Bank of Ghana has appointed an advisor in the person of Dr. Joseph O. France to oversee the recapitalization efforts of Universal Merchant Bank Limited, commencing from March 25, 2024.

According to a statement released by the Central Bank, Dr. France will offer guidance to UMB’s management in supervising the implementation of governance reforms agreed upon by UMB and the Bank of Ghana.

This appointment aligns with section 101(1) of the Banks and Specialised Deposit-Taking Institutions Act, 2016 (Act 930).

“The Advisor will be at post at UMB until otherwise advised by the Bank of Ghana and will furnish the Bank of Ghana with a status report on the bank as frequently as the Bank of Ghana may require,” the statement said.

“It is important to note that an Advisor, unlike an Official Administrator, does not take over the powers, responsibilities, and duties of the bank’s shareholders, directors, or management. Under Act 930, the Advisor may attend meetings of the Board of Directors or Committees of the bank without voting at such meetings,” it added.

Nonetheless, the BoG gave UMB’s clients and depositors the reassurance that the financial institution is still operational and run by the management group of UMB.

The Central Bank went on to say that it is still dedicated to fostering a stable and resilient banking industry that continues to enjoy the public’s trust.

The $300 million World Bank facility earmarked for various projects in 2024 has finally been transferred to the Bank of Ghana’s (BoG) account.

Ghana fulfilled all necessary conditions, including securing approvals from Cabinet and Parliament, to facilitate this transfer. According to Joy Business, the funds were transferred on the morning of March 27, 2024.

The BoG is now expected to convert the dollars into cedis and distribute the equivalent amount to government agencies and ministries.

The foreign exchange component of this facility is expected to bolster the international reserves of the Bank of Ghana. Data from the BoG indicates that its Gross International Reserves exceeded $6 billion by the end of February 2024.

Finance Minister Dr. Mohammed Amin Adam recently stated during a media engagement that the government anticipates receiving around $1.2 billion from development partners before the year ends. This disbursement is crucial for expediting infrastructure projects outlined in the 2023 Budget that were delayed due to the late arrival of donor support.

Originally scheduled for disbursement late last year, the World Bank’s release of this facility was delayed as Ghana struggled to reach an agreement with its bilateral creditors, hampering the approval process for the $300 million loan.

This inflow is expected to curb the depreciation of the cedi by signaling to the international market that the Central Bank is better equipped to stabilize the local currency.

The $300 million Development Policy Financing, the initial tranche of a three-part series, is aimed at crisis response and resilience-building in Ghana. Its primary objectives include restoring fiscal sustainability, enhancing financial sector stability and private sector development, improving energy sector financial management, and bolstering social and climate resilience.

This disbursement is expected to enhance domestic revenue mobilization, control expenditures, ensure financial sector stability, facilitate private investment, stabilize the energy sector financially and operationally, fortify the country’s social protection system, and integrate climate adaptation and mitigation into policies.

Background: This disbursement is part of the overall financial support from Ghana’s donors as part of the IMF program secured by the country in May 2023. The IMF has already provided approximately $1.2 billion to Ghana under the FUND program.

According to the World Bank, this initial tranche of the Resilient Recovery Development Policy Financing is a crucial contribution from the Bank’s International Development Association. It is designed to assist Ghana in its economic recovery and promote resilient and inclusive growth.

The World Bank approved this facility in January 2024 following an agreement in principle by the Official Creditors’ Committee under the G20 Common Framework on the key parameters of Ghana’s proposed debt restructuring. This agreement aligns with the Joint World Bank-International Monetary Fund Debt Sustainability Framework, marking a significant step toward restoring debt sustainability.

Governor of the Bank of Ghana (BOG), Dr. Ernest Addison expressed optimism regarding the stability of the Ghana cedi against the US dollar in the near future.

He attributed this confidence to the robust reserves accumulated by the Bank of Ghana and the implementation of fresh monetary measures along with stringent enforcement of foreign exchange regulations.

Dr. Addison emphasised that the Bank of Ghana’s reserves had surpassed $6.0 billion, marking a significant improvement in the factors that previously exerted pressure on the cedi.

“This is based some strong reserves that the Bank of Ghana has built over the past months to support the cedi, some fresh monetary measures being implemented, and strict enforcement of the foreign exchange regulations.

“We are now reporting reserves of more than $6.0 billion, and therefore the underlying factors that caused those pressures in the past have improved greatly”, Dr. Addison disclosed.

He highlighted increased remittance inflows as well, which are expected to bolster the currency’s performance in the upcoming months.

“We believe that all these developments should give the market some assurance that the cedi’s outlook will remain favourable”.

Addressing concerns about recent challenges faced by the cedi, especially in the first quarter of 2024, Dr. Addison acknowledged a depreciation of about 6.8% against the US dollar.

“These were compounded by delays and uncertainties associated with the second tranche of the cocoa loan inflow and World Bank’s disbursement of budget support”, the Governor added.

However, he noted that measures taken by the central bank throughout 2023 and recent months were beginning to show positive responses.

Despite pressures stemming from the strength of the US dollar in global markets and payments to sectors like energy and corporate, Dr. Addison pointed out mitigating factors such as remittance inflows, mining company contributions, and the Domestic Gold Purchase Programme.

“Inflows from the World Bank, the tight monetary policy stance, and a weaker US dollar from potential policy rate cuts in the USA are expected to support the relative stability of the Ghana cedi”, he pointed out.

He also mentioned expectations of support from inflows, a tight monetary policy stance, and potential US policy rate cuts affecting the US dollar’s strength.

Dr. Addison discussed the revised cash reserve ratio and emphasized the central bank’s commitment to strict enforcement of foreign exchange regulations as measures to uphold the cedi’s performance in the upcoming weeks.

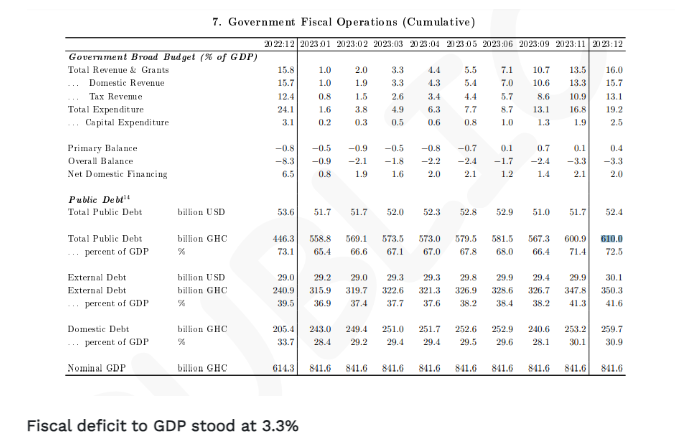

The Bank of Ghana‘s (BOG) March 2024 Summary of Economic and Financial Data has revealed that Ghana‘s public debt has soared to GH¢610 billion ($52.4 billion) by the end of 2024.

This marks an increase of GH¢42.7 billion from September 2023 to December 2023, following a previous decline of ¢14.2 billion between June 2023 and September 2023, when it stood at ¢567.3 billion ($51.0 billion).

The current debt level accounts for 72.5% of the country’s Gross Domestic Product (GDP), indicating that Ghana’s debt situation remains challenging despite the completion of the Domestic Debt Exchange Programme.

The rise in debt is attributed to a GH¢19.1 billion increase in domestic debt and a GH¢23.6 billion increase in external debt, primarily due to the depreciation of the cedi.

According to the Central Bank’s data, the external component of the total public debt was $30.1 billion (¢350.3 billion) in December 2023, representing 41.6% of GDP.

Meanwhile, domestic debt stood at ¢259.7 billion, accounting for about 30.1% of GDP.

The report, however, lacks information on the financial sector resolution debt and other liabilities like the energy sector debt.

Despite these challenges, the government’s fiscal operations remained on target, with the deficit-to-GDP ratio standing at 3.3% in December 2023, down from 8.3% in December 2022.

Additionally, there was a surplus of 0.4% of GDP in the primary balance in December 2023.

Ghana had suspended interest payments on loans to external creditors in December 2022 amid economic difficulties and is currently in negotiations with bondholders after reaching a deal with bilateral creditors in January 2024.

The Head of FinTech and Innovation at the Bank of Ghana (BoG), Kwame Oppong, has anticipates that the upcoming 3i Summit will elevate Ghana as a prime hub for fintech investments across Africa.

Speaking at the Ghana Fintech and Payments Association Awards event in Accra, Oppong emphasized the potential of the 3i Summit to draw significant investment to Ghana, thanks to the anticipated presence of global fintech leaders.

The Fintech Awards event not only acknowledges the accomplishments of outstanding fintech and payments companies but also serves as a platform for industry stakeholders to convene and strategize on enhancing the sector’s growth.

With Ghana emerging as a favorable landscape for fintech, boasting over 70 such enterprises, Oppong believes the 3i Summit will serve as a catalyst for policy discussions, entrepreneurial ventures, and networking opportunities within the industry.

Oppong called upon banks and fintech firms to collaborate in organizing and supporting the summit, stressing that collective participation is key to its success.

Highlighting the pivotal role of fintech companies in advancing Ghana’s financial inclusivity, Oppong noted a significant rise in the country’s financial inclusion index from 58% in 2017 to 68% in 2021.

The 3i Africa Summit, a collaborative effort between the Bank of Ghana, the Monetary Authority of Singapore, Development Bank Ghana, and Elevandi, aims to drive innovation, investment, and impact in Africa’s fintech and financial services sectors.

Scheduled for May 13 to May 15, 2024, at the Accra International Conference Centre, the summit promises to be a pivotal event for the fintech ecosystem in Africa.

Nana Hemaa Ama Anim, Vice President for Women in Fintech, hailed the awards as a source of inspiration, fostering creativity, partnerships, and progress not only within fintech but across the entire financial sector.

“I therefore extend an invitation to all banks and fintech companies to fully participate in diverse ways to organise this summit. Together, we can make the summit a success for all of us in the industry. The summit is for all of us to participate, so let us come on board and work together,” he said.

She said the, “Women in FinTech” programme aimed at closing the gender disparity, empowering women, and supporting the creation of fintech companies led by women.

According to the January 2024 Monetary Policy Report from the Bank of Ghana, the real sector of the economy showed a mixed performance in the eleven months of 2023.

Consumer spending, indicated by domestic VAT collections and retail sales, saw a strong performance in November 2023 compared to the same period in 2022.

Domestic VAT collections increased significantly by 128.9% year-on-year to GH¢1.978 billion, while total domestic VAT for the first eleven months of 2023 rose by 66.6% to GH¢12.831 billion.

Retail sales also increased by 2.4% year-on-year to GH¢193.12 million in November 2023, up from GH¢188.60 million in November 2022. Cumulatively, retail sales for the first eleven months of 2023 rose by 30.4%.

In the manufacturing sub-sector, indicated by trends in the collection of direct taxes and private sector workers’ contributions to the Social Security and National Insurance Trust (SSNIT) Pension Scheme (Tier-1), there was an improvement in November 2023. Total direct taxes collected increased by 135.3% year-on-year to GH¢5.880 billion in November 2023, while total direct taxes collected for the first eleven months of 2023 rose by 60.6% to GH¢44.432 billion.

However, activity in the construction sub-sector, indicated by the volume of cement sales, declined by 13.2% year-on-year in November 2023 to 231,571.37 tonnes, down from 266,695.03 tonnes a year ago. Cement sales for the first eleven months of 2023 also decreased by 25.1% to 2,358,386.77 tonnes.

Transport sector activities, indicated by new vehicle registrations by the Driver and Vehicle Licensing Authority (DVLA), declined by 14.8% to 7,268 in November 2023, from 8,533 vehicles registered in November 2022. Cumulatively, vehicles registered by the DVLA within the first eleven months of 2023 decreased by 35.7% to 135,544.

Passenger arrivals, however, improved by 25.5% year-on-year to 104,157 in November 2023, compared to 82,977 arrivals a year ago. Cumulatively, for the first eleven months of 2023, there were 1,019,841 arrivals recorded at the international airport and land borders, representing a growth of 25.8% compared to the same period in 2022.

International trade at the two main harbors (Tema and Takoradi) showed improvement, with total container traffic increasing by 28.8% year-on-year to 57,738 in November 2023. However, in cumulative terms, total container traffic for the first eleven months of 2023 dipped by 3.3% to 570,711, compared to the same period in 2022.

The Development Bank Ghana (DBG) has reiterated its dedication to fostering the advancement of women entrepreneurs in the nation.

During the Investment Climate Reform (ICR) Facility – Development Bank Ghana Stakeholder Workshop, the bank’s Deputy Chief Executive, Michael Mensah-Baah, unveiled DBG’s initiative to empower 500 women-led enterprises.

These businesses are set to benefit from the GH₵1 billion fund, which DBG and its partners aim to deploy to support Micro, Small, and Medium Enterprises (MSMEs).

Mensah-Baah highlighted DBG’s collaboration with pertinent stakeholders and likeminded financial institutions to realize this objective within the next three to five years.

“DBG is a wholesale lending institution, that is, we lend to other financial institutions so we need to have partners who are like-minded like us, who will work with us, and who share this same ambition of being able to support women-led businesses,” he said on Wednesday.

This initiative is a direct response to the significant challenge of limited access to financial assistance for women.

During discussions with the media at the event, Mr. Mensah-Baah recognized the existing gap in financial access. Despite women owning 50 percent of businesses in Ghana, only 10 percent of these businesses have access to funding.

He emphasized that the workshop aimed to identify and overcome the obstacles hindering women entrepreneurs from accessing the financial support they need.

“The issue we have discovered is that women who are available to receive this funding still struggle to get funding and we needed to have this workshop to understand some of the barriers that prevent them from accessing the funding.

“This is because even though the funding is available and the women are unable to access it, we won’t achieve our ambition of providing long-term capital for these women,” he stated.

According to him, the bank will not only provide financial support but will also offer capacity-building and technical assistance to empower women-led businesses.

He believed this technical training would support women-led businesses, facilitate their growth, and transform their businesses from micro-enterprises into large corporate entities in Ghana.

Emina Abrahamsdotter of the GFA Consulting Group, on her part encouraged collaboration between stakeholders to improve women’s access to finance in the country.

She also noted that staff of DBG and 15 other financial institutions will be trained on gender equality, gender mainstreaming and women’s financial empowerment.

Taking her turn, the Team Lead of Women Banking of Access Bank Ghana, Charity Ahadzie highlighted the numerous challenges faced by women entrepreneurs including lack of access to networking opportunities, information and finance.

She therefore noted that educating and training these women is a crucial form of empowerment to assist them grow their various businesses.

Madam Ahadzie therefore noted that her outfit which is a PFI-partner of DBG readily undertakes capacity building events to ensure that “whatever they are learning they will be able to plow it back into their businesses that way when you lend to them their businesses will grow and they will be able to repay.”

In response to the rapid growth in mobile money transactions and evolving customer needs, the Bank of Ghana (BoG) has announced revisions to the balance and transaction limits of mobile money wallets, effective March 1, 2024.

The decision to revise the limits comes after the release of the 2023 Fintech Sector report by the Bank of Ghana, which highlighted a significant surge in mobile money transactions.

According to the report, there was a remarkable 79 percent increase in the total value of Mobile Money transactions, reaching GHS1.9 trillion compared to the figures recorded in 2022.

Additionally, the total value of Mobile Accounts (Funds) held with commercial banks witnessed a 40% increase, reaching GHS18.3 billion.

Acknowledging the growing trends in transactional activities and the need to accommodate evolving customer demands, the Bank of Ghana deemed it necessary to adjust the transaction limits for various customer accounts.

Effective March 1, 2024, the newly approved guidelines include adjustments to the transaction limits for different customer accounts.

These adjustments aim to ensure that mobile money users can effectively conduct their transactions while maintaining the security and integrity of the mobile money ecosystem.

The revisions in transaction limits are expected to provide greater flexibility and convenience for mobile money users across the country. Furthermore, it aligns with the Bank of Ghana’s commitment to fostering financial inclusion and promoting the use of digital financial services in Ghana.

As mobile money continues to play a vital role in driving financial inclusion and economic growth in Ghana, the Bank of Ghana remains committed to monitoring and adapting to the evolving needs of mobile money users and the broader financial ecosystem.

In response to the surge in mobile money transactions and evolving customer needs, the Bank of Ghana (BoG) has announced adjustments to the balance and transaction limits of mobile money wallets, effective March 1, 2024.

The decision follows the findings of the 2023 Fintech Sector report, revealing a significant 79 percent increase in the total value of Mobile Money transactions, reaching GH¢1.9 trillion compared to 2022 figures.

Mobile Accounts (Funds) held with commercial banks also saw a 40% increase, reaching GH¢18.3 billion.

The revised guidelines include adjustments to transaction limits for different customer accounts:

Minimum Account, Medium Account, and Enhanced Account:

Previous Limits: GH¢2,000, GH¢10,000, and GH¢15,000

Revised Limits: GH¢3,000, GH¢15,000, and GH¢25,000 respectively

Minimum Know Your Customer (KYC) Account:

Previous Limit: GH¢3,000

Revised Limit: GH¢5,000

Medium Know Your Customer (KYC) Account:

Previous Limit: GH¢25,000

Revised Limit: GH¢40,000

Enhanced Know Your Customer (KYC) Account:

Previous Limit: GH¢50,000

Revised Limit: GH¢75,000

Additionally, the monthly transaction limit for a Minimum KYC Account has increased from GH¢6,000 to GH¢10,000. Medium and Enhanced accounts, which had no previous limits on the value of monthly transactions, remain unchanged.

The Ghana Chamber of Telecommunications, as an advocacy institution, encourages the public to seek clarification at any of their members’ customer service centers across the country.

Effective March 1, 2024, the Bank of Ghana (BoG) has increased the balance and transaction limits for customers’ mobile money wallets.

This adjustment comes in response to the growing trend of transactional activities and changing customer needs.

The Ghana Chamber of Telecommunications released a statement highlighting these changes. Under the new limits, daily transaction limits have been raised for different account tiers.

For example, the minimum account, which previously had a GH¢2,000 limit, has been raised to GH¢3,000. Similarly, the medium account limit has been increased from GH¢10,000 to GH¢15,000, and the enhanced account limit has been raised from GH¢15,000 to GH¢25,000.

For maximum accounts, the minimum account limit has been increased from GH¢3,000 to GH¢5,000, the medium account limit has been raised from GH¢25,000 to GH¢40,000, and the enhanced account limit has been increased from GH¢50,000 to GH¢75,000.

Regarding monthly transaction limits, the minimum account limit has been raised from GH¢6,000 to GH¢10,000. The medium and enhanced accounts, which previously had no limits on the value of monthly transactions, remain unchanged.

“Kindly reach out to the personnel of our members at any of their customer service centers across the country, for any clarification you may need”, the statement concluded.

In the fourth quarter of 2023, banks and Specialised Deposit-Taking Institutions (SDIs) extended secured loans with a combined value of GH¢5.9 billion, according to the Bank of Ghana (BoG)

This represents a significant decrease of 54.9% compared to the GH¢13.2 billion recorded in the same period in 2022.

Breaking down the figures from the 4th Quarter Collateral Registry Report, it is revealed that banks contributed GH¢4.5 billion to the total secured loans in Q4 2023, marking a notable decline of 63.0% from the GH¢12.3 billion reported in Q4 2022.

This decline signals an overall deceleration in credit growth for the year, indicating a strategic portfolio reallocation by banks.

Conversely, SDIs experienced an uptick in secured loans, recording a total of GH¢1.4 billion in Q4 2023.

This reflects a significant increase of 53.0% from the GH¢918.7 million reported in the same period in 2022.

Examining the distribution of secured loans, banks maintained the largest share in Q4 2023, accounting for 76.3% of the total value, down from 93.0% in Q4 2022.

Savings and Loans Companies saw an increased share, rising to 13.3% in Q4 2023 from 4.2% in Q4 2022. Rural and Community Banks followed with a percentage share of 6.9%, up from 1.9% in Q4 2022. Microfinance Companies also experienced a rise in share, reaching 1.7% in Q4 2023 from 0.3% in Q4 2022. Additionally, Finance Houses saw a slight increase, from 0.1% in Q4 2022 to 0.5% in Q4 2023.

In a bid to mitigate the risk of being blacklisted by the European Union and the United Kingdom, the Bank of Ghana has announced proactive measures.

These steps underscore the institution’s dedication to collaborative efforts with key stakeholders in the financial sector.

Following a comprehensive evaluation of Ghana’s anti-money laundering and counter-terrorism financing regime by the Financial Action Task Force (FATF) in 2022, Ghana was successfully removed from the EU blacklist.

Second Deputy Governor Elsie Addo-Awadzi has expressed the Central Bank’s commitment to working closely with other stakeholders to maintain this achievement.

Speaking at the Financial Intelligence Centre Ghana’s Risk Assessment on Money Laundering and Terrorism Financing forum, Addo-Awadzi emphasized the importance of sustaining the positive outcomes derived from previous reforms.

“As we proceed to the third round of the mutual evaluation process next year, it is imperative that we sustain the fruits of the hard work exerted by all stakeholders that led to critical reforms and implementation that persuaded FATF, the EU, and the UK to remove Ghana from any adverse listings for ML/CFT/PF risks. All stakeholders must continue to work to maintain an effective AML/CFT/PF regime that stands the test of time,” she said.

The Deputy Governor urged financial institutions to back the Central Bank’s efforts in combating money laundering and terrorism financing. Stressing the importance of the National Risk Assessment (NRA), she underscored its role in enabling a thorough self-assessment of the financial system’s development and the efficacy of the current regulatory framework.

“This NRA presents us a rare opportunity to critically self-assess, taking into account the evolution of our financial system and all key sectors of our economy and how business is being conducted since the last assessment, as well as relevant external factors, and to critically assess whether our AML/CFT/PF regime after all the recent reforms remains robust in the face of these developments.”

She further assured that, “The Bank of Ghana, as the guardian of the monetary system, remains committed to playing its parting as a regulator to support the successful completion of the NRA and a successful Third Round Mutual Evaluation exercise.”

The world of central banking is surprisingly replete with accusations of plagiarism.

The governor of Turkey’s central bank between 2019 and 2020 (and vice governor before then), Murat Uysal, was pilloried by local academics for plagiarising large portions of his Master’s thesis and two published works. He did not get fired for it. After the Turkish Lira lost 30% of its value, however, he was shown the door and replaced with Naci Agbal. Four months later, Naci was summarily dismissed and the job was given to Şahap Kavcıoğlu. No sooner had Sahap settled in than his Alma Mater confirmed an investigation into his PhD thesis. The verdict: large tracts of the text had been lifted from Turkish central bank annual reports. He survived the scandal and stayed in office until the Turkish President tired of him last year.

Around the same time that Sahap was defending his academic integrity, accusations started to fly that the Icelandic central bank governor, Ásgeir Jónsson, was guilty of a similar sin. A Norse Philologist, Bergsveinn Birgisson, with a deep expertise in mythical fiction, was the accuser. The strange intersection of their interests was on the subject of the first settlement of Iceland, on which both had published books. Birgisson says Jonsson stole important hypotheses from his work without attribution. Jónsson denied. Not much came of the dispute.

Much closer to home is the better-known case of the United States–based academic, Victor Dike, and his campaign to bring then governor of the Central Bank of Nigeria (CBN), Lamido Sanusi, to justice for copying from three pages of Dike’s academic paper without giving him the slightest bit of credit. The CBN responded with the most uproarious of excuses: the governor didn’t write the speech, didn’t deliver it on his behalf, and was merely a ventriloquist for the CBN itself in his public speaking appearances! Professor Dike insisted that he will see the governor in Court, and the CBN could follow him there if they so wished. The matter seems lost in the maze that is the Nigerian justice system.

This is the somewhat checkered background against which Ghanaian entrepreneur and development finance specialist, Kofi Arkaah, brings his charge against the Bank of Ghana. Except, perhaps luckily, he is not accusing any official there of lifting verbatim from his published work for their own speeches, theses or academic papers. In some ways, though, his allegation is just as concerning. He is accusing the Bank of Ghana of basing a major policy initiative on a technical model he developed and shared with one of their most senior officials, but doing so sneakily and dishonestly to avoid acknowledging his contributions.

Mr. Arkaah has shown a trail of correspondence to this author which establishes clearly that he did share with a very senior official at the central bank a draft model, and underlying data, on how to develop an optimal gold reserves policy for Ghana. One that would complement the country’s inflation-targeting regime and bolster the national currency by carefully managing the ratio between gold reserves and overall gross international reserves. The trail of correspondence shows the senior official initially expressing a willingness to help Arkaah refine the model before abruptly terminating the engagement.

Arkaah’s need for research support to benchmark the model with data from the Eurozone and WAEMU is what had initially driven the aborted collaboration in 2017. Not much happened in the ensuing years.

Central bank gold reserves as a relative measure. Chart Source: Refinitiv GFMS, World Gold Council & James Steel/Centralbanking.com (2023)

It would seem, however, that some time after the senior Bank of Ghana official terminated the engagement, an army of research assistants were detailed to dig into Arkaah’s data and initial model. In 2021, the Bank of Ghana announced the Gold Purchase Program.

Central bank gold reserves as an absolute measure. Chart Source: IMF (2023)

In his speech heralding the start of the program, the governor gave credit for the idea of developing a gold-backed reserves optimisation policy solely to the sitting Vice President:

“Ladies and Gentlemen, before I conclude, let me acknowledge the support of His Excellency the Vice President, Dr. Mahamudu Bawumia who got this programme started.”

Attentive observers would have noted similar content in the recent UPSA speech of the Vice President. To be clear, Arkaah does not accuse the Vice President of any complicity in these matters.

It is generally the case that intellectual property (IP) infringement cases brought against central banks usually involve technology applications, and are rarely successful. Examples being the lawsuit brought against the European Central Bank by Rochester-based Document Security Systems and Technocrat Consult & IT Limited’s legal action against the Central Bank of Nigeria. However such technology-related IP disputes normally involve patents, not copyrights, and not all disputes are meant for the courts. Reputational consequences also matter.

Indeed, many of the lawsuits currently underway against Artificial Intelligence (AI) companies worldwide involve the uncredited incorporation of copyrighted work into complex, dynamic, models, and the reputational blowback against tech companies for being perceived as ripping off poor creatives. IP lawsuits involving financial models and research are, actually, also not all that unheard of, a case in point being the famous Barclays Capital vs theflyonthewall.com litigation (where the American courts did make a finding of copyright violation).

In bringing this matter to the public’s attention, Arkaah says he is not looking for cheap fame or monetary compensation. To his mind, the policy ecosystem of any serious country is a community of practice. In such a community, it is critical that ideas are properly sourced and attributed to encourage innovative thinking, a sound competition of ideas, and professional integrity.

He does not mind at all that the technical mechanics of aligning central bank gold purchases with other macroeconomic variables were, to his mind, clearly extracted from his model by the Bank of Ghana. He wants many African countries looking to back their currency with gold to do similar statistical heavy-lifting and not fall into the same trap that the likes of Zimbabwe did when they went down that road without a well-calibrated model.

He is peeved however that rather than seeing an opportunity to engender dialogue with the policy community so that the model could be refined for Ghana’s benefit, the Bank of Ghana stealthily appropriated his ideas, and that its officials are busily making unnecessary partisan political capital out of it. To Arkaah’s mind, that kind of conduct does not become a technical organisation that must stay above politics, guard its institutional independence jealously, and nurture the sharpest technocratic thinking and practice. Moreover, the documented allegations of appropriation of intellectual property, without even the basic trivial courtesy of acknowledgement, reinforce a pattern of impunity, which the Ghanaian central bank has been oft accused of perpetrating.

Readers will note that, to date, the Bank of Ghana (BoG) has failed to publish any serious position papers on either the so-called Gold for Oil program or the program referenced in this essay, the Gold Purchase Program. Consequently, the policy and academic communities have been unable to provide robust feedback and subject the BoG’s thinking to the necessary intellectual scrutiny. And, now, we see clear evidence in this Arkaah affair of the BoG’s undue wariness in engaging with professionals desirous of contributing ideas to enhance monetary policymaking in Ghana.

This author’s consistent complaints about the shifty conduct of central banking in the current dispensation finds at least partial vindication in the Arkaah claims. Whether it is concerning the contentiousrecapitalisation program, the botched bailout funds recovery effort, or the BoG’s very murky approach to procurement, the usual style has been one weighed down by a total lack of candour, transparency, openness to scrutiny, and good-faith dealings with public stakeholders.

Mr. Kofi Arkaah tells this author that his intellectual campaign about optimal gold reserves and ideal ratio will not be curtailed by this setback. It is an idea, he says, destined for continental relevance. And he is only getting started.

Source: Bright Simons is the vice-president, in charge of research at IMANI Centre for Policy and Education.

DISCLAIMER: TIGPost.co will not be liable for any inaccuracies contained in this article. The views expressed in the article are solely those of the author’s, and do not reflect those of The Independent Ghana.

Director of Research at the Institute of Economic Affairs (IEA), Dr. John Kwakye, has criticized the characterization by New Patriotic Party flagbearer Dr. Mahamudu Bawumia of the GH¢60.81 billion losses posted by the Bank of Ghana for the year 2022 as merely “technical losses.”

According to the economic researcher, these losses will inevitably result in cuts to essential operations of the Bank as it seeks to mitigate costs.

In a piece titled “Dr. Bawumia’s Speech: Turning an Impossibility into the Possibility?”, Dr. Kwakye highlighted the immediate effects of these losses, particularly noting the fluctuating inflationary figures experienced by the country.

“Dr. Bawumia said BoG’s action was responsible and that it was temporary, as the Bank had advanced money to Government in only two of the past seven years. The Minister of Finance had expressed similar sentiments in the past, which was not surprising because Government was the direct beneficiary of the monetary financing.

“However, as central bankers, we know that the most inflationary source of financing the budget is high-powered money coming directly from the central bank vault. It is not the fact that BoG advanced money to Government that is the issue, for the Bank’s Act provides for such advances up to 5% of the previous year’s revenue. It is the magnitude of the advance—over 50% of the previous year’s revenue—that is disturbing. It is no wonder inflation peaked at 54.1% in 2022—and depreciation ballooned to 54.2% in November 2022, before falling bank to 30.0% in December 2022. Meanwhile, as Government debt to BoG was also discounted under the DDEP, the Bank made a whopping loss of GHS61 billion and a record negative equity of GHS54 billion in 2022.”

Dr. Kwakye contended that despite attempts by Finance Minister Ken Ofori-Atta and the Bank of Ghana to downplay the significance of the loss, the country’s balance sheet has been significantly affected.

“Both the Minister and the Governor seem to have played down the loss as only a technical loss. However, the fact is that the Bank’s balance sheet has been severely impacted, and this would force it to cut back on some of its important operations so as to save costs.”

Vice President Dr Mahamudu Bawumia commended the Bank of Ghana (BoG) for its prudent measures rolled out in efforts to stabilize the Ghanaian economy during the COVID-19 pandemic.

Delivering an address to Ghanaians on February 7, 2024, the Vice President noted that BoG was very instrumental in bringing the economy back on track after the pandemic hit the shores of the country.

He noted that the institution had been unfairly criticized despite its pivotal role in pulling the economy back from the brink.

“I must at this stage salute and give particular recognition to the Bank of Ghana which has come under unfair criticism for taking the necessary measures which helped pull the economy back from the brink,” he said.

Dr. Bawumia particularly lauded the BoG for prioritizing the interests of Ghanaian citizens and providing necessary financing to the government during critical moments.

“BoG provided needed financing to the government at that critical moment. What the BoG did was very responsible in putting the interest of the good citizens of Ghana first,” he added.

Dr. Bawumia emphasized that the data available clearly demonstrates the temporary nature of the financing provided by the BoG to the government, with zero financing recorded in five out of the last seven years, including 2017, 2018, 2019, 2021, and 2023.

Highlighting the context behind the BoG’s financing of the government during specific periods, Dr Bawumia pointed to domestic and global crises, such as the COVID-19 pandemic in 2020 and the liquidity crisis in 2022.

These challenges, coupled with underperforming revenue and limited access to international capital markets, necessitated support from the BoG to sustain the economy during turbulent times.

“The data which is available shows that the financing provided to the government by the Bank of Ghana was temporary. The Bank of Ghana has provided zero financing in five out of the last 7 years. Zero financing in 2017, 2018, 2019, 2012 and 2023.

“The BoG financing of the government in the COVID-19 year of 2029 and the liquidity crisis year of 2022 was because of the domestic and global crisis with underperforming revenue and no access to international capital markets. Ladies and gentlemen, the good news is that the data shows that the economy is recovering from the crisis we faced,” he added.

The Bank of Ghana has scheduled a meeting for today, February 6, 2024, which will involve officials from the Ghana Revenue Authority and various stakeholders in the financial sector.

The purpose of the meeting is to tackle concerns raised by mobile money users regarding unauthorized deductions during transactions.

This initiative comes in response to a significant number of complaints from mobile money users who have experienced deductions beyond the authorized 1.0% levy following the implementation of the Electronic Transfer Levy.

During a media briefing in Parliament on February 5, 2024, Sam George, the Deputy Ranking Member on Parliament’s Communications Committee, expressed these concerns. He urged authorities to promptly address the issue and voiced apprehensions about the implementation structure of the e-levy.

“I still hold the view that the whole implementation architecture of this e-levy is problematic, and the government needs to sit down and understand what it wants to do and not be in a hurry. President Akufo-Addo told us he is in a hurry but he is in a hurry to fail, and that is exactly what they are achieving,” Sam George remarked.

He revealed information about an imminent meeting that will include the Bank of Ghana, Electronic Money Issuers (EMIs), telecommunications companies, and banks. The purpose of the meeting is to address systemic issues related to the ELMAS system, particularly focusing on the challenge of real-time data uploads.

He revealed information about an imminent meeting that will include the Bank of Ghana, Electronic Money Issuers (EMIs), telecommunications companies, and banks. The purpose of the meeting is to address systemic issues related to the ELMAS system, particularly focusing on the challenge of real-time data uploads.

The Bank of Ghana (BoG) has introduced the Beta Version of its Database Portal, a significant move towards consolidating macroeconomic data retrieval and visualization.

This initiative highlights the institution’s dedication to transparency and adherence to global standards within its inflation targeting framework of monetary policy.

The newly unveiled portal aims to simplify data access for the general public and researchers while catering to the increasing demand for economic information.

Structured into five primary economic sectors—External, Financial, Fiscal, Monetary, and Real Sector—along with Survey-Based Indicators, the portal hosts 255 monthly and 86 quarterly time series data collected from the BoG and other pivotal stakeholder institutions.

Regular data updates and revisions will be synchronized with the Data Release Calendar published on the portal, ensuring users have access to the most up-to-date information.

By centralizing data on a single platform, the Bank of Ghana seeks to improve data accessibility and facilitate informed decision-making processes across various sectors.

To access the wealth of macroeconomic data available on the Portal, individuals are invited to visit; https://app.datawarehousepro.com/go/bog/

Despite the Bank of Ghana’s efforts to stabilize the currency by selling $7 million in the spot market and conducting a $20 million auction to Bulk Oil Distribution Companies, the cedi depreciated by 0.60% against the dollar last week.

So far this year, the cedi has lost about 2.5% of its value, mainly due to increased demand from corporate entities, especially in the energy and agricultural sectors.

Currently, the cedi is trading at GH¢12.48 against the US dollar in the retail market and GH¢12.07 on the interbank market.

Analysts predict that the currency may see some stability this week.

This expectation is based on lower corporate demand for foreign exchange as importers have already stocked up ahead of the Chinese holidays from February 9 to February 15, 2024.

The Bank of Ghana (BoG) has unveiled the Beta Version of its Database Portal, a crucial step towards creating a unified platform for extracting and visualizing macroeconomic data.

This initiative aligns with international best practices and reflects the Bank’s dedication to enhancing transparency within its inflation targeting framework for monetary policy.

The portal serves the dual purpose of meeting data requests from the public and supporting research endeavors.

Organized into five primary Economic Sectors—External, Financial, Fiscal, Monetary, Real, and Survey-Based Indicators—the data encompasses 255 monthly and 86 quarterly time series sourced from the BoG and key stakeholder institutions.

Regular updates and revisions, following the published Data Release Calendar on the portal, ensure the information’s accuracy and relevance. For access to data on the Portal, visit the official website: https://app.datawarehousepro.com/go/bog/

RightCard Payment Services Limited, also known as LemFi, has received approval from the Bank of Ghana (BoG) to resume its remittance services to Ghana in collaboration with approved partners.

The approval aligns with RightCard’s commitment to providing secure and efficient services while adhering to the regulatory framework set by the Bank of Ghana.

Following a temporary suspension of its money transfer services in November 2023, RightCard (LemFi) has officially announced the resumption of its services to Ghana.

The company will now operate through approved partners, including payment companies BigPay and ExpressPay, as sanctioned by the Bank of Ghana.

RightCard (LemFi) offers innovative services and products in various markets through its LemFi app. Notably, LemFi is already licensed as an Electronic Money Institution with the Financial Conduct Authority in the United Kingdom.

“We are grateful to stakeholders at the Bank of Ghana as well as our partners for their role in ensuring service restoration”, said Precious Ama Kwartemaa Oduro, LemFi’s Country Manager.

“We resume our operations with a better understanding, and we are now better positioned to address the evolving needs of the Ghanaian market,” she added.

LemFi’s reentry into the Ghanaian market comes with a renewed emphasis on enhancing customer satisfaction, strengthening collaborations with crucial stakeholders, and a dedication to advancing financial inclusion.

Both current and potential customers are now able to benefit from LemFi’s offerings, including competitive exchange rates, zero transaction fees, and instant transfer delivery. To access these services, individuals can download the LemFi app from the iOS or Google Play Store.

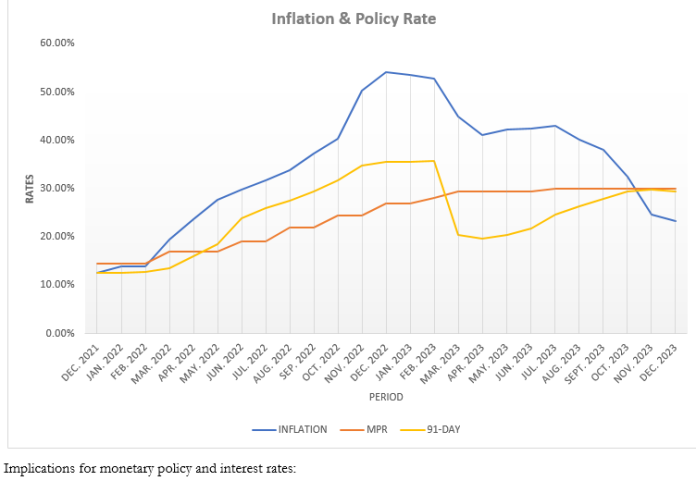

TheBank of Ghana( BOG) announced on Monday, January 29, 2024, that it will lower the policy rate by 100 basis points.

The decision was made in light of growing inflationary risks.

Ghana Commercial Bank (GCB) Capital explains that the Monetary Policy Committee (MPC) decided on a cautious position because of variables that are aiding in the disinflation process, including favourable crude oil prices, a tight policy stance, and relative cedi stability.

This is in spite of the possibility of a deeper reduction.

The Monetary Policy Committee (MPC) anticipates headline inflation to ease to 15%±2% by the end of 2024 and gradually return to the medium-term target range of 8%±2% by 2025.

GCB Capital comments that the cut seems conservative, with the MPC relying on a commitment to maintaining a tight monetary policy stance and strict implementation of the 2024 fiscal budget to sustain the inflationary outlook.

While acknowledging the ongoing disinflation process, GCB Capital agrees with the MPC’s medium-term outlook despite emerging upside risks.

The firm expects the disinflation to persist but at a slower pace, potentially experiencing a shift in March 2024 due to unfavourable base drifts before resuming the downward trend from April 2024.

GCB Capital also notes that, despite economic indicators showing signs of continuous recovery, the Gross Domestic Product (GDP) growth remains below trend and necessitates stimulus.

The policy rate cut is seen as unsurprising, and GCB Capital anticipates the MPC will uphold a suitably tight policy stance to support the disinflationary process.

See statement below:

The rate cut could have been deeper, but for the emerging upside risks to inflation: The committee noted the several factors anchoring the disinflation process, including the tight policy stance, relative cedi stability, and favourable crude oil prices, among others, and the committee expect the disinflation process to continue despite the emerging upside risks to the inflation outlook”, it revealed in it Economic Update and Market Insight.

The MPC cut the policy rate by 100 basis points to 29% on Monday January 29, 2024. It expects headline inflation to ease to 15%±2% by the end of 2024 and gradually trend back to within the medium-term target range of 8%±2% by 2025.

GCB Capital said “Thus, the 100% cut appears to be a conservative action, given the upside risks to inflation, with the MPC counting on its commitment to maintain an appropriately tight monetary policy stance and a strict implementation of the 2024 fiscal budget to sustain the inflationary outlook”.

Disinflation process to continue but at slower pace

It continued that the disinflation process will continue but at a slower pace

“We agree with the MPC that the disinflation process is on course, and we are broadly aligned on the medium-term outlook for inflation despite the emerging upside risks. We expect the disinflation process to continue but at a slower pace, potentially changing course in March 2024 due to unfavourable base drifts before resuming the downward trend from April 2024”.

Again, it said though the 2.8% average growth outturn over nine months of 2023 is ahead of target and the leading indicators of economic activity are showing signs of continuous recovery, Gross Domestic Product growth is still below trend and requires stimulus; hence, the unsurprising cut in the policy rate.

However, it expects the MPC to maintain an appropriately tight policy stance to sustain the disinflationary process.

The total value of mobile money transactions in Ghana reached a record level in 2023, according to the 2023 Summary of Economic and Financial Data by the Bank of Ghana (BoG).

The total mobile money transactions for the year amounted to GH¢1.912 trillion, compared to GH¢1.07 trillion in 2022. In the first 10 months of 2023 alone, the total had reached a record GH¢1.527 trillion.

The data showed consistent growth throughout the year, with December 2023 recording the highest mobile money transaction value of GH¢199.3 billion.

Each of the 12 months in 2023 saw transaction values exceeding GH¢100 billion.

In January 2023, the value of mobile money transactions stood at GH¢130.1 billion, compared with GH¢76.2 billion during the same period in 2022.

It surged to GH¢134.0 billion in February 2023 (February 2022: GH¢76.5 billion) and subsequently to GH¢147.5 billion in March 2023 (March 2022: GH¢90.5 billion).

It however, fell to GH¢138.8 billion in April 2023 (GH¢87.7 billion), but shot up to GH¢159.7 billion in May 2023 (May 2022: GH¢71.4 billion) before declining slightly to GH¢149.4 billion in June 2023 (June 2022: GH¢77.1 billion).

But it achieved a then-record transaction of GH¢169.6 billion in July 2023, before declining to GH¢161.8 billion in August 2023. It again fell to GH¢157.0 billion in September 2023 (GH¢88.2 billion: September 2022) before hitting an all-time record of GH¢179.2 billion in October 2023.

It then surged to GH¢185.9 billion in November 2023 and to GH¢199.3 billion in December.

The Monetary Policy Committee of the Bank of Ghana (BoG) has announced a reduction in its key lending rate from 30% to 29.0%.

Chairman of the committee, Dr. Ernest Addison, made this announcement following the 116th meeting.

Dr. Addison mentioned that the decision to cut the lending rate was influenced by a consistent decline in inflation, which fell from 54.0% in December 2022 to 23.4% in December 2023. However, he also noted that there are downside risks despite the positive trend in inflation.

“The latest forecast suggests that the disinflation process will continue, and headline inflation is expected to ease to around 13-17% by the end of 2024, before gradually trending back to within the medium-term target range of 6-10% by 2025. These forecasts notwithstanding, there are upside risks to the inflation outlook and there is need for strict implementation of the 2024 budget and a tight monetary policy stance to sustain the disinflation process”.

“The Committee noted the emerging recovery but sees the need to maintain a strong policy stance to consolidate the disinflation gains. Under these circumstances, the Committee decided to reduce the Monetary Policy Rate by 100 basis points to 29.0%”, the Governor added.

Prior to the recent information, the Ghana National Chamber of Commerce and Industry (GNCCI) advocated for a reduction in the policy rate to support business growth.

In a statement, the GNCCI highlighted that Ghanaian businesses are grappling with a significant increase in borrowing costs, mainly due to the high Monetary Policy rate.

It emphasized that the elevated interest on commercial loans, averaging 32.0% in 2023, compounds the already high utility tariffs and excessive taxes, making the cost of doing business in Ghana exceptionally high.

The International Monetary Fund’s (IMF) “2023 Article IV Consultation” Staff Report reveals that the Bank of Ghana has given approval to the recapitalization proposals submitted by undercapitalized banks.

These banks are mandated to inject a minimum of one-third of the required capital annually over the next three years, concluding in 2025, to achieve a 13.0% Capital Adequacy Ratio without regulatory forbearance.

Currently, a majority of banks have already submitted their recapitalization plans.

“The BoG [Bank of Ghana] will initiate corrective measures by end-March 2024 against banks that fail to uphold these recapitalisation requirements (new structural benchmark). In the short term, the BoG [Bank of Ghana] stands ready to deploy contingency measures if needed to ensure financial sector stability.

The Bretton Wood said this move will ensure that banks’ capital needs have been estimated based on reasonable forward-looking assessments of losses from government debt restructuring and increases in Non-Performing Loans.

NIB’s insolvency plan to be addressed by end-2024

“The authorities [government, BoG] also aim to address the legacy issues of the financial sector and strengthen the governance of state-owned banks. The remaining tasks from the earlier sector cleanup include addressing the challenges of NIB and long-standing undercapitalization of several special deposit taking institutions (SDIs)”.

The report states that both the Bank of Ghana (BoG) and the Ministry of Finance will collaboratively formulate and initiate, by the end of March 2024, a credible, comprehensive, and cost-effective plan aimed at addressing the insolvency challenges of the National Investment Bank (NIB) by the end of 2024.

In order to mitigate the accrual of additional risks until the completion of this plan, the Staff Report of the Fund indicates that the BoG is dedicated to strengthening the monitoring of NIB and imposing appropriate constraints on critical risk areas.

The report emphasizes that the systematic resolution of other Specialized Deposit Taking Institutions and fund management firms, along with the settlement of outstanding payouts to clients of Securities and Exchange Commission (SEC)-licensed fund management companies, will be concluded by the conclusion of 2024. The government’s payouts will be executed through a burden-sharing approach to minimize fiscal costs.

Furthermore, the authorities are committed to developing a strategy ensuring that state-owned banks adopt sound governance principles, effective business models, and robust risk management systems to secure their long-term viability and facilitate an organized government exit.

The Bank of Ghana has indicated that Ghana received a whooping US$ 16.6 billion at the end of 2023.

This was contained in the Central Bank’s Summary of Macroeconomic and Financial Data for January 2024.

According to the report, the country as of December 2023 had received $16.6 billion from its exports compared to the estimated 14 billion dollars it spent on importing goods for the same period.

This indicates an increase from the 14.9 billion dollars recorded for exports and 12.8 billion dollars for imports in November last year.

On a year-on-year basis, the value of total exports was however a decrease from the $17.4 billion recorded in the same period last year.

Per the data from the Central Bank, the difference between the country’s exports and imports within the period under review resulted in a positive trade balance of $2.6bn.

The positive trade balance accounted for 3.4% of GDP, an improvement on the 2.7% of GDP recorded in the month of November 2023.

Commodities such as gold and cocoa contributed $7.6bn and $2.1bn respectively to the total export value.

Oil exports accounted for $3.8bn of total exports value with other exports accounting for the remaining $3bn.

On the imports side, oil and non-oil imports accounted for $3.6bn and $7.7bn of total import value.

Growth in exports contributed to an increase in the country’s the gross international reserves which stood at $5.1bn at end-October 2023 from $4.9bn at end-September 2023.

Growth in gross international reserves led to a marginal increase in the country’s import cover from 2.3 months in September to 2.4 months in October.

Net International Reserves of the country however stands at $2.1bn, also a marginal increase from the $2bn recorded in September 2023.

The Ghana National Chamber of Commerce and Industry (GNCCI) is advocating for a reduction in the policy rate to support business growth.

The Monetary Policy Committee (MPC) of the Bank of Ghana (BoG) is currently meeting to review developments in the Ghanaian economy, and an announcement on the policy rate is expected by Monday, January 29, 2024.

In a statement, the GNCCI highlighted that Ghanaian businesses are grappling with a significant increase in borrowing costs, mainly due to the high Monetary Policy rate.

It emphasized that the elevated interest on commercial loans, averaging 32.0% in 2023, compounds the already high utility tariffs and excessive taxes, making the cost of doing business in Ghana exceptionally high.

“The costly business environment has contributed to a significant decline in production, the collapse of many businesses; the rise in non-performing loans; the relocation of businesses to other African countries, and as a whole led to the significant decline in the growth of the private sector and the economy. From a GDP [Gross Domestic Product] growth rate of 6.1% in the 4th quarter of 2021 to 2.0% in the 3rd quarter of 2023”, it mentioned.

“As the representative body of the business community in the Country, the GNCCI is very mindful of issues that specifically impact the operational costs of businesses. With the 116th Monetary Policy Committee (MPC) meeting ongoing to discuss the policy rate adjustments, the GNCCI emphasizes the need for the review to favor the growth of businesses. The GNCCI urges the MPC to take into account the cost-push impact of a high policy rate”, it added.

Considering the relative stability in the forex market and the substantial decline of 30.4% in domestic inflation from 53.6% in January 2023 to 23.2%, implying that the Real Interest Rate in Ghana is now positive, the GNCCI proposed that the Bank of Ghana lowers the existing policy rate.

“We believe the reduction will induce commercial banks to also lower their lending rate to enable businesses to access funds for expansion in the short to medium term,” the Chamber added.

“As Ghanaian businesses endeavor to actively engage in the AfCFTA, the cost of borrowing will play a crucial role in defining their competitiveness. With Ghana’s interest rate being the highest in Africa, we urge the Monetary Policy Committee to lower the policy rate. In the chamber’s estimation, anchored on the stability in the forex market, decline in inflation and the projected GDP growth rate of 2.7%, we propose a reduction of not less than 2 percent or 200 basis points in the policy rate for the start”, it continued.

The GNCCI concluded that it will continue to engage stakeholders in the public and private sectors to ensure a thriving business environment that delivers shared growth and prosperity for all.

Former President John Dramani Mahama has called upon the minority caucus to closely scrutinize the activities of the Bank of Ghana concerning the recent release of the second tranche amounting to $600 million by the International Monetary Fund (IMF).

This disbursement follows the successful completion of the first review of the $3-billion three-year extended credit facility, approved by the Bretton Woods institution in May 2023.

In his appeal to the minority caucus for prudent utilization of the IMF funds by the government, Mr Mahama didn’t mince words as he criticized the Bank of Ghana, alleging that it has worsened Ghana’s economic challenges by introducing a surplus of newly-printed banknotes into the financial system.

While emphasizing the need for the government to exercise responsibility in handling the recently acquired IMF funds, Mahama directed a pointed critique at the central bank.

According to him, the alleged flooding of the system with freshly minted currency by the Bank of Ghana has contributed to the exacerbation of the economic difficulties faced by the nation.

Mr Mahama said “under normal circumstances, the release of $600 million by the International Monetary Fund (IMF) to the government of Ghana should provide relief to the already-overburdened and suffering Ghanaian.”

“It is, however, evident that Ghanaians will continue to suffer as long as Akufo-Addo, Bawumia and the NPP remain in office”, he posted on Facebook.

Mr Mahama urged “the outgoing NPP government to be cautious, responsible and judicious in utilising the IMF $600 million and other funds that may be made available to Ghana from the World Bank and other development partners”.

The former President declared that his party will closely monitor the government’s handling of the recently acquired funds.

“I have already encouraged the NDC minority in parliament to ensure strict oversight on both the government and not to take their eyes off the Bank of Ghana that illegally printed billions of cedis and aggravated our economic situation”.

“On my part, I will, from time to time, continue to engage the Ghanaian public about my vision to build the Ghana we want and how we will work together to create well-paying jobs through my 24-hour economy policy and other pragmatic initiatives”.

Last year, the Cassiel Ato Forson-led minority caucus marched in demand for the resignation of the Governor of the Bank of Ghana, Dr Ernest Addison as well as his two deputies.

“The purpose of this protest is to express our revulsion at the illegal printing of money (about GHS80 billion) between 2021 and 2022 by the BoG for the corrupt Akufo-Addo/Bawumia/NPP government which led to a hyperinflation rate of 54.1 per cent in December 2022”, Dr Ato Forson said in a statement at the time.

The caucus claimed GHC22.04bn of that amount was used by the BoG to support the government’s budget without parliamentary approval.

“This singular act of BoG”, he emphasised, “has negatively impacted livelihoods and businesses and pushed about 850,000 Ghanaians into poverty in the year 2022 alone”.

The caucus said as representatives of the people, it was “totally disgusted by the crass mismanagement and reckless mishandling of the affairs of the Bank of Ghana,which resulted in a gargantuan loss of GHS60.8 billion and a negative equity of GHS55.1 in 2022 with its attendant hardships on Ghanaians”.

The Bank of Ghana, however, denied the allegations.

In a statement issued on Tuesday, 26 July 2022, the central bank said Dr Forson’s claim could not be farther from the truth.

The bank observed that Dr Forson’s reaction was in response to the 2022 mid-year fiscal policy review which was presented to parliament by the Minister of Finance on Monday, 25 July 2022.

It explained: “In Appendix 2A of the Mid-Year Fiscal Policy Review document, under Financing, out of the total financing of GHC28.12 billion, an amount of GHC22.04 billion was captured under BoG”, adding: “This is the amount being referred to by the Ranking Member as BoG’s printing of currency to support the budget”.

Concerning the loss and negative equity posted by the central bank, Governor Addison later explained at a press conference that it was important for Ghanaians to appreciate that the GHS60.8 billion loss recorded by the nank in 2022 “were technical losses arising from the haircut and the application of accounting standards (in particular, IFRS 9) to estimate expected credit losses over the tenor of the Government debt held by Bank of Ghana”.

He told journalists on Monday, 21 August 2023: “It is not money lost by the Bank of Ghana through its operations in 2022”.

Rather, he said “one should look at this as a reflection of the total cost of the economic and social crisis the country faced over the years and an attempt to resolve a major structural problem of the Ghanaian economy.”

Also, Dr Addison said this is not the first time the central bank has recorded negative equity.

“I must also add that, if one takes time to go through historical financial statements of the Bank of Ghana, you will realise that this is not the first time that the Bank has gone into negative equity”, he stated.

He reported: “During the early years of structural adjustment, very large exchange rate depreciations led to revaluation lossesthat drove the Bank into negative equity”.

Indeed, Dr Addison mentioned, “anytime the economy faces major challenges, the Bank of Ghana balance sheet suffers, and the equity position moves into negative territories”.

“You will recall that in 2017 and 2018, the Bank of Ghana incurred similar negative equity from the impairment of legacy liquidity support loans granted in 2015 and 2016 to insolvent banks, which our external auditors impaired due to the doubtful prospects of recovering from those insolvent banks”.

“The Bank of Ghana, however, recovered and generated profits throughout the period 2019 to 2021”, he pointed out.

“It is worth noting that Central Banks are not commercial banks”, he highlighted, stressing: “Bank of Ghana’s current financial condition will not impact negatively on the operations of the Bank”.

He said the IMF Technical Assistance mission validated this conclusion before the necessary decisions were taken.

“In their opinion, the Bank of Ghana was policy solvent and would remain so, as it had enough income to cover monetary policy operational costs”, Dr Addison said.

The Bank of Ghana, he indicated, “had sufficient capital amounting to about 15 per cent of its total liabilities”, noting: “Its recommendation was for the Bank to retain all profits and a reassessment should be made in the year 2027”.

“The Bank will also manage to reduce its operational costs during this period”, he promised.

In all these, Dr Addison said the Bank of Ghana has “acted within the applicable laws”. He also denied claims that the central bank has been bankrolling the government annually.

“It is not true that Bank of Ghana has been providing financing for the Government every year. There has been zero-financing in 2017, 2018, 2019 and 2021. The Bank of Ghana has only had to support in the pandemic year of 2020 and the crisis year of 2022. The Bank of Ghana Act (612), as amended, limits financing of Government to 5 per cent of previous year’s tax revenue”, Dr Addison reiterated.

“This provision in the law has been adhered to since I took office in April 2017. Between 2017 and 2019, in addition to the requirements of the Bank of Ghana Act (612), as amended, the Bank signed a Memorandum of Understanding (MOU) with the Ministry of Finance to even impose a tighter restriction of zero-central bank-financing, and this was observed strictly, even though MOUs are not legally binding. Between 2012 and 2015, the Bank of Ghana provided overdraft to finance government and COCOBOD every year. And there was neither a pandemic nor a global economic crisis”.

“When Ghana was hit with the COVID-19 in 2020, Section 30(6) of the Bank of Ghana Act (612), as amended, was triggered, and as indicated earlier, the Bank purchased GHC10 billion worth of Covid-19 bonds to support the economy through the pandemic”.

“This was done within the applicable laws governing the Bank of Ghana. When section 30 (6) of the Bank of Ghana Act (612), as amended, is triggered, it, allows the Governor, the Minister for Finance and the Controller and Accountant General to agree on a new limit of central bank financing”.

“The law further says that the Minister of Finance will then have to inform parliament and the Minister has since informed parliament as part of his briefing to update Parliament on the IMF programme and status of the Domestic Debt Exchange”.

Governor of the Bank of Ghana, Dr. Ernest Addison, has provided reassurance to the public, affirming that the launch of the highly-anticipated e-Cedi, the country’s digital currency, will occur before the conclusion of 2026.

While acknowledging the advancements in the development of the e-Cedi, the Governor pointed out that the delay in its launch is attributed to the economic dislocation caused by the events of 2022.

“Probably, it could be earlier than that. As I mentioned, we have reached a point of trying to understand the commercials a little bit more,” said Dr. Addison during an interview held on the side-lines of the Eastern Caribbean Central Bank (ECCB) 40th anniversary and Central Banking Autumn meetings in Saint Kitts and Nevis in November 2023.

He further explained that after successful completion of the pilot phase in Sefwi Asafo, discussions on the e-Cedi’s commercial aspects were initiated. However, the COVID-19 pandemic’s onset and resulting economic crisis shifted priorities – leading the central bank to temporarily halt the digitisation process.

The pilot was an essential step in the country’s plan to enhance financial inclusion and promote digitalisation. Despite the setback caused by economic challenges, the central bank remains optimistic about the e-Cedi’s future.

In December 2023, the Bank of Ghana announced winners of the country’s first ever e-Cedi hackathon. The e-Cedi Hackathon reflects the fintech community’s enthusiastic engagement. The competition encouraged innovation and partnerships around the central bank’s new digital currency. Of 88 initial applicants, 10 finalists were selected to showcase their e-Cedi solutions; covering areas such as agriculture, government payments, business transactions, taxation and more.

Dr. Addison provided insights into the e-Cedi pilot’s status, emphasising its offline operational capacity. “The central bank did a lot of things due to favourable conditions at the end of 2019,” he explained. The pilot, conducted in some of the country’s remotest parts, featured an offline version of the digital currency to ensure usability in areas with limited connectivity infrastructure.

“The Ghanaian population is used to mobile money, so the concept of a digital currency was easily absorbed – it’s not an alien concept to people,” Dr. Addison highlighted. Positive results from the pilot, wherein participants were given a certain value to spend within their locality, demonstrated the e-Cedi’s potential success.

While the economic challenges of 2022 prompted a reevaluation of priorities, Dr. Addison emphasised that progress toward launching the e-Cedi is ongoing. The central bank’s adoption of a retail token-based CBDC, stored locally on various devices, aims to replicate traditional attributes of physical cash while incorporating additional functionalities.

“The e-Cedi’s successful deployment could have a significant impact on the country, helping to augmentthe government’s digitalisation agenda and foster financial inclusion,” Dr. Addison stressed. The Bank of Ghana seeks to reinforce its role as an active regulator and facilitator of a digital economy, aligning with the nation’s evolving financial landscape.

As Ghana advances in its digital currency efforts, the e-Cedi hackathon served as a crucial milestone, fostering innovation and supporting the nation’s goals of financial access and digital transformation. With assurances from the Bank of Ghana’s Governor, anticipation builds for the e-Cedi’s official launch – which is expected to bring transformative changes to the country’s financial ecosystem.

Bank of Ghana (BoG) secured a substantial 432,358 ounces (oz) of gold from members of the Ghana Chamber of Mines (GCM) by mid-December 2023 through the Domestic Gold Purchase Programme (DGPP) and a voluntary foreign exchange sales initiative.

This constitutes approximately 84 percent of the Bank’s targeted acquisitions for 2023 and represents nearly 15 percent of the planned output by GCM members for the same year, as reported by the Ghana Chamber of Mines (GCM).

The primary objective of the Bank of Ghana’s gold acquisitions is to mitigate the depreciation of the local currency and its subsequent impact on inflation.

The Chamber’s president, Joshua Mortoti, noted that this is in line with the commitment of GCM’s producing members to help government’s efforts to speed-up the economy’s recovery.

The Chamber, he added, is in the process of collating members’ planned gold sales to BoG for 2024, and will facilitate the signing of bilateral agreements between the central bank and mining companies after targets are finalised.

Mr. Mortoti was speaking at a breakfast meeting with the Minister of Lands and Natural Resources – organised by the Chamber in Accra, and also stated that: “In the same vein, members continued to voluntarily give the Bank of Ghana first option to buy forex they intend to sell for the local currency”.

The DGPP was announced in 2021 by government to enable BoG have the first right of refusal for all gold mined in the country. It is part of the central bank’s plan to build gold reserves to stabilise the cedi.

The decision was also against a background that the central bank had only 8.7 tonnes of gold reserves at end-2021, despite the country being one of the world’s leading gold producers.

Announcing the policy decision of the time, Vice President, Dr. Bawumia Mahamudu said: “The central bank will purchase the gold at world market prices and mining companies will export the portion that is not purchased by BoG. Ultimately, once we accumulate enough gold; future borrowing and our currency can be backed by gold. This will stabilise the cedi long-term.

“We must also deepen our industrialisation through value addition to gold; even though Ghana has two gold refineries, neither has London Bullion Market Association (LBMA) certification. This limits our full participation in the gold value chain. We will urgently work toward LBMA certification for our refineries over the next few years,” he added.

Also speaking at the breakfast meeting, Minister of Lands and Natural Resources Samuel Abu Jinapor said he continues looking forward to support from the Chamber for various interventions being implemented by government – including value addition, local content and participation, as well as development of mining communities.

He said: “Together, we will achieve the President’s vision to make Ghana the mining hub of Africa.

“The ministry remains fully committed to effective and efficient utilisation and management of our country’s natural resources, anchored on transparency, integrity and utmost good faith for the Ghanaian people’s benefit,” he added.

Member of Parliament for North Tongu, Sam Okudzeto Ablakwa, has made public documents shedding light on the government’s spending patterns during the 2020 election year.

In a Facebook post on January 17, Mr. Ablakwa shared a document from the Public Procurement Authority (PPA) detailing the procurement process for the construction of a 50-bed guest house in Tamale.

The document indicated that approval was granted to the Bank of Ghana to employ single sourcing, engaging Messrs De-Simone Limited for the final works on the project at a cost of GHC139 million.

Mr. Ablakwa raised concerns about what he perceives as an unhealthy inclination toward restricting tendering by the Governor of the Bank of Ghana, Dr. Ernest Addison.

“The fresh documents in my possession show that Dr. Addison appears to have a hooliganistic appetite for single-source and restricted tendering so much so that NONE of the procurements under his watch have been competitive,” Mr Ablakwa wrote.

He added, “The venerable Togbe Afede XIV was obviously right when he wrote in his latest op-ed that the BoG has failed us.”

He recalled the times when President Akufo-Addo during his time in opposition condemned “single source procurements and argued that it was a veritable conduit for corruption.”

“Without principle and scruples, they are now the all-time champions of grand single source procurements.

“It is most instructive to note that payments for other infamous wasteful Akufo-Addo-legacy projects such as the US$450million National Cathedral fiasco and the US$222.7million BoG Head Office all commenced during the electioneering campaign of 2020,” he added.

“The Akufo-Addo/Bawumia single-source-procurement-regime will be planning similar “lootocratic” schemes,” he warned.

Fitch Solutions predicts that the Bank of Ghana will initiate a significant monetary easing cycle, reducing the policy rate by a total of 800 basis points to reach 22.00% by the close of 2024.

This projection is based on a considerable moderation of headline inflation, as indicated by the UK-based firm.

“With inflation moderating substantially through 2024, we anticipate that the BoG will embark upon a sizeable monetary easing cycle, cutting the policy rate by a cumulative 800bps to 22.00% by year-end.”

Fitch Solutions noted that the impact of interest rate adjustments on the real economy typically requires around 12 months due to the lag in monetary transmission mechanisms.

Consequently, the firm believes that the Bank of Ghana‘s dovish monetary policy stance is improbable to lead to a significant rise in real loan growth. This is particularly evident as real loan growth has persisted in contractionary territory from January to August 2023.

The Bank of Ghana increased the benchmark policy rate to 30.00% in 2021, a rise of 1,150 basis points. Access to corporate credit has been hampered as a result.

In the meantime, the Bank of Ghana’s Monetary Policy Committee will review economic developments during its 116th regular meeting, which will take place from Tuesday, January 23 to Friday, January 26.

In response to escalating geopolitical tensions impacting oil prices and a year-end consumer inflation rate of 23.2 percent, the Bank of Ghana Monetary Policy Committee (MPC) is poised to maintain its ‘tighter-for-longer’ policy stance until inflation is securely anchored.