocoa farm roads, the government should principally look to the cash flows and earnings of the Cocoa sales as the source of funds for repayment for principal and interest payment but if borrowed funds are used in funding social project like funding the Free SHS then the repayment created debt crises. Furthermore, such projects should pass a sensitivity analysis test that quantifies the effect on the project (and in the case of a project loan, the effect specifically on cash flow available for debt service and loan repayment.

In preparation for the international capital market, the first task of the government was to identify a portfolio of projects that are viable for commercial funding with enough economic rate of service return the underlying debt. Projects selected for funding were not commercially viable in their own right but sometimes for political expediency and also project yields did not have a high economic rate of service return to the underlying debt. The decision on how to use borrowed funds is important to ensuring debt sustainability.

At all costs, funds raised by issuing debt should be invested in projects that have a high private or social return. When borrowing in foreign currencies, the country should take great care to ensure that future export revenues will be sufficient to service the additional debt. Debt accumulation is unlikely to be sustainable if domestic or foreign borrowing is used to finance public or private consumption with no effect on long-term growth.

Most of the selected projects were desirable but did not meet the criteria for access to commercial funding. However, the first debut sovereign bond in 2008 met the project criteria for sourcing external funding as it was not properly appraised and evaluated. Eurobond proceeds must be used judiciously to support projects that generate more future export revenues to service the debt. Furthermore, sovereign bond or Eurobond proceeds should not be thinly spread as done recently.

Eurobond proceeds of US$ 1 billion were thinly shared among the Ministry of Energy and Petroleum, Ministry of Food and Agriculture, Ministry of Roads and Highways, Ministry of Railways Development, Ministry of Water Resources, Works and Housing, Ministry of Education Ministry of Health. Some of the detailed allocations under the Eurobonds looked very frivolous and flimsy, for example, the allocation of GHC50 million for the construction of greenhouses and capacity building training centers while not supporting the growth of oil palm and cashew sectors and also spent a whooping GHC45 million for supplying and installation of integrated e-learning laboratories for senior high schools in Ghana while we still have some primary schools in our villages and cottages operating under trees and dilapidated structures ( Report of the Finance Committee, Parliament of Ghana, 03/2018).

The government should have sought concessional funding for projects like coastal protection green housing projects and capacity building instead of funding these projects with expensive commercial debt. The decision on how to use borrowed funds is important to ensuring debt sustainability. At all costs, funds raised by issuing debt should be invested in projects that have a high private or social return. Debt accumulation is unlikely to be sustainable if loans are used to finance public or private consumption, with no effect on long-term growth. The fact is that development cannot be justified by high and unsustainable public debt.

The country’s debt can only be reined in through sustained fiscal prudence to help reduce borrowing. It is important therefore that loans contracted are used to develop the economy to enable it to ‘grow out of debt.’ It would be a fatal mistake to use loans to fund recurrent spending or refinance debts that were used to fund recurrent spending that did not have a direct bearing on growth. But there are conditions under which even debt used to finance productive investment could turn out to be unsustainable.

This happens if the ex-post returns on a project end up being lower than the interest and principal debt repayments and should therefore be guided against very carefully. Borrowing from the local bond market at 19.1% to finance social projects at 0% returns has caused domestic debt crises over the past six years.

Second, another factor that has contributed to the country’s debt crisis has been the continuous high fiscal deficits driven by unproductive public spending influenced by vague political promises made during political campaigns.

According to Bawumia (2010), the global food and fuel price increases in 2007-2008 adversely impacted most Sub-Saharan African countries, including Ghana. In the context of these global shocks and the 2008 elections, public sector spending increased substantially, raising the fiscal deficit from 7.6% of GDP in 2006 to 14.5% of GDP in 2008 to further record high of 15.2% of GDP in 2020. Contributing to the strong fiscal expansion were high energy-related subsidies, increased infrastructure investment, higher wages and salaries, and a rise in social mitigation expenditures to dampen the effects of the global price shocks.

Over the past decade the government primary deficits have been arising thus increasing the burden of debt because the governments had little resources to service interest on public debt. Fiscal deficits had worsened not only because of the plunged in export revenues but also because of the need to increase social spending and safety nets over the period.

In Ghana, the lack of fiscal discipline is identified as a cause of the ballooned public debt up. For example, Ghana has been accumulating relatively large primary fiscal deficits over the past two decades, amplified every time the country was approaching elections. According to various IMF Country reports recorded high budget deficit over the past decade, for example in 2007 was 7.8% of GDP, 14.5% of GDP in2008; 10.9% of GDP in 2011; 10.2% of GDP in 2012; 10.3% of GDP in 2013; 12% of GDP in 2014. 9.5% of GDP in 2015; 9.3 % of GDP in 2016; 6.3% of 2017; 7% of GDP in 2019; 15.2% in 2020 9.4% in 2021; 12.4%in 2022.

In 2020, Ghana was hit hard by the Covid 19 pandemic which accelerated fiscal deficit of 15.2% of the GDP that included energy and financial sector costs with a further 2.1% of GDP in additional spending financed through the accumulation of domestic arrears (IMF, 21/221). Ghana’s continuous high fiscal deficit was driven by partly by unproductive public spending that was not efficient in supporting equitable development. However, around the 2008, 2012, 2016 and 2020 elections, fiscal slippages and unduly spending led to deep holes in the budget and unfavorable debt issuances.

For example, the fiscal slippage in 2008 was the result of government subsidies of utilities, election year wage and salary increase and increased capital investment from proceeds of Ghana’s sovereign bonds to deal with energy crisis (Bawumia, 2010). At root of Ghana’s fiscal deficits was out of control government spending, largely to pay salaries of an overgrown civil service (Adams,2015). Fiscal slippages were due to bad public finance management in Ghana.

As a result of this weak fiscal discipline, decline in commodity prices and high investment needs, the Ghanaian public finances have been under serious pressure over the years. A major factor that has contributed to the debt problem is the levels of fiscal deficits over the past decade, borrowing to finance the deficits and the terms of borrowing. Among all these factors the most important is probably the fiscal deficit as it drives the level of borrowing and even the terms that can be obtained for such borrowing.

Ghana opted for major development programs and highly expansionary fiscal policies during the oil findings in the late 2000s, acquiring external debt as spending increases outpaced the rise in tax receipts. These spending policies continued for some time after the post- collapse in commodity prices (cocoa, gold and oil). Ghana also used external borrowing to maintain consumption in the face of falling export earnings.

The growing fiscal deficits also reduced the ability of governments to make debt-service payments as they led to declines in the growth of real national income, inflationary pressures, and depreciation of Cedi against major trading currencies. Private savings, which could have been an alternative to foreign borrowing, were also discouraged by policies designed to keep domestic interest rates low. This resulted frequently in negative real interest rates and disintermediation in the financial sector.

Third, the rising Ghana’s debt has limited the economy and has hampered tax collection system which accounted for only 13%. tax to country’s GDP ratio which the lowest among our peers in the sub-region.Total tax revenue collections in 2019 totalled GH¢45.6 billion, implying a tax-to-GDP ratio of 13% (IFS, 2021). The tax-to-GDP ratio in Ghana increased by 1.0 percentage points from 13% in 2020 to 14.1% in 2021 (IFS,2022) low than Africa’s average tax-to-GDP rate of 16.5%.

Tax evasion, tax avoidance and tax exemptions are some reasons that have accounted for low tax to GDP ratioin Ghana. The defining feature of tax systems across in Ghana is their inability to collect a significant share of revenue through income taxation of individuals and corporations. Ghana’s overwhelmingly collect far less direct tax than developed countries, both as a share of total taxation and as a share of GDP. Also, the higher debt affected the revenue mobilisation in several important ways.

Revenue mobilisation was directly affected by debt constraining the economic environment in a way that led to low economic growth. Low economic growth meant less tax to collect. These were some of the channels that debt affected tax collection in the country. Domestic government debt crowds out the private sector by limiting the funds available to borrow. This has constrained the private sector’s ability to grow the economy, create jobs, and generate revenues that could be taxed. Debt also increased the risk of fiscal crises by creating an unstable macroeconomic environment.

External debt repayments put pressure on the exchange rate contributed to it deteriorating and made imports more expensive thereby contribute to higher inflation in 2022. This, in turn, has contributed to lower growth. Further, debt has created a crowding-out effect, where the government’s high interest payments and repayments consume a significant portion of the government’s revenue, leaving less room for the country’s self-financed public investment. This has created a greater incentive to borrow to finance public investment and thus, beginning the cycle again.

Fourth, one key factor that has contributed current debt crisis in Ghana has been the endemic corruption prevailing the public sector, as huge fiscal revenue continues to be lost, impeding the ability of government to invest in public social spending using domestic revenue. The 2022 Auditor General’s report shows that irregularities in the public sector in 2021 amounted to about GH¢17.5 billion. Similarly, the Auditor General’s COVID-19 expenditure report shows that US$81 million worth of vaccines paid for by the state were never delivered, among other infractions.

Over the years there has been a growing interest on the relationship between public debt and corruption globally. Voluminous studies have looked at this relationship and out of these studies the main finding has been that corruption increases public debt and also that a larger shadow economy reduces tax revenues and thus increases public debt, similarly, higher government expenditure enhances the effects of corruption on government debt. Transparency International defines corruption as abuse of entrusted power for private gain.

The World Bank defines corruption as the abuse of public office for private gain. Corruption and unsustainable public debt are twin governance challenges confronting Ghana’s public finance management system. Corruption in Ghana has resulted in a marked increase in levels of fiscal deficit and domestic indebtedness as central government has bailed out and taken over the debts of several parastatals. Corruption has increased public debt, and a larger shadow economy has reduced tax revenues and thus increased public debt. Similarly, higher government expenditure enhances the effects of corruption on government debt.

In Ghana corruption and unsustainable public debt are twin governance challenges confronting the public finance management system. Corruption often leads to adverse influences on the economy. It is one of the main constraints facing companies in developing economies (World Bank, 2021). Gupta et al. (2002) highlights that corruption increases income and wealth inequality and poverty in several developing countries like Ghana.

In particular, it enhances the transaction costs of private investors, which leads to a decline in profit and investment. Widespread corruption tarnishes a country’s international reputation and reduces its attractiveness for foreign investment, public debt, tourism, and development assistance. It undermines Ghana’s standing in global indices that measure corruption levels, such as the Corruption Perceptions Index, and can hinder international cooperation and partnerships. Corruption hampers economic growth and development.

It distorts market mechanisms, undermines fair competition, and diverts resources away from productive sectors. It creates barriers to investment, reduces investor confidence, and deters both domestic and foreign direct investment. Corruption also leads to inefficient allocation of resources, loss of public funds, reduced government revenue and increased domestic debt. The effect of corruption on public debt is increased by government expenditure, the shadow economy and military expenditure and they found out that the effect of corruption on public debt is compounded by increased government expenditure and increased size of the shadow economy.

In another related study by Cooray, Dzhumashev and Schneider (2017) confirmed that increased corruption and a larger shadow economy leads to an increase in public debt. More so they did find that a larger shadow economy reduces tax revenues and thus increases public debt, similarly, higher government expenditure enhances the effects of corruption on government debt. Theoretical literature shows that there is link between corruption and government debt through a regime-based approach and they found that public debt appears to respond faster to a high corruption regime compared to a low corruption regime.

The fifth factor that has brought about the Ghanaian debt crisis was the many years of unfavorable terms of trade. The widening external debt to current account receipts ratio has been a major feature over the past decade. Strong public spending growth combined with rapid credit expansion and rising oil import costs contributed to a widening of the external current account deficit from 9.9% of GDP in 2006 to 19.3% of GDP in 2008.

While Ghana’s external indebtedness has increased in recent years, the current account receipts have decreased since 2011. According to IMF Country reports (2011-2022) the current account recorded negative ratios of GDP (-9.3% in 2011; -11.7% in 2012; -11.9% in 2013; -9.6% in 2014; -8.3% in 2015; -7.2% in 2016 and -5.5% in 2017; -3.1% of GDP in 2018; -2.78 in 2019; -3.2%; in 2020; -2.8% in 2021 and -2.1% in 2022). The decline in the export receipts contributed significantly to debt crisis of the 2000s. The significant drop in export receipt from cocoa, gold and oil, combined with a strong US$ (i.e. the value of the dollar increased relative to the value of other currencies) and high global interest rates, depleted foreign exchange reserves that Ghana relied upon for international financial transactions. Ghana consequently began to feel the strain of having to borrow to refinance the maturing 2008 Eurobond of US$ 750 million in 2019. The interest payment of the huge foreign debt has recently compounded depreciation of the cedi against the major trading currencies and massive capital flight. The persistent current account deficits not only depleted gross official foreign reserves but also involved an accumulation of external debts.

The terms of trade have shifted against Ghana over past decades. Revenues from commodity taxation did not rise as fast, and previous governments used foreign borrowings to meet the cost of projects. When commodity prices declined, expenditures were not reduced commensurately, but governments resorted to additional borrowing to maintain expenditure levels.

This policy would have been appropriate had the decline in the terms of trade been temporary but the deterioration of the terms of trade had persisted through the 2000s. As the country still dominantly consists of a commodity-based economy, the drop-in receipts from cocoa, gold and oil has been mainly due to decline in commodity prices. Oil discovery and volatility in commodity prices have been another cause of the Ghana’s debt problem.

According to some analysts, Ghana’s post HIPC/MDRI debt crisis is a result of the gradual increase in borrowing off the back of the discovery of oil and volatility in world commodity prices. In early 2013, the price of gold fell significantly, as did the price of oil from the start of 2014. More money was therefore borrowed following the fall in the price of oil and other commodities to deal with the impact of the commodity price crash while the relative size of the debt also grew because of the fall in the value of the cedi against the dollar. At the same time, the rapid economic growth in the 2010-2016 periods, driven by the coming on stream of oil production in the country has led to an increased willingness and desire of various institutions to lend to the country, with a corresponding willingness to borrow (Jones, 2016).

Secondly, on the revenue side, the Ghana has been seriously affected by the decline or collapse of commodity prices on the international market over the past decade. Ghana as a major exporter of cocoa, gold and oil have experienced significant decrease in fiscal revenues, yet the lion’s share of export receipts did not build up sufficient buffers during the boom period to deal with shocks.

A continued and sustained decline in commodity prices jeopardized the debt sustainability position of this commodity dependent nation since drop-in commodity prices reduce export earnings and therefore increase the debt service to export earnings ratio. Consequently, the country’s debt increased astronomically during the last decade. A combination of commodities price fall and loans not being used judiciously enough to ensure that they could be repaid also contributed to pushing the country back into debt crisis.

Sixth, one major factor that has contributed to the current domestic debt crisis has been the energy sector debt since 2014. Ghana’s energy sector debt has been a major contributor to her current domestic debt crisis. According to IMF country report (23/168) found that shortfalls in the energy sector have been significant due to below-cost-recovery tariffs, large distribution losses, and excess capacity amid take-or-pay contracts have all contributed to the debt crisis.

The deficiencies in the sector characterized by the tariff systems and management issues coupled with expensive power purchases by the state in addition to the transmission losses, poor revenue mobilization, wastage and losses in power distribution were the major problems in the energy sector driving Ghana’s into her current debt crisis.

The mismatch between the production cost of the Independent Power Producers (IPPs) vis-à-vis how much consumers paid led to an upsurge of debts since the Government could not make financial commitments to them (IPPs). The Power Purchasing Agreements (PPAs) signed were expensive (World Bank, Laporte, 2023). In addition to the exorbitant power purchases the country was paying for energy it does not use due to the ‘’take or pay contracts.

According to the Fitch Ranks, the energy sector is the biggest driver of the national debt as the West African Country currently owes independent power producers to the tune of $1.58 billion. The economy is on the verge of collapse and a legacy of take or pay contracts saddled our economy with annual excess capacity charges of close to $1 billion. These were basically contracts to supply energy to Ghana way more than our requirements, but we were obligated to pay for the power whether we use it or not. Excess electricity take-or-pay charges.

ECG (and the central government) are counterparties to several take-or-pay contracts with independent power producers. The contracts require payment for contracted volumes of electricity even if the electricity is not consumed (take-or- pay charges). When ECG expenses the charge, its equity is reduced, and its liabilities (accounts payable) increase.

The reduction in equity lowers the value of the government’s investment in ECG. The actual payment of the claim by ECG or the government does not alter the public sector’s net worth. The debt overhang has forced the government at times to borrow from international capital to settle part of the legacy debt. Government has been trying to renegotiate and restructure the Power Purchase Agreements (PPAs) with six (6) operational Independent Power Producers (IPPs), namely, Karpower, Cenpower, Early Power, Twin City Energy (formerly Amandi), AKSA Energy, and CENIT Energy but it has achieved little success to ensure that power is affordable and available for industrial, commercial, and residential use.

The government has been trying to renegotiate commercial agreements with each of the IPPs to convert power plants to tolling structures, and switch to the use of natural gas to power the plants and to ensure achieve sustainable power. The Ministries of Energy and Finance must collaborate with the World Bank to work closely to reduce future legacy debt which has been albatross on the country’s meagre finances.

To make total savings of millions of dollars are expected when all agreements are finalized and executed. To avoid the debt overhang in the energy sector, the government must renegotiate with N-Gas to reduce the take-or-pay and other financial obligations on the gas supply agreement with VRA were concluded and this is expected to lessen the take-or-pay burden on the Government. The energy debt has become debt overhang.

To reduce the debt overhang, the government must agree with the IPPs to restructure the huge indebtedness owed by the government.

Seventh, one most important single contributor to the current domestic debt crisis has been the financial sector clean up to the tune of almost of GHS 26.05 billion in 2017-2019. In line with the above, the Bank of Ghana (BoG) as the resolution authority for banks and specialized deposit-taking institutions (SDIs) revoked between 2017 and 2019 the licenses of four hundred and twenty (420) financial institutions in an exercise dubbed the Banking Sector Cleanup.

Among the 420 institutions were nine (9) Banks, twenty-three (23) Savings and Loans /Finance Houses Companies, three-hundred and forty-seven (347) Microfinance Companies, thirty-nine (39) Microcredit Companies, one (1) Remittance Company, and One (1) Leasing Company.

The total assets taken over for the 420 defunct institutions amounted to GHȻ26.05 billion (7.45% percent of GDP). The Government of Ghana spent GHȻ18.99 billion (5.49% of GDP) to fund the repayment of the deposits of affected depositors’ including the establishment of a bridge bank (Consolidated Bank Ghana Limited). The Banking Sector Clean-up was aimed at ensuring orderly exit of insolvent institutions to protect depositors’ funds and also ensure the safety and soundness of the banking sector which was in a state of distress (GH-MOF FSD-315018-CS-INDV, 2022).

Lastly, another contributing factor to the current domestic debt crisis has been the government flagship programs over the past six years. The government flagship programs have enjoyed budgetary allocation worth GH¢33 billion in a span of three years (2020-2023) and added to the country’s domestic debt crisis. According to IMF Country report on Ghana (23/168) Ghana spent close to 4 percent of GDP on education with good results in terms of enrollment but poor learning outcomes.

The flagship program Free Senior High School (SHS), which covers the full cost of secondary education, has helped increase enrollment but is poorly targeted. Key identified areas of potential improvement of education spending include strengthening primary education resources, better teacher training, and stronger performance-based funding practices.

The flagship programs captured in the report include Free SHS, Planting for Food and Jobs (PFJ), One-district, One-factory (1D1F), Infrastructure for Poverty Eradication Program (IPEP), Ghana School Feeding Program, Railways Development, Agenda 111 and Coastal Fish Landing Sites. For education, it said Ghana spends close to 4% of GDP on education with good results in terms of enrollment but poor learning outcomes. It pointed out that the flagship program Free Senior High School (FSHS), which covers the full cost of secondary education, has helped increase enrollment but is poorly targeted.

The challenges associated with the implementation of the policy were financial constraints, infrastructure deficit, inadequate and delayed release of food items, lack of teaching and learning materials, inadequate contact hours, and poor implementation of the policy and the double-track system. The challenges associated with the implementation of the policy were financial constraints, infrastructure deficit, inadequate and delayed release of food items, lack of teaching and learning materials, inadequate contact hours, and poor implementation of the policy and the double-track system.

The government must comprehensively review the FSHS policy and consider cost sharing with parents and caregivers to sustain the policy. The accumulated debt is part of past excesses of the Ghana government flagship programs and, the corruption of the Ghana political system, the dysfunctional public sector, the high rate of tax evasion, tax exemption and persistent fiscal deficits.

In conclusion, Ghana domestic debt crisis has been caused by a combination of factors. The debt was accumulated over many years as successive governments borrowed heavily to finance public spending and social programs. Another factor was the country’s weak economy, which was hit hard by the Covid 19 pandemic and Russia and Ukraine. The crisis led to a sharp decline in economic growth, rising inflation, persistent depreciation of the local currency, and falling tax revenues. Ghana also suffered from a lack of competitiveness, with high labor costs and low productivity.

5.0. Ghana’s Domestic Debt Exchange Program (DDEP). (Debt Reduction)

Theoretical literature by Picarelli (2018) argues that the choice between these two restructuring strategies is usually driven by whether a country is experiencing a solvency or a liquidity crisis. Debt rescheduling is generally used to help solvent but illiquid countries that are temporarily unable to roll over their debt; Debt reduction is used instead in the case of insolvent countries that are permanently unable to pay back their debt. Deciding whether the Ghana restructuring domestic debt was the right decision hence involves two questions. First, had Ghana reached the threshold level of distress and high debt which would justify a debt restructuring purely from a domestic standpoint, abstracting from contagion?

Second in light of the collateral damage that the Ghana restructuring was likely to inflict on other institutions operating within the economic space – and arguably did– was there a better alternative? Ghana government decided to adopt the Domestic debt exchange to help protect the economy and enhance the country’s capacity to service the public debts effectively. The debt sustainability analysis demonstrated unequivocally that Ghana’s public debt was unsustainable, and that the Government would not be able to fully service its debt down the road if no action was taken. Indeed, debt servicing absorbed more than 50% of the total revenue and almost 70% of tax revenues, while the total public debt stock, including that of state-owned enterprises and all, exceeded 100% of GDP. This was reason why the government adopted the DDEP to help to restore the capacity to service the debt (MOF/05/12/2022). Public debt increased to 88.1 percent of GDP by end-2022, almost evenly split between external (42.4 percent of GDP) and domestic (45.7 percent of GDP), with the latter generating over 80 percent of overall debt service in 2022 due to high interest rates and short average maturity.

The situation of the public finances was unsustainable, with debt inclusive of the SOEs reaching 100% of GDP and nearly half of the budgetary resources in December 2022 dedicated solely to interest payments. On the domestic front, the government launched a debt exchange program in early-December, opting for a voluntary approach, seeking to swap outstanding medium- and long-term domestic bonds for lower-coupon and longer maturity bonds. The exchange, which covered about 65 percent of total outstanding domestic bonds (and excluded bonds held by pension funds to protect pensioners’ savings), received about 85 percent participation (IMF Country report, 23/168).

According to Bank of Ghana’s financial data on public debt rose to GH¢435.5 billion as of December. 2022 representing 88.1% of Gross Domestic Product with external debt stood at GHS 240 billion while the domestic debt also stood at GHS 194.8 billion. But however,the total public debt rose to GHC575.5 billion at the end of June 2023, with domestic debt at GHC246.9 billion and external debt at GHC328.6 billion at 80.1% of GDP. The persistent high fiscal deficit in the country has been partly attributed to the excessive government spending that was not productive and failed to effectively promote equitable development. During the period the central bank financed the government by ballooning deficits directly or by offered short‐term refinancing to banks by investing the liquidity in government securities. Regardless, this practice has exposed the economy to recent inflation and currency depreciation.

Large external shocks in recent years have exacerbated Ghana’s pre-existing fiscal and debt vulnerabilities, resulting in a loss of international market access, increasingly constrained domestic financing, and reliance on monetary financing of the government. Decreasing international reserves, Cedi depreciation, rising inflation and plummeting domestic investor confidence, eventually triggered an acute crisis. The authorities have taken bold steps to tackle these deep challenges, including by accelerating fiscal adjustment.In Ghana’s shallow financial market, especially where firms have limited access to international finance, domestic debt exchange could lead to swift and severe crowding out of private lending.

This raised the cost of private capital and created an adverse selection problem for banking institutions as more conservative risk-averse borrowers shy away from the credit market. To help restore macroeconomic stability, Ghana has secured a three-year IMF Extended Credit Facility (ECF) program of about $3 billion and has embarked on a comprehensive debt restructuring. The authorities have committed to a front-loaded fiscal consolidation while pursuing a tighter monetary policy, complemented by structural reforms in the areas of tax policy, revenue administration, and public financial management, as well as steps to address weaknesses in the energy and cocoa sectors.

The government launched a comprehensive debt restructuring to address severe financing constraints and the unsustainable public debt. The government has completed a Domestic Debt Exchange Program (DDEP), implemented an external debt repayments standstill, and sought official debt restructuring under the Common Framework. The revised- DDEP has marginally affected both profitability and solvency of the financial sector given its sizeable exposure to the public sector debt. However, the revised domestic debt exchange implemented has moderately affected the ability of domestic banks and businesses to grow, could possibly result in a decrease in overall economic output.

Additionally, restructuring including a “haircut”, has led to a further loss of confidence in the government’s ability to repay its debts and in the country’s economy. Both domestic and external debt became an issue when debt service payments become unaffordable compared to state revenue and other spending requirements. Ghana’s higher levels of debt repayments has resulted in: damage to economic growth as other spending is crowded out, constraints on the ability of governments to spend counter-cyclically, reduced resources for current spending needs, and also created debt overhang. As to address the above challenges, the country decided to adopt debt treatment from the Paris Club takes two forms: i rescheduling: i. Postponing debt service repayments, ii. reduction in debt service obligations: This occurs during a set period as flow treatment (debt service payments) or at a set date for stock treatment (treating the original loan and interest/arrears). Ghana adopted in domestic debt exchange in December 2022 as the country’s debt reduction methodology.

In the case of Ghana, debt exchange was one of the methodologies for debt reduction because the country was insolvent, i.e. permanent inability to honor debt obligations. In practice, sovereign debt resolution often includes a mixture of fiscal adjustment and additional funding coupled with a reduction of the outstanding debt, extending maturity of the debt from 3.8 years to 8.3 years and cutting the coupon rate from 19.1% per annum to 9.1%.

According to Minister of Finance the overall domestic bonds ¢203 billion were exchanged, which has resulted in debt service savings of ¢61.7 billion over 2023 (Joy business/17/10/2023). The Ministry of Finance posited the under-listed of domestic debt exchange program. Debt reduction might produce positive consequences by reducing the uncertainty level.

Indeed, a large amount of outstanding debt creates uncertainty about government’s future policies, since the debt servicing obligation will need to be met. As a result, economic agents will be inclined to postpone their investment decisions. Creditors would suffer a reduction in the market value of creditor exposure toward the debtor country, as high uncertainty might imply an increase in default risk. In this context, a debt reduction measure would help to restore normal conditions in the financial markets (i.e. markets do not like uncertainty).

The Original DDEP without the Pension. Cocoa bills, Domestic debt denominated bonds, Bank of Ghana non-marketable securities. The government launched on December 5, 2022, a DDEP covering all medium- and long-term debt issued in local currency by the Government of Ghana, Daakye and ESLA.

Government-issued T-bills have been excluded from the DDEP perimeter. The initial exchange did not yet include domestic debt denominated in U.S. dollars and Cocoa bills issued by Cocoa board. Over the course of discussions with bondholders the government also agreed that pension funds (representing about 20 of the debt eligible for the exchange) would not be expected to participate in the exchange. The original DDE settled on February 21, 2023. In total, 85 percent of the face value of bonds held by investors other than pension funds was exchanged in the DDE, equivalent to 28 percent of all outstanding domestic debt (which includes, among others, non-marketable debt, verified arrears and Cocoa bills). The government offered most bondholders a set of new bonds at fixed exchange proportions with a combined average maturity of 8.3 years and coupons up to 10 percent (with part of the coupons capitalized rather than paid in cash in 2023 and 2024). At a 16-18 percent discount rate, the final terms of the DDE imply an average NPV reduction of about 30percent for these bondholders.

Individual bondholders1/ were offered an exchange into shorter term debt with higher coupons. Crucially, the completed DDE has also produced very large cash debt relief for the government of almost GHS 50 billion in 2023, relieving pressure on the domestic financing market (IMF, 23/168).

7. Detailed of the Final Breakdown of Revised Restructured Domestic Debt (Debt Reduction)

On the revised DDEP included Treasury bonds, ESLA, Daakye bonds; US$742m restructured from dollar-denominated local bonds with average coupon rate and maturity period being 3% (previously 5.3%) and 1.5 years (4.5 years); GHS 7.7bn restructured from Cocoa bills with the coupon rate and maturity period being 13% (previously above 30%) and 4.4 years (previously 0.7 month); GHS 70.9bn principal haircut on the non-marketable debt instrument of the Bank of Ghana with the current coupon rate and maturity period 10% and 15 years respectively but excluded the pension bonds (MoF, 09/2023).

The breakdown of the GHS 203bn restructured domestic debt is as follows:

GHS 87bn restructured from Treasury bonds, ESLA and Daakye bonds excluding pension funds. The average coupon rate and maturity period of the restructured bonds currently stands at 9.1 (previously 19.1%) and 8.3 years (previously 13.8 years)

GHS 29.6bn restructured Pension Fund holdings in Treasury bonds, ESLA and Daakye bonds excluding pension funds. The coupon rate and average maturity period remains the same at 20% and 4 years respectively.

US$742m restructured from dollar-denominated local bonds with average coupon rate and maturity period being 3% (previously 5.3%) and 1.5 years (4.5 years).

GHS 7.7bn restructured from Cocoa bills with the coupon rate and maturity period being 13% (previously above 30%) and 4.4 years (previously 0.7 month).

GHS 70.9bn principal haircut on the non-marketable debt instrument of the Bank of Ghana with the current coupon rate and maturity period 10% and 15 years respectively.

DATA ANALYSIS USING THE NPV DISCOUNT RATE IS 16% (DEBT REDUCTION)

The government offered most bondholders a set of new bonds at fixed exchange proportions with a combined average maturity of 8.3 years instead of the original 13.8 years and coupons of up to 10 percent (with part of the coupons capitalized rather than paid in cash in 2023 and 2024).

It started by launching a voluntary Domestic Debt Exchange Program (DDEP), which is intended to increase average debt maturity from 3.8 years to 8.3 years instead of the original13.8 years and reduce average coupon payments from 19.1% to 9.1%, with only 5% paid in cash in 2023 and 2024. Crucially, the completed DDEP has also produced a very large cash debt relief for the government of almost GHS 61.7 billion in 2023, relieving pressure on the domestic financing market.

The average haircut on Ghana of Ghana and Bank of Ghana bonds of GHS 203 billion has resulted in government savings of GHS 61.7 billion or 30% haircut which at same time represented a significant loss to all bondholders especially Bank of Ghana that has taken massive hit to its balance sheet.

With push back by Trade Union Congress, Pension Funds, Individual Bondholders and Civil Societies the government decided to shift the original NPV losses to the Bank of Ghana in the revised DDEP to save the banking sectors.

We conclude that there was a reduction in the net present value of debt servicing costs does not mean that more money is available now for Ghana to spend. The reduction means that future debt servicing costs are reduced compared to the current baseline during the next decades and, therefore, Ghana would have to spend less on financing its debt in the future.