Despite global challenges, Ghana’s economy exceeded expectations, with key indicators performing better than predicted for several months.

Data from the Ghana Statistical Service (GSS) shows that the country recorded an average GDP growth of 6.3% for the first nine months of the year, compared to 2.6% during the same period in 2023.

This growth was fueled by quarterly increases of 4.8% in the first quarter, 7% in the second quarter, and a remarkable 7.2% in the third quarter – the highest in five years.

The non-oil sector also played a major role, achieving an average growth rate of 6.2%, up from 2.6% last year. Quarterly growth in this sector was 4.3%, 6.6%, and 7.7% for the first, second, and third quarters respectively.

These numbers suggest that Ghana is on track to surpass the 4% GDP growth target set under the IMF program.

Consumer inflation

Inflation continued to rise in 2024, reaching 23% in November, up from 22.1% in October, according to the Ghana Statistical Service (GSS).

Although inflation dropped from a high of 54.1% at the end of 2022 and 23.2% in December 2023, it remained unstable and failed to hit the government’s initial target of 13% to 17%.

From 20.4% in August, inflation steadily climbed due to rising food prices and the lingering effects of earlier currency depreciation. It now seems likely that inflation will stay above 20% in December 2024.

In January 2024, the Bank of Ghana (BoG) lowered its key policy rate by 1% (100 basis points) to 29%, marking the first cut since 2021. The decision was based on a decline in inflation.

The policy rate stayed unchanged for most of the year until it was reduced again by 2% (200 basis points) in September due to inflation trends. However, in November, it was maintained at 27%.

As a result, borrowing costs remained high, with average lending rates exceeding 30% due to persistent economic risks.

The Ghana Reference Rate, which was 31.31% at the start of the year, gradually dropped to 28.84% in early November but was raised slightly to 29.31% for December 2024.

IMF-supported programme

The Post-COVID-19 Programme for Economic Growth (PC-PEG), supported by the IMF, has delivered significant results.

Ghana successfully secured an additional SDR 269.1 million (US$360 million) after the IMF Executive Board approved the third review of the programme, bringing total disbursements to US$1.92 billion.

The country achieved all six key performance benchmarks and four indicative targets set for June 2024, marking a major achievement. Efforts to streamline government spending have also paid off, with the primary balance improving from a 4.3% deficit of GDP in 2022 to a surplus of 0.4% by mid-2024.

Foreign currency reserves grew to US$7.7 billion in October 2024, up from US$5.2 billion in October 2023, offering 3.5 months of import coverage.

Funding for social programmes also increased, benefiting initiatives such as the National Health Insurance Scheme, school feeding programmes, and the Livelihood Empowerment Against Poverty (LEAP) project.

Debt restructuring

Significant milestones were recorded in the nation’s debt restructuring efforts during the year under consideration. Agreements were reached with the Official Creditor Committee under the G20 Common Framework to restructure US$5.1billion in bilateral loans, securing debt service relief of US$2.8billion between 2023 and 2026. Additionally, Eurobond holders agreed to restructure US$13.1billion in debt, resulting in a US$4.7billion cancellation and US$4.4billion in debt service savings.

Consequently, the debt-to-GDP ratio fell from 79.2 percent in September to 74.6 percent in October 2024, resulting in a much-needed reduction in public debt stock. The IMF confirmed that these restructuring efforts align with programme parameters, marking Ghana as a model for swift and successful debt negotiations under the Common Framework.

Energy sector reforms

After years of negotiations, the government reached agreements with Independent Power Producers (IPPs) to restructure legacy arrears and power purchase agreements (PPAs). This initiative is expected to provide fiscal relief and ensure reliable power supply. The restructuring includes amendments to PPAs and master gas supply arrangements between the Electricity Company of Ghana (ECG) and the Ghana National Petroleum Corporation (GNPC).

Banking developments

The industry’s total assets surged by 42.4 percent to reach GH¢367.2bn in the year to October, a marked acceleration from the modest 3.2 percent growth recorded in the previous year.

Private sector credit expansion accelerated markedly to 28.8 percent year-on-year in October, representing a substantial reversal from the previous year’s contraction. Banking sector resilience improved moderately, with capital adequacy ratios strengthening to 11.1 percent, though asset quality deteriorated as the non-performing loan ratio climbed to 22.7 percent.

The industry’s outlook remains contingent upon earnings recovery and adherence to recapitalisation requirements. Notably, real credit growth turned positive at 5.5 percent, following the previous year’s significant 31.6 percent decline.

SME support

The government deployed nearly GH¢2.1billion under the SME Growth and Opportunity (GO) programme to support small and medium enterprises (SMEs). The Ghana Exim Bank received GH¢700million to provide subsidised financial assistance, while the Ghana Enterprises Agency (GEA) and the Development Bank Ghana (DBG) allocated GH¢230million and GH¢1.4 billion, respectively, to support high-growth SMEs and MSMEs.

Currency performance

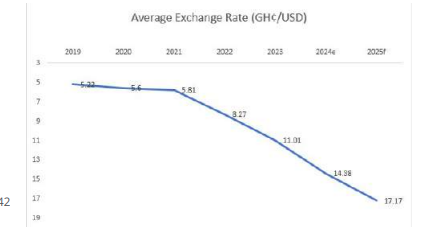

The cedi faced continued pressure in 2024, depreciating by 28 percent against the US dollar, compared to last year.

This was attributed to strong domestic demand for foreign currency and a stronger dollar globally. This decline contrasted with a 9.78 percent depreciation in the same period in 2023.

The unit has clawed back some gains, following the central banks injection of more than US$800million into the market in November.

Fixed income market

The fixed income market showed mixed performance in 2024. While treasury bills attracted strong investor interest due to attractive yields, the secondary bond market remained below pre-Domestic Debt Exchange Programme (DDEP) levels. Yields on 91, 182 and 364-day treasury bills declined, reflecting reduced inflation and a cumulative 300-basis-point cut in the monetary policy rate.

The secondary market began picking up as government was able to meet it obligations. As of end-November 2024, traded volumes reached 153.52 billion, marking a 87.97 percent increase over the 81.67 billion traded in the corresponding period last year. This corresponded to a value traded of GH¢126.58billion.

On the equities front, the value of shares traded from January to November 2024 amounted to GH¢1.996billion, approximately GH¢ billion, marking a 165.44 percent increase compared to the GH¢752million recorded during the same period in 2023.

This surge was accompanied by a 71.29 percent rise in traded volumes, which reached 952.72 million shares during the period. As a result, the market capitalisation climbed to GH¢108.4billion, significantly higher than the GH¢74.2billion recorded by the end of November 2023.

“Awula, your selfless commitment to Ghana’s development is deeply appreciated and deserving of praise, And I assure you that the issue on land compensation and ensuring protection will be satisfactorily resolved just as compensation for crops that have been affected.”

“Awula, your selfless commitment to Ghana’s development is deeply appreciated and deserving of praise, And I assure you that the issue on land compensation and ensuring protection will be satisfactorily resolved just as compensation for crops that have been affected.”